You are reading an excerpt from our free but shortened abridged report! While still packed with incredible research and data, for just $20/month you can upgrade to our FULL library of 50+ reports (including this one) and complete industry-leading analysis on the top crypto assets.

Becoming a Premium member means enjoying all the perks of a Basic membership PLUS:

- Full-length CORE Reports: More technical, in-depth research, actionable insights, and potential market alpha for serious crypto users

- Early access to future CORE ratings: Being early is sometimes just as important as being right!

- Premium Member CORE+ Reports: Coverage on the top issues pertaining to crypto users like bridge security, layer two solutions, DeFi plays, and more

- CORE report Audio playback: Don’t want to read? No problem! Listen on the go.

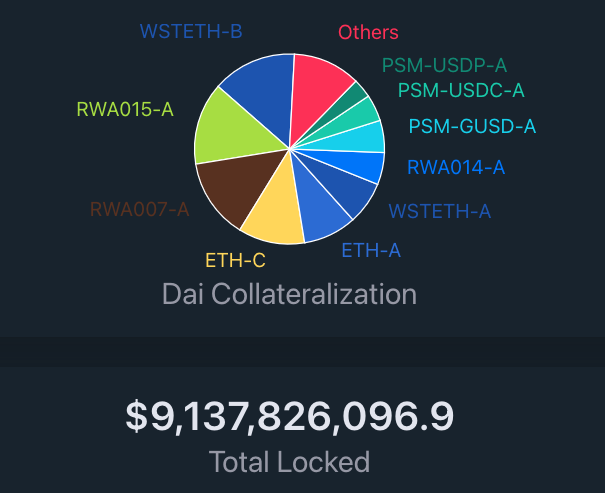

DAI Collateral

MakerDAO's DAI stablecoin has been making significant strides toward diversification and decentralization in 2023. The organization's recent strategic shift towards real-world assets (RWA) has resulted in a substantial decrease in DAI's collateralization by USDC, a constant point of concern given its centralized nature. The move into RWAs has not only diversified the risk associated with centralization but has also created a yield-generating opportunity for DAI holders.

In June, MakerDAO purchased an additional $700 million worth of U.S. Treasury bonds, a move that pushed USDC collateralization in its Peg Stability Module (PSM) below 10%, down from its peak of 64%.

Following instability in the banking system in Q1 2023, stablecoins experienced considerable volatility themselves. This initially occurred due to ~8% of USDC's collateral being tied up in the failing Silicon Valley Bank (SVB). Off-chain reserve-based stablecoins, such as USDC and Tether (USDT), claim to maintain $1 of assets, like cash or securities, for every digital token issued on-chain. As a result of the USDC/SVB news, traders started selling the coin, causing its value to drop below $0.90. This led to USDC holders depositing their tokens in the PSM (discussed more below), minting Dai, and selling it, causing Dai's price to lag behind USDC's. This has resulted in MakerDAO governance adding a 1% fee to the PSM and adjusting protocol parameters to bypass the Governance Service Module Delay to avoid similar occurrences in the future.

Dai (DAI), the largest on-chain collateralized stablecoin with 36% of its reserves in USDC, also experienced a significant decrease in value, falling below $0.90 as well. Notably, Dai was collateralized at 147%, meaning that even if all the USDC backing it became worthless, it would still have been over-collateralized.

Source: NYDIG

Source: NYDIG

All of this has led to Dai being more backed by USDC than before, and there is disagreement within the Maker community on how to address this issue. Some believe in decoupling Dai from the US dollar to become an independent stable currency, but this option seems unrealistic given that there is almost $6bn of Dai in circulation that is pegged to the dollar.

Ultimately, the Maker community must acknowledge that Dai is a product with market adoption and that it must operate within its self-imposed USDC constraints. While there is no clear plan for weaning off of USDC, it is clear that the community must work together to find a solution that works for everyone. As the cryptocurrency industry continues to evolve, it will be interesting to see how MakerDAO and other stablecoin projects adapt to meet the demands of the market.

The blacklisting of USDC addresses by Circle in 2022 and the subsequent depegging of USDC in March accelerated MakerDAO's efforts to reduce reliance on the stablecoin. The organization has primarily achieved this by investing in other RWAs, such as U.S. Treasuries. This strategic shift has not only mitigated the risks associated with USDC centralization but has also enabled MakerDAO to earn better yields and pass these onto DAI holders through the DAI Saving Rate, which was recently increased from 1% to 3.49%.

MakerDAO's strategic shift has been a significant step towards addressing criticisms related to its reliance on USDC, particularly those concerning centralization and censorship. The organization believes that DAI can maintain sufficient decentralization by diversifying the composition and location of its RWA collateral, rather than eliminating the risks associated with accepting centralized collateral like USDC.

However, MakerDAO's push into RWAs also exposes DAI to other forms of centralization risks. This move could potentially pave the way for the emergence of more decentralized, censorship-resistant stablecoins that align more closely with Rune Christiansen’s original vision of a truly decentralized stablecoin. Despite these challenges, MakerDAO's focus on RWA initiatives has positioned DAI as a standout among other "decentralized" stablecoins, offering yield-generating opportunities through the DAI Savings Rate.

Source

Source  Source: TokenTerminal

Source: TokenTerminal