You are reading an excerpt from our free but shortened abridged report! While still packed with incredible research and data, for just $20/month you can upgrade to our FULL library of 50+ reports (including this one) and complete industry-leading analysis on the top crypto assets.

Becoming a Premium member means enjoying all the perks of a Basic membership PLUS:

- Full-length CORE Reports: More technical, in-depth research, actionable insights, and potential market alpha for serious crypto users

- Early access to future CORE ratings: Being early is sometimes just as important as being right!

- Premium Member CORE+ Reports: Coverage on the top issues pertaining to crypto users like bridge security, layer two solutions, DeFi plays, and more

- CORE report Audio playback: Don’t want to read? No problem! Listen on the go.

Banks Burn Down

The recent failures of Silicon Valley Bank, Signature Bank, and the voluntary liquidation of crypto-focused Silvergate Bank have caused significant turbulence in the banking sector. The Federal Reserve's aggressive rate hikes have pushed deposits away from banks in search of higher money market yields, resulting in liquidity and solvency issues.

To mitigate the crisis, the US Regulators and the Fed guaranteed deposits at the affected banks and introduced the Bank Term Funding Program (BTFP), offering up to one-year liquidity in exchange for eligible collateral. However, this solution is only short-term, as banks continue to face deposit outflows and become increasingly dependent on Fed liquidity.

The Fed now faces a challenging decision between tackling inflation or supporting the financial system. With the Fed's balance sheet expanding significantly due to banks tapping into various liquidity facilities, the prospect of further rate hikes while simultaneously providing liquidity for the struggling banking sector appears unlikely. The unfolding crisis reinforces the original narrative that gave rise to cryptocurrencies, making the case for decentralized finance even stronger.

Meanwhile, over in Europe, Switzerland's largest bank, UBS, has confirmed a rescue acquisition of its struggling competitor Credit Suisse, in an effort to alleviate financial market turmoil.The 167-year-old bank's shares plummeted 25% last week, with massive withdrawals from investment funds and deposits. A nearly $54 billion emergency loan from the Swiss National Bank failed to stabilize the situation but allowed time for the rescue deal to be negotiated.

UBS is purchasing Credit Suisse for 3 billion Swiss francs ($3.25 billion), approximately 60% less than the bank's market value when markets closed last Friday. Credit Suisse shareholders will face significant losses, as their shares will be exchanged for UBS shares at a lower value. Holders of $17 billion worth of riskier bank debt will lose their entire investment, according to Swiss regulators.

Remarkably, the Swiss government has agreed to amend the law to expedite the deal without requiring shareholder approval. Credit Suisse had been suffering from declining investor and customer confidence for years, culminating in a dramatic loss of faith last week due to accounting issues and the collapse of Silicon Valley Bank and Signature Bank.

U.S. Macro and the Fed

Over the past twelve months, this column has consistently cautioned that Quantitative Tightening (QT) would ultimately fail, compelling the Federal Reserve to implement another series of emergency liquidity infusions, reminiscent of the repo crisis in September 2019. Merely nine months following the official launch of QT, we now find ourselves in this situation.

Having withdrawn a trillion dollars in cash from commercial banks, QT claimed its initial casualty. Silicon Valley Bank collapsed, triggering a domino effect of contagion and fear. In response, the Fed supported uninsured depositors from the prestigious institution and devised a new emergency lending mechanism for other struggling banks.

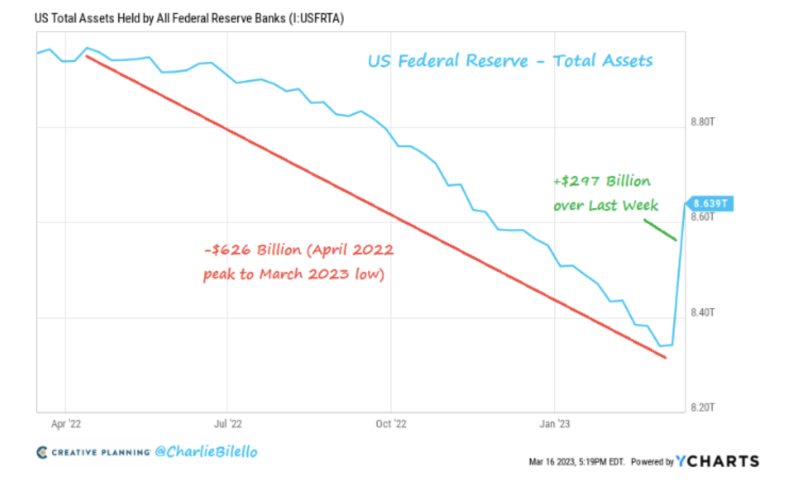

The most recent Federal Reserve balance sheet data, released on Thursday, demonstrates the extent of the new liquidity offered to the banking sector. Over the past week, the Fed's balance sheet grew by $297 billion, offsetting approximately half of the total impact of QT to date.

How could a liquidity crisis emerge so early in the QT process, especially considering the massive monetary expansion of the previous two years? The Fed had anticipated QT to operate in the background for years, decreasing its overall balance sheet by trillions. However, the Fed ended up hastily addressing a bank run.