Welcome to part 2 of my guide to everything about LPs and IL, you should read part 1 first here.

A deeper dive into Impermanent Loss

As discussed in part 1, IL is experienced when the price of two assets in a liquidity pool changes relative to eachother. As such, for people to actually profit from providing liquidity the IL in a period of time must be lower than the fees generated for that period of time. At first glance this might look to someone that any and all price change is bad for an LP, however this is only true in the case of them putting in both the assets that they would have otherwise held, the story changes entirely once we look at maintain a market position while being an LP. Simply put, if you provide liquidity in only 1 of the 2 (or more in Balancer) assets then you are no longer neutral, and one side of IL will benefit you. So if you have supplied only ETH to the ETH/USDC pool by selling half the ETH to USDC then putting in both as LPs then the price of ETH falls you will not only have gained the fees from the pool, but also would have more ETH than you put in due to IL. This is because the pool would now have more ETH and less USDC, meaning the value in USDC fell but the value of your LP tokens in ETH increased.

This becomes much more powerful when coupled with a lending platform like Compound (which you can read more about here). For example, if you want to be net long Ethereum while still making money from LP fees you would use your ETH as collateral in Compound to take out a loan of USDC, then sell half the USDC to ETH to provide liquidity. Now, let’s say the price of ETH goes up substantially, now your LP share would have a lot more USDC and less ETH, however as discussed previously since you only provided liquidity through one asset this would benefit you. In this case you would be able to pay back your loan with that USDC you gained from IL and you would be left with the ETH part of your LP tokens, essentially you have gained some ETH from IL as well as all the fees from swaps over that period of time. This can also work vice versa by borrowing ETH to act as a short instead, and of course the idea can be applied to any and all tokens.

Liquidity mining – even more gains

So far, I have talked about “LP tokens” a few times but never mentioned what they are or what role they play. Essentially, they are tokens that prove your share of the liquidity pool, this exists across most DeFi platforms too as different tokens that represent your deposit into a certain platform. This makes it much easier to transfer these shares between people and addresses instead of taking out your liquidity, sending the tokens to a new address and adding liquidity again there. This system gave rise to a phenomenon knows as Liquidity mining (or Yield farming) which grew big due to the Yam and Sushiswap platforms which attracted millions of dollars in liquidity staked in their contracts. Since your LP tokens accrue the fees automatically regardless of where they are or what they are doing, what if you could use those LP tokens to make even more money. This is where this phenomenon pops up.

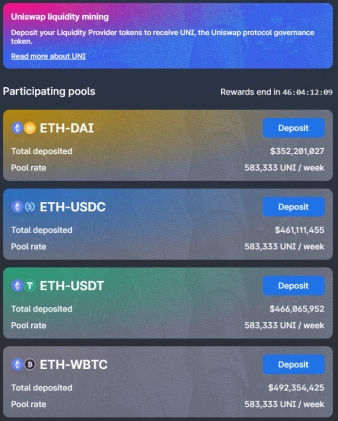

Essentially you deposit your LP tokens to a smart contract and receive back that platform’s native token, for example you could lock ETH/USDC LP tokens in Sushiswap and make sushi as long as your LP tokens were deposited. You could then sell those tokens for even more gains on top of the fees you get from providing liquidity. This can be seen best in Uniswap’s new token UNI that is currently being distributed to the LPs of the 4 biggest Uniswap pools. On one hand, providers gain additional income, on the other is the importance of these platforms in the first place. Some platforms use this “mining” or “farming” to simply distribute their token in a somewhat fair manner instead of a presale or airdrop or something else of the sort, these tokens can then be used for governance, or given additional uses on the platform such as profit sharing with Sushi. This makes it possible for people to invest into a platform without directly giving it money or buying its native token outright, instead earning it for providing a service.

There are many other popular implementations of this, however, it is also important to realise that unless the underlying platform and token have value that this sell pressure created by LPs can destroy any token in a matter of days or even hours.

A quick overview of other AMMs

So far, I have mostly looked at Uniswap because it is the largest AMM by value locked and is the most popular in the space, however as I previously mentioned it is not the only one. I will be writing much more in-depth articles about these other platforms in the future; however, this will provide a quick overview of other options. Particularly Curve and Balancer.

Curve is an AMM focused entirely on stablecoin and synthetic asset pools, offering high liquidity for most popular stablecoins as well as different synthetics of an asset such as renBTC/WBTC/sBTC. As such it uses a different formula and system than Uniswap that is much more specialised and is geared to be the best at those exact swaps.

Balancer is another AMM that differs from Uniswap in 3 major ways, firstly pools in Balancer can feature more than 2 assets, for example one pool might have WBTC/ETH/LINK/COMP. Additionally, it allows for different asset percentages than 50/50 like in Uniswap, for example a pool can consist of 90% ETH and 10% USDC, which in this case would be a pool geared more towards users who wish to be LPs while holding an overall long position on ETH. This feature means that fluctuations in price in the asset with a smaller allocation will not create as much IL as a 50/50 pool. Lastly, each pool has a custom swap fee set by the creator of it, so unlike a fixed 0.3% fee on all Uniswap pools you can have some Balancer pools with 2% fees and some with 0.1% fees.

This concludes the overview of being an LP and all the in-depth analysis of different strategies, avoiding IL, and making profit from providing liquidity. Thanks for reading and I hope that we can have further discussion in the comments.