On the topic of passive income, I have wrote before about how to Earn 25% APR during the Elrond Genesis Staking.

What is it?

Nexo is positioning itself as a crypto lending service. The people who don't want to sell their crypto, but need liquidity instead, can post their crypto as loan collateral and borrow fiat instead. I see their collateral is 90% for stablecoins and around 50% for the rest of the crypto currencies. Nexo is also backed by Credissimo who aren't exactly amateurs in the European lending market.

I have mentioned the above bit despite not being interested in borrowing from Nexo merely to shed some light into their business model. The thing that caught my eye is the high interest accounts. Basically, the stablecoins or fiat deposited in their accounts is used by Nexo for lending, while the accounts are collecting a nice 8% interest with daily compounding. Nexo says this is "risk-free" which sounds a bit optimistic as high volatility on the crypto market and no liquidity on their part may posses challenges if a lot of their lenders need cash. As with every investment, there is at least some degree of risk.

Assets earning interest

There's a couple of ways one can earn - stablecoins and fiat. Nexo is by far the most flexible platform I have tested as there's no coin to stake to get the maximum benefits and there's no minimum term. Their accounts don't behave like savings bonds. More like savings accounts with instant access, without losing the interest rate in the process. They earn daily interest for as long as the accounts are being funded.

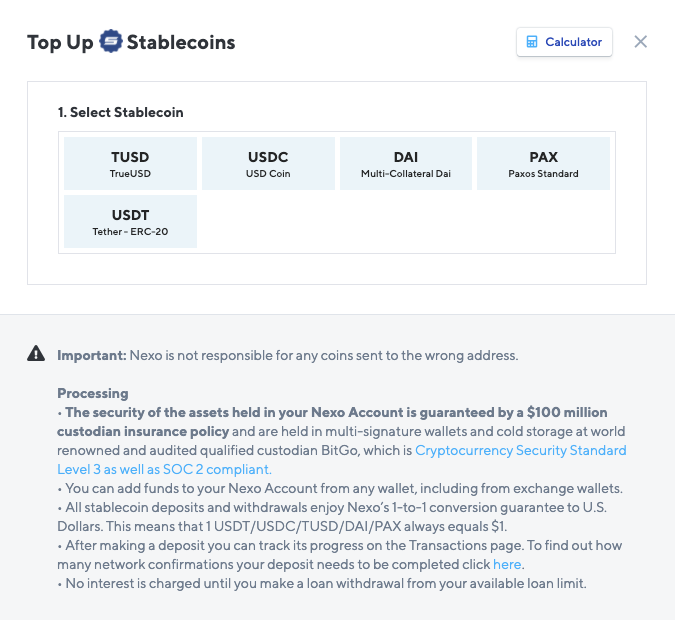

For stablecoins, Nexo takes a bunch of cryptos pegged against the USD: TUSD, USDC, DAI, PAX, USDT. I haven't seen an actual minimum limit as for testing purposes, my first transaction was $6 worth of DAI to see how it behaves. It has started to collect interest the next day, albeit at this rate, I don't see myself owning a yacht anytime soon. Then, deposited some more DAI. The interest is accumulated for the deposited token and may only be withdrawn using the deposited token. Nexo do not operate an exchange platform in the proper sense.

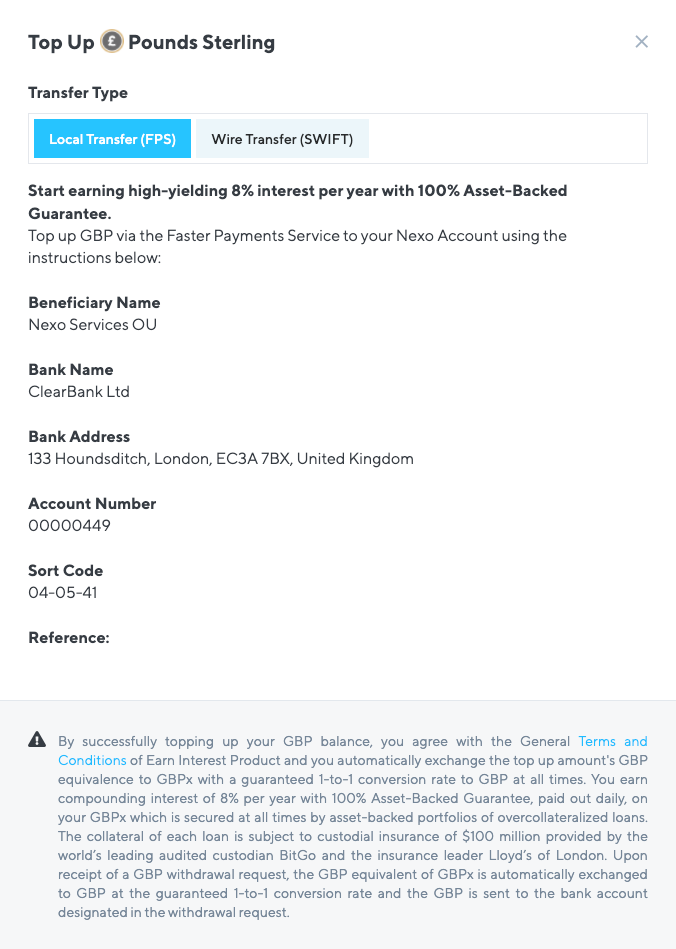

For fiat, they only support EUR and GBP. These accounts can be funded by a bank account and you can only withdraw to a bank account. These types of accounts do have a minimum limit which for the moment is €1000 or £1000, depending on the currency. They promise that those limits will be lowered soon, albeit measuring the time until soon is like figuring out how long is a piece of string.

The bar for fiat accounts isn't necessarily low, but with the interests being historically low due to the ongoing COVID-19 crisis and the high streets banks neutering the interest rates of my savings, this is a decent proposition. Bear in mind that when the money is funded to the accounts, it is being converted to EURx or GPBx, so technically this looks like staking.

These are also stablecoins pegged against EUR and GBP. Upon withdrawal, the stablecoins are converted back to the currency they are pegged against. Depending on the jurisdiction, this has different tax implications as these are not treated like savings accounts on a high street bank. There shouldn't be any capital gains as they are using a 1:1 conversion ratio. As I am not a tax accountant and this is not tax advice, you should ask for the advice of a qualified professional.

Also, they are promising that soon they are going to introduce the possibility for earning interest for crypto assets, albeit I shall believe it when I see it.

NEXO token

I have mentioned that there's no coin to stake to benefit from the high interest rates and flexibility. They do have their own ERC-20 token. They promise that they distribute 30% of their profit to the eligible token holders staking the tokens on Nexo i.e "dividends". Bear in mind that is not 30% yield.

While they have taken measures to limit the volatility around ex-dividend date by having the loyalty rates, I am not really convinced about the rest. Last year the reported yield was around 12% and I assume that's with a long loyalty period. However, the difficulty for buying NEXO is eating up into potential returns as Changelly takes around a whopping 12% in transaction fees when funding with a Debit Card compared to the value of the token on the spot market. The initial impact is quite large when buying into this token.

This is far less convenient than their fiat accounts even if you can get some cheaper on Huobi Global. Add on top of that the volatility of the crypto markets, the seemingly lack of communication from Nexo with respects to their "dividends", and the fact that their OTC desk don't want to hear from you unless you have $100,000 in a spare wallet. You got the recipe for something which isn't that desirable.

Therefore, the amount of hoops to jump through makes paying into the fiat accounts the headache-free option for passive income with Nexo.

I have said "dividends" as NEXO tries to position itself as a security token, but I have failed to see any proof that it gives any actual rights apart from a promise to distribute 30% of the profit. The real shareholders are those usually reaping the benefits.

This article is not investment advice. Should you need it, please hire the services of an independent financial advisor.

This article contains referral links should you wish to support the author.