The idea of a social security program is relatively new still in the grand history of things. Capitalism in general is far older, dating back to the Middle Ages and even as far back as Rome when it comes to chain businesses and networks. It was really in the 20th Century and increasingly after World War II that countries in Western Europe, Asia and the U.S. really began creating social security nets for seniors and elderly. Prior to that point, if a family didn't have the self-economic means to support, a senior pretty much worked until he or she dropped or went into homelessness and begging.

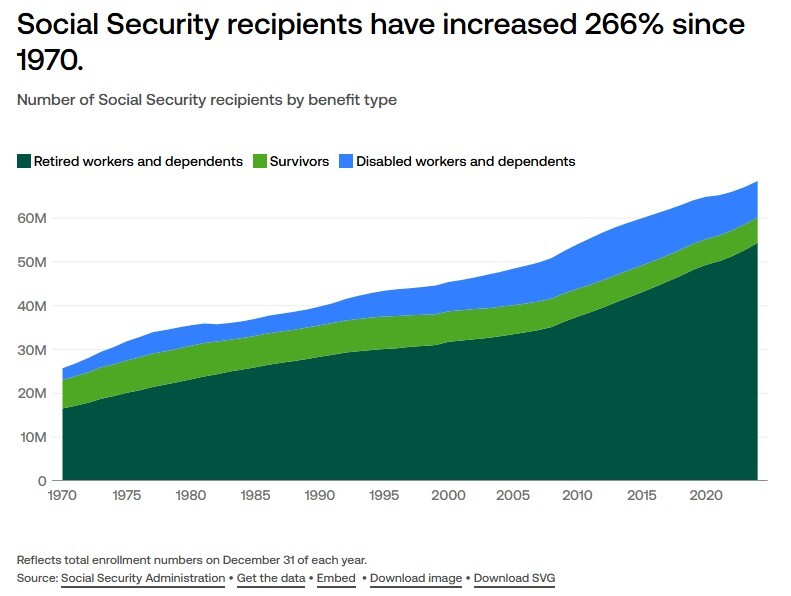

The concept for modern senior financial support was fairly straightforward and has even been compared to a Ponzi scheme, just legalized as government programs. Basically, younger generations who are charged a percentage of their gross earnings every pay period, which then goes into the big pot for retirement costs paid out to support seniors. The thinking is, statistically, there will be more workers paying in at any given time than seniors getting paid out. This statistical assumption is due to studies in health, mortality, economics, and rates of accidents. In some cases, people just die well before they reach senior age. Of course, the assumptions behind these programs when first created in the early 20th century were a bit off as well. Wars were killing off significant numbers of adults in young or prime age, and no one expected the latter third of the century to explode in population the way it did after 1970. Additionally and compounding application versus theory, no one expected governments to be raiding/borrowing their retirement funds either versus just leaving the deposits alone and letting them grow in size.

Source: USAFacts.com and U.S. Social Security Administration, 2025.

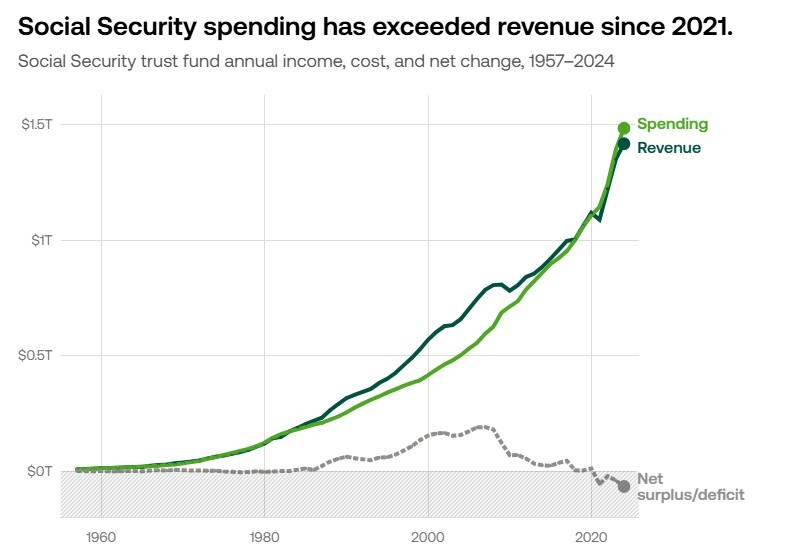

So, given the fund-shifting, bad assumptions, population growth, lack of big wars, wide-scale improved health and general safety improvement, now the same social security programs have a big problem - looming insolvency. Essentially, there's not enough money in these jumbo accounts to pay out senior support at the same level it is paid out now, including all the existing criteria, filters and eligibility checks already in place. Ergo, some of the biggest accounts, like that of the U.S. social security program are projecting being tapped out by the mid 2030s (just in time for my retirement, goddammit!, story of my generation, sheesh.).

To offset the inability to pay out and prolong the effectiveness of such programs and extend their solvency, a number of options exist. The most obvious is to bring more money in. That essentially means raising the social security contribution from people's paychecks, which is generally seen as a tax increase (it's not really a tax, even though the charge feels like it as a withholding; it's a credit for eligibility to participate, but that's a semantic nuance when your paycheck is being effectively reduced).

Source: USAFacts.com and U.S. Social Security Administration, 2025.

The next option is to reduce costs going out. The most broadband way to put that option into effect is either to reduce eligibility or cut off participants. Cutting people off arbitrarily is a sure way to create upheaval and accusations of favoritism, so eligibility gets the focus instead. And that comes with the controversial "age of retirement." The age metric essentially dictates when a person can actually legally claim senior social security benefits. Some countries have a singular minimum age, and others have a range of choices. The big difference is in how much money one gets in benefits monthly per choice. Earlier dates produce less, standard is the middle range, and longer age dates get more money. It might not seem fair at first, but again statistics take over. Higher payments for waiting longer can be a savings as less people live as long to get their payments, both in terms starting and cumulative effect. So, it's actually possible to wait, get more in a benefit monthly, and receive less because you died sooner within the payment window than someone who starts earlier, gets less, but lives longer in the payment window. Crazy mortality math here.

The age bump has already been applied recently in France in 2023. There, the government raised the eligible retirement age from 62 to 64 with 43 years of documented working (note the average in many European countries is age 65 already). The reaction was a number of huge protests, mainly due to the expedited "sneaky" way of passing the law, but it stuck and the age went up. Older folks were pissed at having to wait longer for what they worked for, and younger people felt their benefits were pushed out further from reality. No one was happy except France's administrators. Financially, the change is expected to reduce the cost impact to France's government (previously 14 percent of GDP) for senior support/retirement, rebalancing the country's pension account by 2030. The U.S., in comparison, spends 7 percent of its GDP on social security, but only gets 50 percent of it replenished versus France's pre-law inbound level of 74 percent. And, Americans work longer, seeing early retirement at 65, standard at age 67 now, and late retirement at 70 (again the range option). So, compared to the French, Americans work longer, get less, and their country's retirement account is deeper in the hole.

While chatter in these discussions focuses on the burden to those paying in, what often gets ignored or omitted is the fact that, at least in the case of the U.S., the government has repeatedly tapped into and take retirement monies without returning it. Depending on the math and whom is asked, the amount of funds missing involves approximately $2.9 trillion borrowed by the U.S. government from the Social Security Trust Fund. Most would argue pay it back to avoid the 2034 looming insolvency. That seems practical. Yet the counter-argument to that is that the borrowing generates approximately $804 billion in interest from 2017 through 2027. Wiping out the debt also ceases the interest income based on it as well.

The American model takes the incoming funds and, in a simplistic explanation, issues bonds on the money. The Treasury then accounts for and pays interest on the bonds. When the SSA needs cash, it calls a demand on the bonds, and the Treasury returns the cash. The rate of consumption versus the balance + interest + income is where the math gets painful. More is going out than coming in, ergo the eventual insolvency. Does the American model mean in 2034 payments stop? No. More than likely it really means having to apply reduced payments out, but that could be as much as 20 percent plus. For a senior living on a fixed income, this really matters. It's already felt with less-than-desirable cost of living adjustments (COLAs) that don't keep up with inflation. A 20 percent cut would be devastating for many just on the edge and unable to make it up working again.

So, the burden probably will end up on the working. Since few want their withholding "taxes" to go up, bumping the age of retirement is politically easier to apply quickly. Both will likely need to happen by the mid-2030s. And that by default means people have to work longer, work more, and take on extra jobs in their old age. Welcome to the 21st Century.