Bitcoin’s hashprice has spent most of 2024–2025 trading below $0.05/TH/day — roughly half what miners earned before the April halving. In that margin environment, how you get paid matters as much as how efficiently you mine.

Operators with 5–50 PH/s fleets consistently over-index on pool luck when evaluating whether to switch pools. Luck is visible, easy to screenshot, easy to compare. It’s also one of the more expensive analytical mistakes you can make in the current margin environment.

Mining Is a Fixed-Cost Business. Treat It Like One.

Bitcoin mining has hard monthly outflows: power contracts, cooling, hosting, ASIC maintenance, staffing. A 100 PH/s operation at $0.06/kWh doesn’t defer its electricity bill because the pool had a rough luck week.

Pool selection, when made well, is a treasury decision first and a technical decision second.

Pool Luck: Useful Signal, Dangerous Metric

Pool luck is the ratio of expected blocks found to actual blocks found. A pool at 110% found more than the statistical average. At 85%, fewer.

Luck normalizes over time. Across months, every pool converges toward 100%. A 7-day luck chart shows variance — not infrastructure quality. For smaller pools, swings are wider and take longer to mean-revert. If you joined during the hot streak, your comparison window is misleading.

The right question isn’t which pool found the most blocks last week. It’s which pool delivers the most consistent revenue per terahash, at the lowest effective fee, with the most transparent share accounting.

Payout Models as Business Architecture

- PPLNS ties payouts to your proportional share contribution within a trailing window. Identical hashrate, meaningfully different revenue across consecutive weeks — purely based on block timing. For operations with tight liquidity, that’s a real planning problem.

- PPS guarantees a fixed rate per valid share regardless of block timing. The pool absorbs variance and charges a higher fee. It’s insurance on your revenue stream.

- FPPS extends PPS by including transaction fee income in the guaranteed rate — increasingly material since the 2024 halving pushed fee pressure higher. Foundry USA, AntPool, and WhitePool all run FPPS. For large fleet operators, it’s not about getting paid more. It’s about getting paid consistently enough to model forward accurately.

Post-Halving Margin Reality

The April 2024 halving cut the block subsidy from 6.25 to 3.125 $BTC. Hashprice dropped from roughly $0.10/TH/day pre-halving to sub-$0.05/TH/day in the months following, as difficulty kept climbing. Some operators didn’t survive the adjustment.

In that environment, every layer of payout inefficiency is real money. Stale shares, delayed settlements, opaque fees, poorly handled orphan blocks — incremental losses stacked on top of a halved subsidy. A pool introducing 1–2% effective revenue leakage costs you more than a fee differential you’d scrutinize for weeks.

What Payout Reliability Actually Looks Like in Practice

Fee rate gets most of the attention. It shouldn’t. A pool with a 1% fee and unreliable settlements will cost you more than a 2% fee pool that pays daily with full transparency. Here’s what experienced operators check instead.

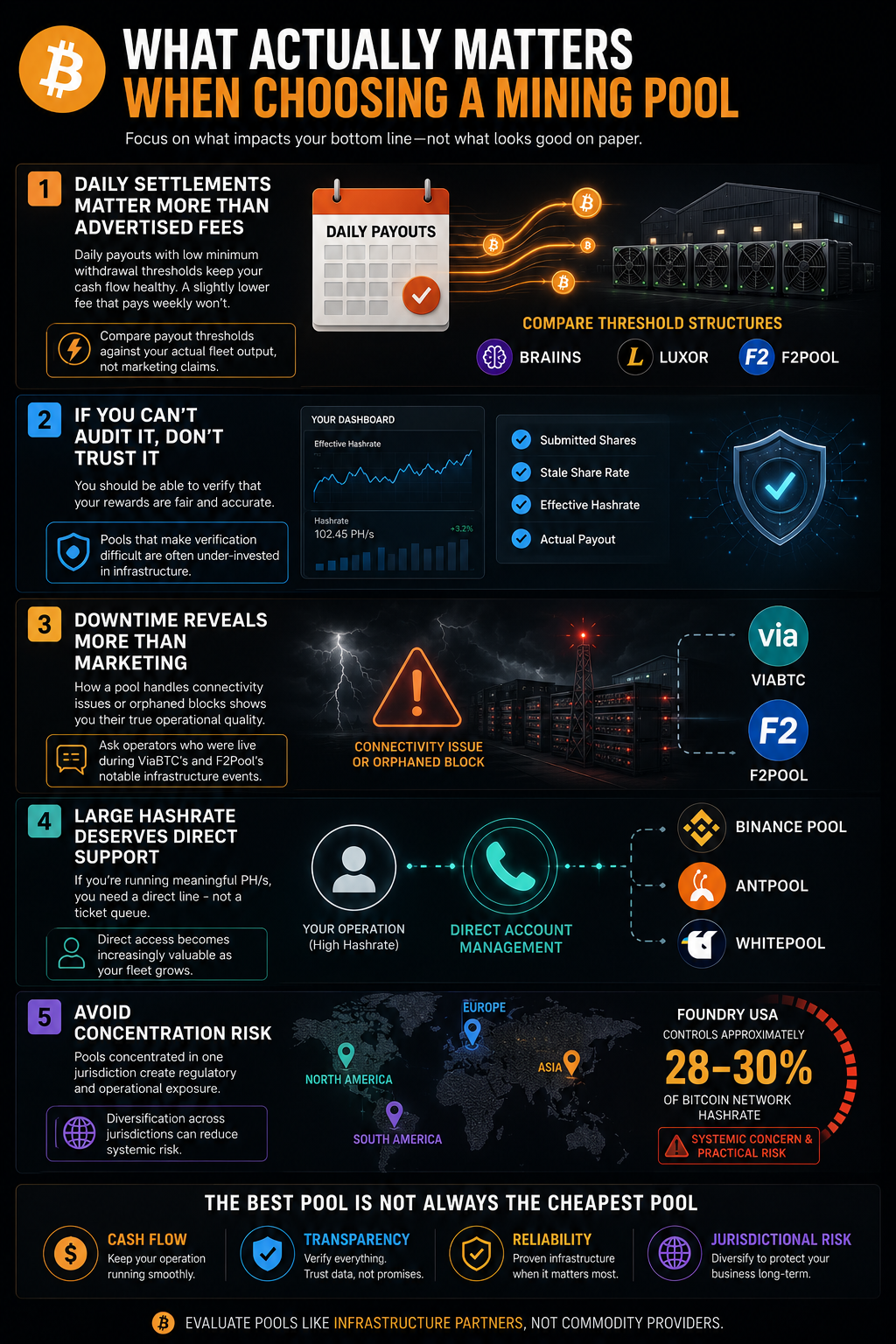

- Settlement frequency and threshold. Daily settlements with a low minimum payout matter more to cash-flow-sensitive operations than a theoretical fee advantage that clears once a week. Compare Braiins, Luxor, and F2Pool’s threshold structures against your actual fleet output.

- Transparency of share accounting. You should be able to audit submitted shares, stale rates, and effective hashrate against your payout. Pools that make this difficult are under-invested in their own infrastructure.

- Incident communication. How a pool handles a connectivity issue or an orphaned block tells you more than any marketing material. Ask operators who were live during ViaBTC’s and F2Pool’s notable infrastructure events.

- Support structure.Binance Pool, AntPool, and WhitePool offer direct account management for significant hashrate. If you’re running meaningful PH/s, you need a direct line — not a ticket queue.

- Geographic and regulatory exposure. A pool concentrated in one jurisdiction carries regulatory tail risk. Foundry USA currently holds roughly 28–30% of Bitcoin’s global hashrate — a systemic concern and a practical risk for operators who want genuine jurisdictional diversification.

The Bottom Line

Pool luck is noise. Payout architecture is signal.

In a post-halving environment where hashprice sits under $0.05/TH/day and difficulty keeps grinding higher, the margin for sloppy infrastructure decisions is gone.

Disclaimer: This is not financial or investment advice. Do your own research before making any decisions. Use at your own risk.