Learn why owning white label crypto cards infrastructure via API is the only way to stop the bleed. Are your users forced to dump your token on Binance just to buy coffee? Discover why relying on third-party crypto off-ramp solutions is draining your ecosystem's liquidity.

Introduction

As the global adoption of digital assets accelerates, white-label crypto cards are emerging as a critical tool for meeting the growing demand for seamless payment solutions. These cards are gaining popularity because they offer an accessible, scalable way for enterprises to provide crypto-enabled payment choices without the prohibitive costs or technical complexities of building a proprietary infrastructure from scratch.

By leveraging ready-to-use card solutions, businesses can bypass the "Renter's Trap"—where liquidity and brand identity are often lost to third-party exchanges—and instead offer a fully integrated financial experience. This article explores the fundamentals of white-label crypto cards, how they bridge the gap between DeFi and daily spending, and the strategic benefits they provide to businesses and users in the evolving Web3 landscape

Let me introduce my friend Alex.

Alex isn't a crypto newbie. He is the founder of Apex-fi, a serious DeFi protocol based in Berlin with $85 Million in Total Value Locked (TVL) and a community of 42,000 active members.

On paper, Alex was winning...but, in reality, his project was starting to bleed...

Despite the high TVL, his ecosystem had a massive leak. Every time one of his 42,000 users wanted to spend their gains in the real world, they were forced to leave the platform, send their tokens to Binance, and market-sell them to get fiat.

Alex call it "The Binance Bleed." He was losing liquidity and crushing his own token price simply because he relied on third-party crypto off-ramp solutions.

He realized he was building an $85M skyscraper on rented land.

This is the story of how Alex made a strategic decision to stop renting. He deployed a White Label Crypto Card Infrastructure package, and turned his biggest operational weakness into his most profitable asset.

The Liquidity Paradox: When your protocol succeeds on-chain with high TVL, but fails off-chain due to a lack of real-world spending utility.

The Bottleneck: The Hidden Cost of Third-Party Crypto Cards

In the early days, to solve the constant "wen utility?" questions, Alex took the easy route. He partnered with a well-known, generic third-party crypto card provider.

It felt like a quick win. He proudly announced to his community: "Look! We finally have our card! Now you can finally spend your yield on Netflix and groceries!"

But the honeymoon phase ended faster than a memecoin rug-pull. The community sentiment went from "Wen Lambo?" to "Wen Refund?" in record time.

Why? Because Alex discovered the expensive truth about "renting" infrastructure:

1. Brand Dilution (The "Generic Wallet" Problem) When users generated their virtual cards and added them to Apple Pay or Google Pay, Alex was horrified. The digital card art on their phone screens didn't feature the elegant Apex-fi branding. Instead, it displayed the partner’s generic, neon-green logo.

-

The Pain: Every time a user tapped their phone to pay for coffee, they were staring at another company's brand, not Alex's. He was paying thousands of dollars to advertise a third-party provider inside his own users' pockets. It looked cheap, rented, and amateur.

2. Data Leakage (Giving Away the Gold) To activate the virtual card, Alex’s users were disappointed cause they were forced to click a redirect link and undergo KYC (Know Your Customer) outside of the Apex-fi app.

-

The Pain: Alex committed the cardinal sin of business: he handed over his user database to a stranger. He essentially onboarded his own users onto another platform. Now, that provider owned the customer relationship (and the email list) and could market competing tokens or services directly to Alex's community.

3. The Freeze (The 72-Hour Nightmare) The final straw came during a volatile market week. The third-party provider, spooked by regulators in a jurisdiction Alex didn't even operate in, hit the panic button. They paused all instant USDT off-ramp transactions.

-

The Pain: For 72 hours, which is an eternity in crypto, users couldn't spend a dime. Alex’s Telegram chat turned into a war zone. Users accused him of stealing funds. Alex was the one getting screamed at, but he was powerless to fix it because he didn't own the "On/Off" switch.

Alex realized that relying on external fiat on-ramps wasn't an infrastructure solution; it was a single point of failure that threatened to kill his $85M protocol.

He needed control. He needed his own rails.

The Branding Nightmare: Without your own infrastructure, your users see a random provider's logo on Apple Pay, not yours. You are paying to advertise someone else.

The Search: Demystifying Payment Infrastructure

Alex, being an engineer, started digging into the mechanics of global finance. He realized that becoming a "bank" was impossible due to the wide regulatory moat.

But he discovered he didn't need to be a bank. He just needed direct access to their infrastructure.

His search terms shifted from "best crypto affiliate card program" to serious infrastructure queries like "API-based card issuing" and "Web3 payment infrastructure", "Best White label Crypto Cards".

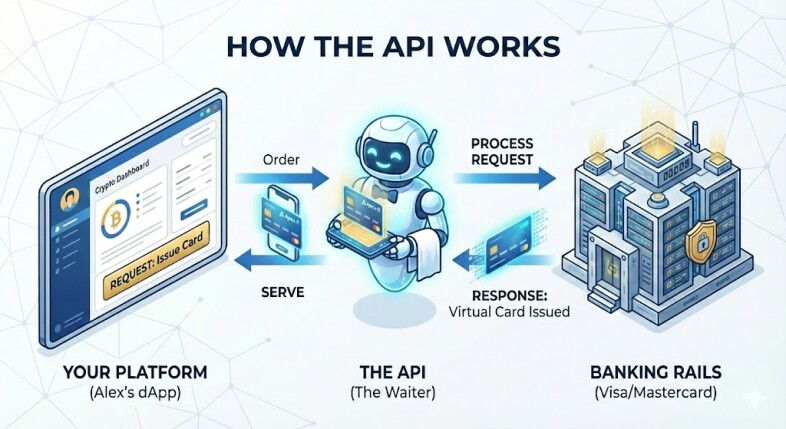

Wait, what is an API? (In Plain English)

If you are not a developer, think of an API (Application Programming Interface) like a waiter in a restaurant.

You (the dApp) are sitting at the table. The Kitchen (Visa/Mastercard Network) is in the back, full of complex rules and heavy machinery. You can't just walk into the kitchen and start cooking; you'd get kicked out.

Instead, you tell the waiter what you want ("I want to issue a card"). The waiter takes your order to the kitchen, the kitchen executes it, and the waiter brings you the result.

In Alex's case, the API is the waiter. It allowed his code to "talk" securely to the banking system, ordering thousands of cards and processing payments without Alex ever needing to touch the banking infrastructure himself.

Little did he know that He would discover a tier of technology providers that most retail users never hear about. These companies had already done the hard work: securing BIN (Bank Identification Number) sponsorships with Visa and Mastercard networks globally.

They weren't offering a consumer product; they were offering "White Label Crypto Cards" as a service. They provided a robust API that would allow Apex-fi to become the issuer of record, programmatically generating virtual cards linked directly to users' on-chain balances, enabling frictionless spending without forcing users through a manual pre-sale of their assets.

The API "Waiter" in Action. It connects your crypto platform to global banking rails instantly.

Note: While visualized here as a physical delivery for clarity, the API generates a 100% virtual card

sent directly to your user's Apple/Google Wallet.

The Paradigm Shift: Owning White-Label Crypto Card Infrastructure

Alex decided to stop playing games. He realized that to scale, he needed to stop renting widgets and start owning infrastructure. He invested in an enterprise-grade white-label crypto card platform (like the solution provided by Toncard).

The difference was night and day. Because he was now using API-based card issuing, the integration took weeks, not years.

Compare that to the 18 months of compliance meetings, lawsuits, and "blood sacrifices" it usually takes to open a direct card issuance program with a traditional bank.

The shift was profound. Apex-fi was no longer asking permission; it was deploying code.

1. True "Branded" Utility (The Apple Wallet Flex)

Now, when an Apex-fi user wanted to spend their yield, they didn't leave the dApp. They clicked "Issue Card," and instantly, a virtual Visa card appeared.

When they added it to Apple Pay and bought a coffee in London or software in New York, the screen didn't show a generic, ugly green rectangle from a third party. It showed the glowing Apex-fi logo.

It’s a small detail, but in Web3, "flexing" your brand in the real world is half the utility. It legitimized the project instantly in the eyes of his users (and his competitors). The implicit message is: this crypto project is really serious.

The "Flex" Factor: Unlike generic solutions, a White label crypto cards puts your brand front and center in your user's digital wallet, building trust every time they look at their phone.

2. Closing the Liquidity Loop (Diamond Hands Mode)

This was the biggest ROI for Alex. Before, spending meant selling the token on a CEX days in advance. Now, the card infrastructure allowed for "Just-in-Time" liquidity.

A user could hold (HODL) their $APEX token right up until the exact second the barista tapped the terminal. Basically, they could have "Diamond Hands" until the caffeine withdrawal kicked in.

For Alex, this meant maximal liquidity retention within his protocol for the longest possible time, helping stabilize the token price against panic dumps.

3. Turning a Cost into Revenue (The "Uno Reverse" Card)

Previously, payment fees were a drain on his users and his treasury. By owning the infrastructure, Alex flipped the script.

Every time a user swiped their branded card, the merchant paid standard interchange fees. Because Alex was now the program owner, a portion of that revenue flowed back to the Apex-fi treasury.

Alex was no longer paying the bank; the bank's system was paying him. It felt like a financial cheat code, but it was just smart infrastructure.

From "Wen Utility?" to Watching Netflix: Frictionless spending means your users can hold your token until the exact moment of purchase, creating "Just-in-Time" liquidity for your protocol. Having your own white-label crypto card is not an option.

Diagnostic: Do You Actually Need a White-Label Crypto Card?

I know that now you might be reading Alex’s story and thinking, "This sounds great, but is it right for my project?"

But you must know this first: Not every crypto project needs its own payment rails. For example, if you just launched a memecoin yesterday with 50 holders, stick to the basics.

However, if you are building a serious ecosystem, whether it's a DeFi protocol, a Wallet, a DAO, or a Play-to-Earn game, relying on generic tools is likely costing you more than you think.

The Crypto Infrastructure "Pain Points." If you identify with the liquidity drain, technical limitations, or data risks shown above, it's a clear sign your project is ready to upgrade to a White-Label Crypto Card solution.

Here is the 4-Point Diagnostic Checklist. If you find yourself nodding "yes" to these problems, it’s time to upgrade to a white-label crypto card solution.

1. The "First of the Month" Liquidity Drop

Do you notice a dip in your Total Value Locked (TVL) or token price at the end of every month?

-

The Problem: Your users are cashing out to pay rent and bills. They are forced to sell your token on an exchange to get fiat.

-

The Fix: With a card program, they can pay rent directly without "dumping" the token. The liquidity stays in your system until the moment of payment.

2. You Are Tired of Donating Your User Data

Are you sending your users to third-party on-ramps/off-ramps (like MoonPay, Transak, or centralized exchanges) to cash out?

-

The Problem: Every time you redirect a user, you are handing your verified customer data to a third party. You are building their business, not yours.

-

The Fix: Owning the infrastructure keeps the KYC and user data inside your ecosystem, increasing your project's valuation.

3. Your Developers Need Custom Logic

Are generic "widget" plugins too limited for what you want to build?

-

The Problem: Maybe you want to issue cards only to users who hold a specific NFT, or you want to offer cashback in your native token. "Out-of-the-box" plugins can't do this.

-

The Fix: This is where API-based card issuing infrastructure becomes essential. It gives your dev team the programmatic freedom to build custom reward tiers, spending limits, and automated issuance rules that fit your specific tokenomics.

4. You Have High Transaction Volume (But Zero Revenue)

Do your users move millions of dollars in volume, but you don't see a dime of the transfer fees?

-

The Problem: You are paying gas fees and exchange fees, but capturing zero value from the payment flow.

-

The Fix: By becoming the program manager of your own card, you tap into interchange revenue. You turn a cost center into a profit center.

The Verdict: If you checked "Yes" on any of the above, you have outgrown the "renter" model. Like Alex, you have reached the stage where integration via API is no longer a luxury—it’s a survival requirement for scaling your economy.

The Business Case: Why Smart Founders Pay for White-Label Solution

You might be looking at the price tag of an enterprise-grade white-label solution (often starting around $25k for setup) and hesitating.

But in the world of high-stakes crypto, speed and ownership are the only currencies that matter. Here is the math that led Alex—and thousands of other founders—to make the switch.

1. The Engineering Argument: Buying Time

Your CTO knows the truth: Building a direct banking integration from scratch requires a team of senior engineers, PCI-DSS certification, and at least 18 months of development.

-

The Math: 5 Senior Devs ($50k/month) x 18 Months = $900,000+ in burned capital.

-

The Reality: Paying for a ready-to-deploy API infrastructure isn't an expense; it’s a discount. You are buying 18 months of R&D for a fraction of the cost, allowing your team to focus on your core product, not banking compliance.

2. The Tokenomics Argument: Protecting Your Market Cap

What is the cost of a 10% dump in your token price because users are exiting to fiat? For a project with an $85M market cap, that is an $8.5 million loss in value.

-

The Reality: By implementing a closed-loop card program, you retain liquidity. Even if the infrastructure costs $25k, saving just a fraction of your Total Value Locked (TVL) pays for the system instantly.

3. The Valuation Argument: Owning the Asset

Investors don't pay high multiples for "wrapper" companies that rely entirely on 3rd party widgets. They pay for companies that own their data and their revenue streams.

-

The Reality: When you own the program, you own the user data and you share in the Interchange Revenue. You are transforming your company from a simple dApp into a Fintech powerhouse.

The white-Label Landscape in 2025: Who is Who in Crypto Card Issuing

Once Alex understood the API model, he had to choose a partner. The market for white label crypto cards has matured rapidly in 2024-2025. It’s no longer a "wild west"; it’s a tiered ecosystem where choosing the wrong partner, specifically one with weak compliance, can kill your project overnight.

Based on infrastructure audits and "Due Diligence" reports, here is how the top players stack up for a Web3 Founder:

Tier 1: The Agile "Web3 Natives" (Best for Speed & Value)

These white-label providers understand that a DeFi protocol handles assets differently than a traditional bank.

-

Striga (The Crypto-Native): Now part of the Lightspark ecosystem, Striga is often the top pick for CTOs who want "Just-in-Time" liquidity without the headache. Their unified API handles custody, crypto-to-fiat exchange, and card issuing in one loop. This sounds magnificent!

-

Best for Projects that need a seamless on-ramp/off-ramp experience natively.

-

-

Wallester (The Budget Friendly): If you are validating an MVP or watching your runway, Wallester is the disruption leader. They famously offer a €0 setup fee model, shifting costs to a monthly SaaS fee.

-

Best for: Startups needing fast execution (accounts in 24h) and low initial CapEx.

-

Tier 2: The Institutional Heavyweights (Best for Scale)

When you have 100k+ users and need global reach beyond Europe, Asia or America.

-

Unlimit (The Global Titan): Formerly Unlimint, they are unique because they are both the issuer and the acquirer. This removes middlemen, improving transaction success rates.

Just imagine this: Your user travels to Brazil or Japan and tries to buy dinner. A generic crypto card might get declined because the issuer lacks local banking connections and flags it as "high risk." With Unlimit’s white label crypto card infrastructure, the transaction is recognized by their local rails. The result? "Transaction Approved" instantly, while your competitors get blocked. That reliability is what enterprise scale looks like. -

Baanx (The Self-Custody King): The engine behind giants like Ledger and MetaMask. Their specialty is non-custodial infrastructure, perfect if your philosophy is "Not your keys, not your crypto."

Now picture that the same user walks into a Starbucks. Their funds aren't sitting on your company's database; they are secure in their self-custody wallet. When they tap to pay for a latte, a smart contract instantly executes a liquidation for the exact amount needed ($5) on-chain. They maintained ownership of their assets until the milk was poured. This is the ultimate "trustless" utility that die-hard crypto natives demand from modern white-label solutions.

⚠️ The Cautionary Tale: The "Intergiro" Lesson

In 2024, Intergiro was a popular choice. By mid-2025, their license was revoked by the Swedish Financial Supervisory Authority (SFSA) due to systemic AML failures. The Lesson: When selecting a Banking-as-a-Service (BaaS) partner, technology is secondary to compliance. If your provider loses their license, your users' cards stop working instantly. Always audit their "RegTech" stack.

Who is Who in 2025. A strategic map of the white-label crypto card ecosystem.

Choose Tier 1 (Wallester, Striga) for speed or Tier 2 (Unlimit, Baanx) for global scale, but always beware of compliance red flags like the Intergiro case.

The Real Cost: Breaking Down the Infrastructure Investment

You might be asking: "Alex paid $25k? But didn't you say Wallester has a €0 setup fee?"

This is where the difference between "sticker price" and "Total Cost of Ownership" (TCO) matters. Whether you pay it upfront (Setup Fee) or over time (SaaS Fees), launching a serious white-label crypto card program requires capital.

Here is the financial breakdown of what a professional integration actually costs in 2025:

1. The Setup Fee (The Barrier to Entry)

-

Budget Option (e.g., Wallester): €0 - €5,000. They lower the barrier to entry to get you started fast.

-

Enterprise Option (e.g., Baanx/Unlimit): $25,000 - $50,000.

-

What you are paying for: Custom legal structuring, complex non-custodial wallet integrations, and dedicated BIN sponsorship. This is the premium tier for established protocols looking for a robust white-label crypto card solution that scales.

-

2. The Monthly SaaS Fee (The Operational Cost)

Even "free setup" providers have to eat.

-

The Cost: Expect to pay between €3,995 and €5,995 per month for a full crypto-friendly VASP license package.

-

Reality Check: Over 6 months, a "free setup" provider will still cost you ~€30,000 in SaaS fees. This validates that $25k is the standard investment for the first phase of any high-tier white-label crypto card program.

3. The Revenue Share (How You Earn It Back)

This is the "Uno Reverse" card.

-

Interchange Fee: In Europe, capped by the EU Interchange Fee Regulation (IFR) , you might share in the ~0.2% interchange fee. In the US, this can jump to ~1%+.

-

The Break-Even: If you negotiate a smart revenue share (often 20%-50% of net interchange), a community with high transaction volume (GMV) can cover the monthly SaaS fees entirely.

The Bottom Line: You can start with a "Budget" option to validate, but if you want custom logic, self-custody features, and high limits, the $25k investment into enterprise-grade white-label crypto cards is not a cost—it is the price of buying your own bank branch.

The "Revenue-First" Approach: Turnkey Ecosystems

While Tier 1 providers offer speed and Tier 2 offers scale, there is a third category emerging in 2025: The Turnkey Fintech Ecosystem.

This model is designed for founders who don't just want "payment rails"—they want a business in a box. Instead of hiring a frontend team to build an app from scratch around an API, solutions like Toncard provide the entire frontend and monetization logic pre-built.

Here is why this "Hybrid Model" is disrupting the market for Media Buyers, Traffic Teams, and Web3 Communities:

1. Native Telegram Integration (The "Super-App" Strategy)

Most providers give you a card. Toncard gives you a Branded Telegram Mini-App.

-

The Advantage: You don't need to force users to download a new

.apkor TestFlight app. Your entire banking interface lives inside Telegram, where your community already spends 90% of their time. This drastically lowers Customer Acquisition Cost (CAC).

2. Built-in Monetization Loops

Standard providers charge you fees. The Turnkey model turns the tables so you earn on every action.

-

The Difference: The infrastructure comes with a pre-configured 5-level affiliate program and cashback systems. You aren't just issuing cards; you are launching a viral referral economy where one active client generates profit daily from top-ups and transactions.

3. Speed to Revenue (3-7 Days)

We mentioned that banking integrations take months. Because the "Turnkey" model uses pre-approved, ready-made infrastructure (like KeyTether.io rails), the time-to-market shrinks to 3-7 days.

-

Ideal For: High-velocity niches like Media Buying (running ads) or Gambling/iGaming where waiting 6 months for compliance is a death sentence.

The Verdict: If you have a dev team of 20, get an API (Tier 2). But if you have traffic and a community and want to monetize them immediately with your own logo and "look and feel", the Turnkey Ecosystem is the smartest capital efficiency play.

The View from the Top. When you stop renting and start owning your white-label crypto card infrastructure, you don't just issue cards, think bigger: you secure your ecosystem's liquidity and more importantly, your sustainability.

Conclusion: From Renter to Owner

Today, Alex isn't just running a DeFi protocol; he is running a self-sustaining economy. The "Binance Bleed" has stopped. His users are no longer exiting the ecosystem to sell their tokens; they are staying within it because they finally have real utility in their pockets.

By deciding to issue branded debit cards directly linked to his protocol, Alex bridged the ultimate gap between on-chain assets and global spending.

This is the strategic advantage of modern white-label solutions. They allow you to stop promoting generic third-party services and finally prioritize your brand, your look and feel. When your users open their digital wallet, they should see your logo, not a stranger's.

If you are serious about liquidity retention and user experience, don't settle for a rented widget. It’s time to launch branded card program infrastructure that turns your project into a fintech powerhouse.

Alex made the shift from renter to owner. The question is: Are you ready to own the rails too?