At the end of the day money is money, but with that said, there is are some very different contexts of money that become important in the implementation of a CBDC. Simply delineating between wholesale money or retail money and public versus private money and a variety of other separations of money usage within an economy does not mean that it requires any sort of separation within the technical infrastructure. Many of the different contexts of money being used within an economy are more likely to be controlled via the use of smart contracts rather than through the specific separation of purposes of that money. So, if we are looking at building a cohesive digital currency ecosystem, we need to be certain how the different layers of that system get represented effectively.

Coming up with a working ‘one currency – one ledger’ model is likely unrealistic and highly disruptive to the existing banking systems. Only in cases where a complete overhaul of a country’s banking system is required should this even be considered. The contexts that we use to separate or pool money, either by Central Banks, banks, governments, corporations or even individuals is possibly a better reason to create isolation of ledgers at the varying layers within the system. Separating purely on wholesale vs retail also doesn’t provide a lot of value to the system.

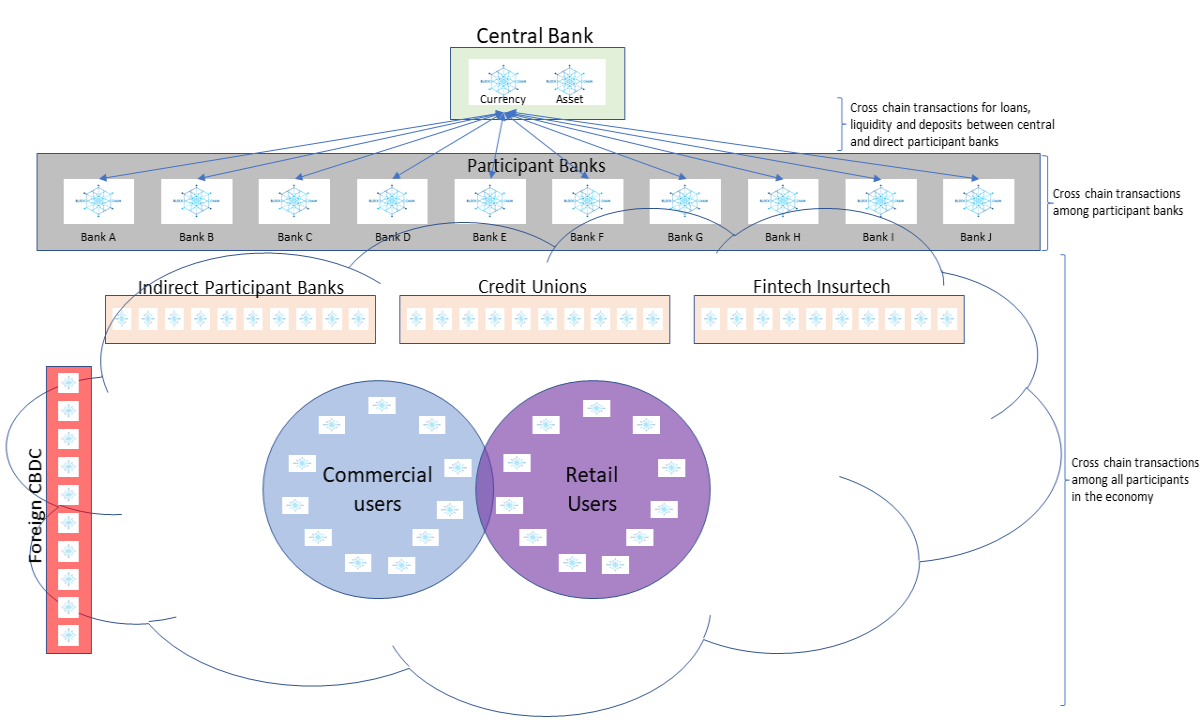

Every tier and every entity in the system should be able to establish their own individual ledger that can essentially operate independently and integrate with other ledgers within the ecosystem to generate deeper value and generate exponential opportunities for innovation. Since we are talking about permissioned ledger solutions here – not decentralized - all transactional activity is instant and secure. The focus is on enabling intra-ledger transactions for communities of users and then cross-ledger transactions for the interactions between those communities. The independent ledger model would look like this:

At the Central Bank level, there is the need for a ledger that can serve as the ledger of ledgers for the body that can issue and tokenize currency value to the ecosystem. Beyond that, each direct participant can either borrow or accept deposits from the Central Bank and each would have their own ledgers and be permissioned for cross-ledger transactions among each other and with the Central Bank. Smaller indirect banks can set up their own ledgers and be permissioned into the ecosystem via one of the direct banks. Wallet end-points for individuals and corporations can be made available that could accept tokenized currency value in the local CBDC and could support carrying tokens of foreign currency value as well.

With modern monetary policy, there are already reasons for a Central Bank to operate multiple ledgers internally besides their fiat currency issuance ledger. As Central Banks continue to leverage asset balance sheets, these assets could be managed and valuated in their own ledger that supports the valuation of the currency. Private bond and debt sales may also justify their own ledgers as these tend to stand separately in support of the fiat currency but don’t involve the CBDC directly. However, defining separate ledgers for things that are directly associated with the fiat currency would just add complexity that a Central Bank does not need. Programmable features of the CBDC will provide all of the contextual flexibility that a Central Bank requires.

The Central Bank ledger would include all of the currency issuance/destruction details, seigniorage backing, liquidity and deposit details with the direct participant banks. This will give the Central Bank all of the same tools and controls that they have over fiat currency, but with the speed and efficacy that is provisioned with programmable currency and smart contracts. As an example, one group already built a working representation of a decentralized currency blockchain supported by a permissioned asset blockchain in the AXIA Coin project. The key variance in a CBDC is that both blockchains would be permissioned. For an existing example of the independent ledger model in operation, take a look at how Nanopay works.

Essentially, there are a myriad of benefits to this model including the independence of organizations, independence of smart contracts and the ability to compete in the programmability layer either within your service offering or across service offerings. All transactional references within each chain are relevant to the party that is holding them and you get the added integrity of validating values across multiple blockchain sources. It also means that P2P, B2B, and P2B transactions can be facilitated in offline, nearline and online modes as available.

Focusing on the core currency, if you feel that there is an opportunity or benefit to moving away from a single ledger solution for CBDCs based on loosely defined contexts of money, then going all the way to an independent ledger solution may make more sense as you consider some of the benefits of data dispersion, operational independence and the need for creating innovative opportunity. The Central Bank really just needs to set the blueprint for the tokens and the base blockchain along with the candidate module that others can take and use. Organizations and FinTechs can then move the capability forward for economic participants.