This is NOT investment advice. Investing in startups is risky whether it is via StartEngine or any of the other platforms. Liquidity may or may not be an option for an extended period of time.

We took a break in July and intended to do so in August. This is an ad hoc post for August in response to news.

Let's see if we can toss out a few names on a monthly basis for people to debate and evaluate and see if this is useful. At times, we have only one name or zero.

The types of firms that typically catch our attention are generally based on seeking a potential "bet a little, win a lot" approach where we seek potential "winner takes all or most" outcomes. We tend to focus on those and avoid battles with low barriers to entry UNLESS the firm is simply executing at a very high level and clearly advancing to a few different potential exits.

First, a couple of recent posts here on this platform:

When is CHECKMATE - Bitcoin Update

StartEngine Raises That Intrigue Us - March 2024

The Submerge - Ether Merge Debacle

Here is what made it through our screening. We committed to screening these monthly and this is the result of the screening for this month. Some of these are repeat names, and that is the way it is. We don't chase new ones simply to pull the trigger. We would rather add to winners.

Perhaps a little blurb about what we will not invest in could be helpful. When seeking a potential "winner takes all" and vice grip lock on certain economic value, we try to be very strict. We have to feel it and understand it. If we don't "get it" in terms of how and why the pieces fit together, then we pass. This can happen frequently with tech, biotech, medical, and retail. We aren't smart enough to know all of these details for each industry and products. If we can't connect all the dots we pass. If the business relies on hype and marketing we pass.

AtomBeam - We've commented extensively already about this opportunity. Our entry is 8M. A+ is ongoing and doing quite well already.

AtomBeam has revenue, albeit from DoD contracts only at this time. This is very positive in our view since the firm could progress through full DoD cycles (granted it can be slow and frustrating) where the contract dollar values are much higher thus providing non-dilutive financing for the company's growth. Yes, there are costs the company must bear to execute the contracts, but it all aligns with the long term strategy and vision. Not to mention DoD might become one of the biggest customers.

Apparently AtomBeam has signed a commercial customer - meaning nothing to do with the U.S. federal government or grants, etc. The company released the name of the customer: Ericsson. Apparently AtomBeam has been working with them for a while, and expectations should be reasonable. They are rolling things out incrementally so refrain from demanding huge revenue boosts immediately. This is a giant client that could lead to all sorts of things so we will continue to be patient.

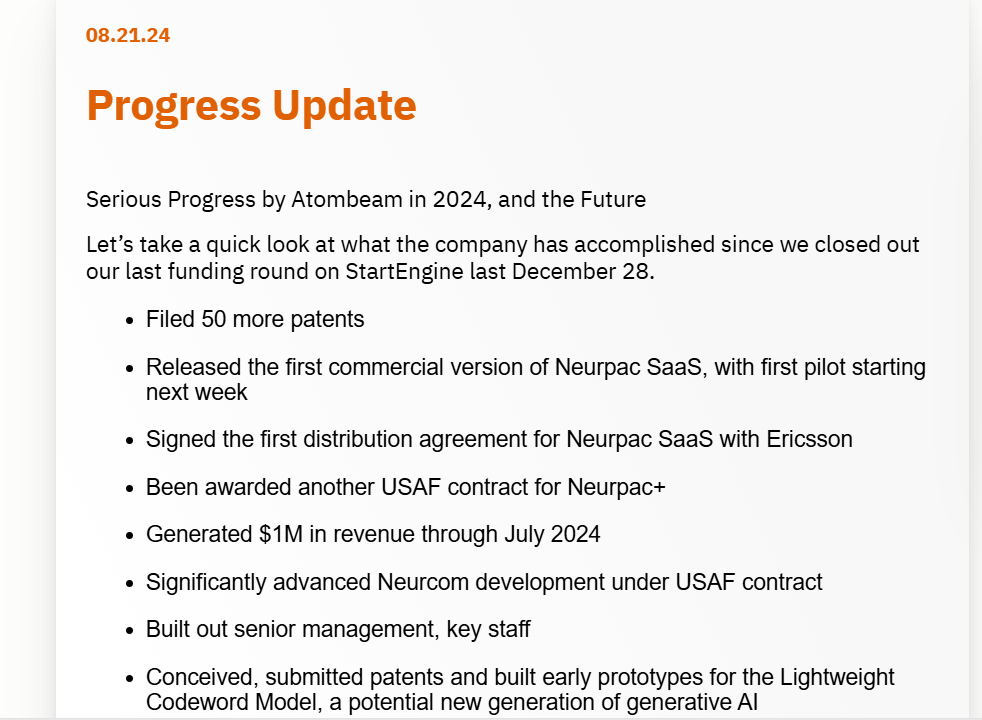

Here is an updated released recently: