There was a time when money was gold. Not metaphorically. Literally. Coins were chunks of precious metal—heavy, tangible, sometimes dirty—and their value didn’t depend on the will of a central bank or the whim of financial markets, but on the weight and purity of the material they were minted from. The gold standard was more than a monetary system: it was a worldview. A way of thinking about value, trust, and the economic order of the world.

People often speak of it with a blend of nostalgia and reverence, as if it were a golden age—and yes, the adjective is ironic—in which money couldn't be inflated at the whims of politicians, and economic imbalances corrected themselves almost automatically. But scratch the surface, and that idyllic vision falls apart, revealing shadows, contradictions, and conveniently forgotten truths.

A Promise of Anchoring in a Liquid World

What makes the gold standard appealing is its promise of stability. By fixing the value of a national currency to a specific quantity of gold, governments were—at least in theory—limited in their ability to print money without backing. Bankers liked that. Capital exporters liked that. Colonial powers, too. Gold was international, apolitical, incorruptible. A standard that allowed no negotiation or sudden devaluations by decree.

The 19th century, especially between 1870 and 1914, was the classical age of the gold standard. Not coincidentally, it coincided with the so-called Belle Époque—a period of imperial expansion, technological progress, and relative peace among the great powers. Looking back, it's tempting to imagine gold as the silent lubricant of that order. But that illusion ignores the other side of the system: its rigidity. To maintain the gold peg, countries had to adjust their internal economies to inflows and outflows of gold. In practice, that meant deflation, stagnant wages, and painful corrections.

In other words: the gold standard worked for capital, not necessarily for people.

When Gold Becomes a Straitjacket

Crises test dogmas. During the Great Depression, the gold standard proved more of a trap than a refuge. As international trade collapsed and banks fell like dominoes, the insistence on maintaining convertibility into gold worsened the pain. The UK abandoned the system in 1931. The U.S. held on until 1933, when Roosevelt made the political—and deeply symbolic—decision to suspend convertibility for citizens.

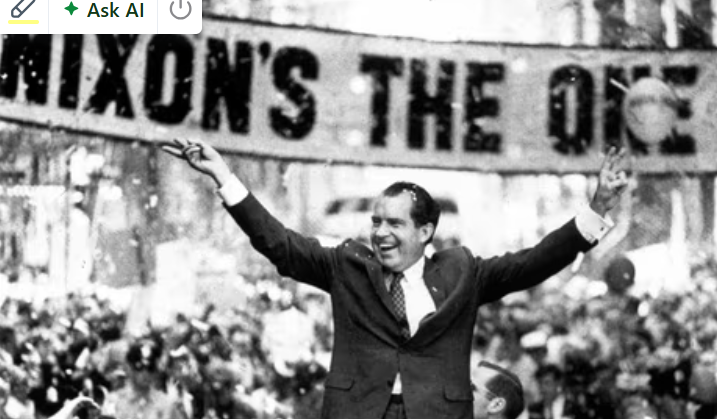

What followed was a redesign of the global monetary system, culminating in the 1944 Bretton Woods agreements. A kind of indirect gold standard: currencies were pegged to the dollar, and the dollar to gold. But even that setup was unsustainable in a world of growing capital flows, military spending, and structural imbalances. Nixon officially dismantled it in 1971 with a gesture that, although technical in appearance, changed history: he closed the “gold window,” ending the tacit agreement that money had to be backed by something physical.

Since then, we’ve lived in a regime of pure fiat money. That is, money by trust. Or by faith.

The Gold Standard as an Idea That Won’t Die

And yet, the gold standard doesn’t die. Not completely. It resurfaces cyclically, like a ghost haunting libertarian forums, Austrian economists’ arguments, and the more skeptical corners of the crypto ecosystem. Every time there’s an inflation crisis or a loss of faith in central banks, someone waves the golden flag. “Return to gold,” they cry, as if the problem were merely a lack of anchoring, as if a shiny metal rod could restore monetary sanity.

But that nostalgia misunderstands—or chooses not to understand—that gold isn’t neutral. Its distribution is unequal. Its extraction comes with environmental, geopolitical, even human costs. Returning to the gold standard would mean a brutal loss of autonomy for economic policy. And, ultimately, what people long for isn’t gold itself but the idea of a predictable world governed by clear rules and physical limits. A longing that reveals more about today’s anxieties than about the virtues of that old system.

One Last Digression (or Warning)

Sometimes I wonder if the gold standard survives not because it was better, but because it’s not here to disappoint us. Like an ex we idealize over time: no longer facing their flaws daily, we attribute to them virtues they never had. Meanwhile, we live with a fiat system that—with all its flaws—gives us more flexible tools to adapt to a changing world. Even if that means risk. Even if confidence sometimes wavers.

Maybe the problem isn’t that we abandoned gold. Maybe the problem is that we still don’t quite know what to put in its place.