The Early Years: From Piggy Bank to Fixed-Term Deposits

As a kid, I loved saving money. Every birthday or holiday, I’d quietly stash away the cash gifts from my parents and relatives. Over the years, the pile grew—until one day, I proudly showed my parents the small fortune I’d tucked away. Shocked at first, they were soon proud of my quiet discipline. That led to my first real step into finance: opening a savings account.

My dad took me and my little stash to the bank, where we opened my first savings account—a fixed-term deposit. My money was locked for two years. As a kid, I couldn’t believe I could earn money by just letting it sit there. This was my first real lesson in patience paying off.

In this article, I’ll share my journey and lessons around:

- Starting with savings accounts, deposits, and interest strategies

- Moving into mutual funds, cooperative shares, and finally ETFs

- Building a diversified ETF portfolio and rebalancing it over time

- Navigating German tax rules for accumulating vs. distributing ETFs

- Experimenting with riskier assets like crypto and peer-to-peer lending

- Developing the mindset to stay calm and consistent during market crashes

Learning to Optimise: Interest Hopping and Deposit Laddering

As interest rates declined and I needed more flexibility, I moved to an instant access savings account—still offering some yield but without the lock-in period. This opened the door to a strategy I later learned was called “rate hopping”: shifting funds between banks to chase the highest interest rates available at the time.

Then I came across fixed-term deposit laddering, a way to better balance liquidity and yield:

- €1,000 for 6 months

- €1,000 for 1 year

- €1,000 for 2 years

- €1,000 for 4 years

Each tier had different yields, and as terms expired, I could either reuse or reinvest the funds. It gave me structure and efficiency. These were small but meaningful steps that helped me better understand how to manage time horizons and optimize cash.

First Investing Lessons: Mutual Funds and Cooperative Shares

When I turned 18, I found out my parents had invested in mutual funds recommended by someone at my dad’s reputable company. Unfortunately, they underperformed the market. I had a few shares worth around €1,000 to €2,000, held them for a few years, and eventually decided to reinvest the funds into better, lower-cost products.

Around the same time, I learned I also owned cooperative shares—offered by local banks or co-ops. They paid decent interest for a while, but then the payouts stopped. Since these came with risk too, and weren’t very liquid, I sold them and redirected that money into more diversified and stable investments.

These early experiences taught me two key things: performance matters, and fees and transparency are crucial when choosing investment products.

Discovering the Stock Market: The ETF Revelation

I became curious about the stock market. I spent years reading about mutual funds, investment strategies, fund managers, and historical performance. But before I invested, I stumbled across something better suited to my personality and goals: exchange-traded funds (ETFs).

As someone who values simplicity and cost-efficiency, ETFs were a revelation. They gave me broad market exposure with much lower fees. I also learned that even most professionals fail to beat the market consistently in the long run. I didn’t want to gamble or guess—I wanted steady, long-term growth without high fees eating into my returns.

Why I Avoid Individual Stocks

I’ve never been drawn to individual stocks. Building a diversified portfolio this way felt like too much work—and risk. What if I picked the wrong stock? A black swan event, a scandal, bad management, or even bad press could wipe out a holding—even if the sector or index overall remained stable.

I preferred broad, diversified exposure. ETFs aligned better with my values: low risk, broad diversification, and minimal effort over the long haul.

Building My ETF Portfolio

ETF Selection

At the time, All-World ETFs weren’t yet common. So I created my own combination:

- MSCI World (~1,500 companies, developed markets)

- MSCI Emerging Markets (~1,400 companies, developing markets)

- STOXX Europe 600 (600 companies across 17 European countries)

- Bloomberg Energy and Metals Equal-Weighted Index (Commodities: 10–15 energy and metals futures contracts)

I added the Europe ETF to reduce the MSCI World’s US-heavy tilt—moving closer to a GDP-weighted allocation.

Portfolio Allocation

I structured my portfolio like this:

- 50.4% World

- 12.6% Europe

- 27% Emerging Markets

- 10% Commodities

This mix gave me broad exposure across geographies and asset classes—without overcomplicating things. I started small at the end of 2015 and scaled over time.

How I Invested: Gradual and Consistent

I was new and cautious. So I began with automated monthly investments into my ETF mix—a technique called dollar-cost averaging. It helped reduce the impact of market volatility and gave me peace of mind.

As I earned more and gained confidence, I increased my contributions significantly. I lived below my means and directed a large portion of my savings into this plan.

I rarely checked my portfolio. I trusted my system and intended to hold for decades.

Rebalancing the Portfolio

Over time, some ETFs outperform others, causing allocation drift. Rebalancing helps keep risk levels aligned with your plan. My approach was straightforward:

Whenever a fund deviated by more than 5–10% from its original weight, I rebalanced to restore it. This usually happened once or twice a year, depending on performance differences.

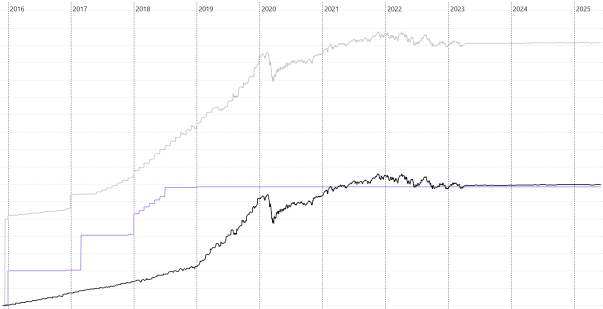

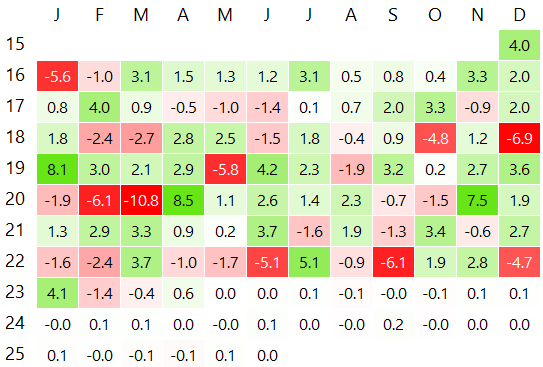

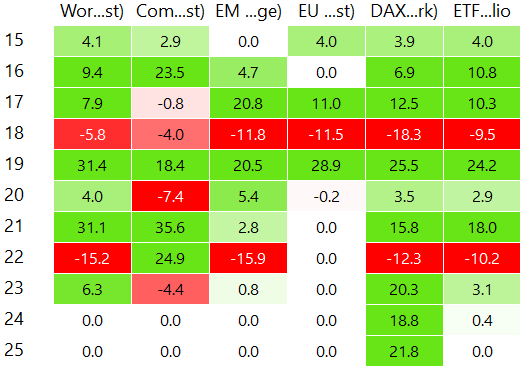

The Results

Here’s what the performance looked like over time:

- Image 1 - Absolute performance

- black: ETF portfolio

- purple: savings account

- grey: both combined

- (data of savings account not updated sinc 2018)

- (error in data since 2023)

- Image 2 - Monthly Returns of ETF Portfolio

- (Error in data in since 2023)

- Image 3 - Yearly Returns for:

- MSCI World

- Emerging Markets

- Europe

- Commodities

- DAX (benchmark)

- Full portfolio

- (Error in data starting from 2023)

Tax Optimisation in Germany: Accumulating vs. Distributing ETFs

Before 2018, German tax law made accumulating ETFs more attractive. These reinvested dividends and were taxed only upon sale (especially if domiciled outside Germany). In contrast, distributing ETFs triggered annual taxes on paid dividends.

This meant that by choosing accumulating funds, you could defer taxes and maximize compounding—unless you wanted to use the Freistellungsauftrag (tax exemption limit of €801/year). If unused, this tax-free allowance went to waste.

In 2018, however, reforms changed everything. Now, both types of ETFs are treated equally, and “phantom” taxation applies to accumulating ones as well. As a result, the difference is mostly gone. Today, choosing between accumulating and distributing ETFs is more about preference than tax strategy.

Dipping Into Higher-Risk Assets

I experimented—cautiously—with some higher-risk investments:

- Shipping containers: Promised 10–20% returns but didn’t feel trustworthy, so I exited quickly.

- Peer-to-peer lending: Initially offered ~12% returns, now averaging closer to ~9%. It’s a small part of my portfolio.

- Cryptocurrency: I dipped into Bitcoin with an amount I was willing to lose. Luckily, it performed well.

These riskier assets remain a minor slice of my overall investment pie.

Getting Into Trading (Briefly)

Later, I explored swing trading—an approach focused on short- to medium-term price movements.

At first, technical analysis seemed like nonsense. But over time, I understood it as a way to work with probabilities. I even built a Python tool to test strategies and log performance.

That opened up a whole new rabbit hole—trading and strategy development. But that’s a topic for another time.

Emergency Funds: The Financial Safety Net

Before diving deep into investing, I made sure I had an emergency fund—three to six months’ worth of living expenses. It’s not an investment; it’s a buffer.

If something unexpected happens—job loss, car repairs, health issues—I don’t need to touch my ETF portfolio. I keep it in a highly liquid savings account. Knowing it’s there helps me stay calm and invested through market turbulence.

Mindset During Market Crashes: Staying the Course

Market crashes are inevitable. What matters is your mindset.

When I started investing, I mentally prepared for downturns. I avoided daily portfolio checks and focused on long-term goals. When COVID hit or markets dipped due to geopolitical events, I didn’t panic—I kept buying through automated monthly investments.

Crashes became opportunities, not threats. My mindset: over decades, markets rise. The dips are just bumps on a long upward slope.

Key Takeaways From My Investing Journey

- Start small, start early: Even saving birthday money got me thinking long-term

- Be curious and take your time: Learn before you commit

- Use laddering and rate-hopping: Maximize returns from your cash

- Keep it simple: Low-cost ETFs are effective long-term tools

- Avoid emotional investing: Stick to rules you set

- Mutual funds ≠ better: Watch the fees

- Automate your investing: Dollar-cost averaging works

- Know your taxes: Tax planning matters

- ETFs are your ally: Diversified and efficient

- Skip stock picking (unless you’re really into it)

- Stick to the plan: Don’t chase trends

- Try riskier assets carefully: Small, experimental exposure only

- Keep an emergency fund: Your financial safety net

Final Thoughts: Keep It Simple, Take Your Time

Looking back, I’m proud of how far I’ve come—from piggy banks to ETFs. I moved gradually, learned continuously, and always valued discipline and simplicity. I ignored hype and trusted what I could understand.

If you're just starting: Keep it simple. Stay consistent. Begin now. Start small if you need to—but just start. Let time and compounding do the rest.

You don’t need brilliance to invest well—just curiosity, patience, and a steady hand.