Goldman Sachs made a lot of unintended negative headlines in the cryptocurrency community when it delivered a presentation to some of its clients on May 27. It included five reasons why cryptocurrencies, including Bitcoin, are not an asset class. In this post, I'll examine each of those reasons, and explain why they are not very convincing to me.

Reason #1 - Cryptocurrencies do not generate cash flow like bonds

Photo by Ethan Wilkinson on Unsplash

This was an odd reason given in the presentation, because a few slides earlier, the presenters compare securities with gold. Intuitively, this validates gold as an asset class. Most investors are not able to generate cash flow from the gold bullion they own, easily making Reason #1 invalid.

What about bullion banks you might ask? For the purpose of this presentation, my assumption is the target audience was retail investors because it was authored by Goldman Sachs's Consumer and Investment Management division. Because of this, it's perfectly reasonable to say that gold is recognized as an asset class, but it does not generate cash flows for retail investors. Reason #1 is not a good one.

Reason #2 - Cryptocurrencies do not generate any earnings through exposure to global economic growth

Photo by Markus Spiske on Unsplash

I'm going to refer to their Reason #1, and say that bonds are an asset class that does not generate any earnings through exposure to global economic growth. Reason #2 is also not a good one in my mind.

Reason #3 - Cryptocurrencies do not provide consistent diversification benefits given its unstable correlations

Photo by sheri silver on Unsplash

It's well known that cryptocurrencies are considered to be high-risk investments due to their volatility (also noted by Goldman in their Reason #4 that will follow). Because of this, most investment advisors recommend diversifying by allocating no more than 3%-5% of your investment portfolio to high-risk securities. Reason #3 is flawed, since it goes without saying that retail investors should not allocate more than 3%-5% of their portfolio to cryptocurrencies, unless their tolerance for risk is much higher.

But I would also like to take a moment to point out that Bitcoin has outperformed the S&P 500 between 2013 and 2019. This point alone makes Reason #3 look a bit foolish.

Reason #4 - Cryptocurrencies do not dampen volatility given historical volatility of 76%

Image by Mediamodifier from Pixabay

The first part of this argument is that investments that are volatile do not make an asset class. The second part of this reason is that Goldman points to Bitcoin's 37% drop in price in a single day as evidence of its volatility.

Let's look at the first point, and examine historical volatility of something that Goldman should be familiar with...the Dot Com Bubble. I decided the historical volatility of the NASDAQ Composite from 1995 to 2005 would mirror the 11-year life of Bitcoin. The audience of the presentation should notice that a footnote in Goldman's presentation actually refers to Bitcoin's historical volatility between December 31, 2014 and May 23, 2020 to be what the 76% value refers to, and not cryptocurrencies in general, so the information on the slide can be misleading unless you read the fine print.

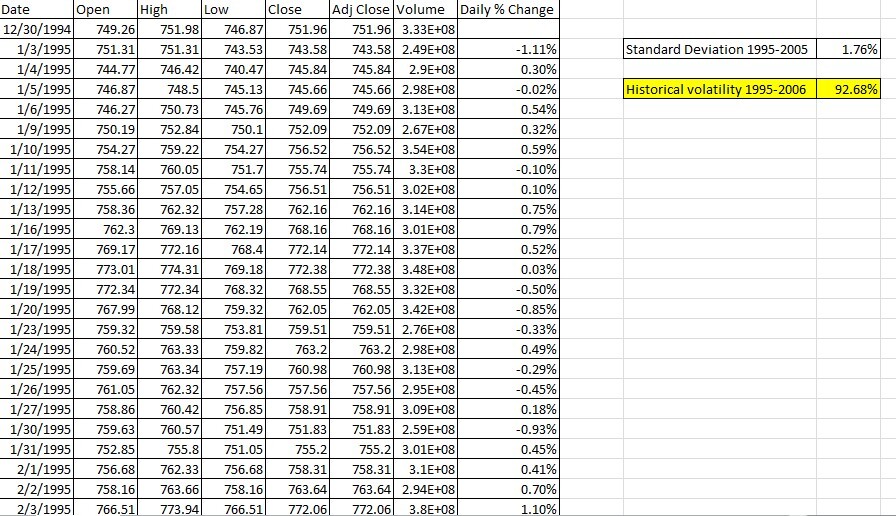

I downloaded the NASDAQ Composite data, and I included a screenshot of my data below:

Screenshot: NASDAQ Composite from 1995 to 2005

Here are the formulas that I used:

Standard Deviation 1995-2005

=STDEVA(H3:H2773)

Historical volatility 1995-2005

=STDEVA(H3:H2773)*(SQRT(COUNT(H3:H2773)))

This discovery actually shocked me, because the NASDAQ Composite's historical volatility from January 3, 1995 to December 30, 2005 works out to 93%! Based on Goldman's logic, investors of the NASDAQ Composite during the Dot Com Bubble were actually exposed to more volatility than individuals who bought Bitcoin!

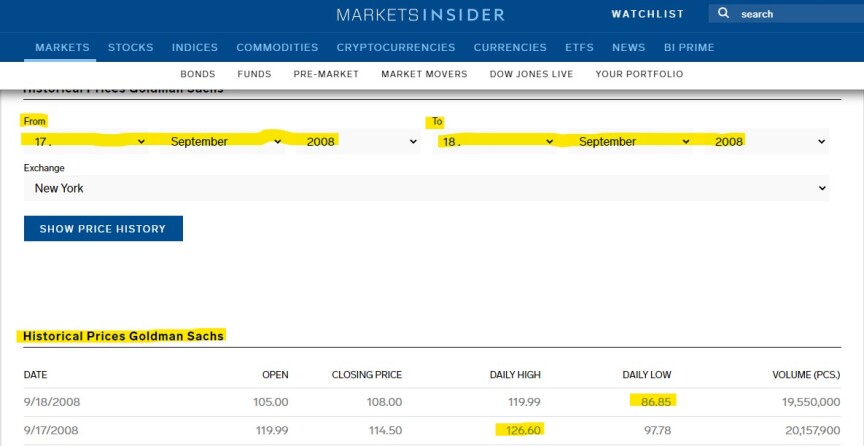

So how do stock prices compare in terms of single-day volatility, which covers the second part of Reason #4? I can confirm that Goldman Sachs themselves are not immune from large single-day drops in value (Ticker: GS). On September 17, 2008, Goldman Sachs's stock price reached an interday high of $126.60 on the NYSE, then plunged to an interday low of $86.85 the following day.

Source: Markets Insider - Goldman Sachs Historical Price - Sept 17 & 18, 1987

This represents a single-day drop of 31%, which isn't far from the 37% that Bitcoin suffered in March.

Hold on...does that price drop span two market trading days? Yes it does, but that price drop spans a period of 24 hours in my mind. Maybe Goldman should point out that the crypto market doesn't have a closing bell to stop trading. I'm simply pointing out that I'm trying to be transparent about my data collection process, and that it's also sometimes difficult to make an apples to apples comparison.

Reason #5 - Cryptocurrencies do not show evidence of hedging against inflation

Image by Gerd Altmann from Pixabay

Admittedly I don't follow all cryptocurrencies, so I will focus my rebuttal on the performance of Bitcoin.

I used coinmarketcap.com to retrieve my data. Unfortunately, the earliest data available for Bitcoin was from April 28, 2013*. I then calculated annual gains from January 1 to December 31 for each calendar year. You can also see the performance of a $100 investment on April 28, 2013, and also on each successive January 1 from 2014 to 2019.

Bitcoin yearly percentage change from 2013-2020*

Source of Bitcoin pricing: Coinmarketcap

By comparison, the annual inflation rate in the US since 2013 ranged between 0.73% to 2.28%. Let's look at the table above more carefully. Since 2013, the only year in which Bitcoin would not have performed well as a hedge against inflation was 2018.

But what about the -59% yearly change in value experienced resulting from 2014 you ask? If the Bitcoin buyer was a HODL'er, however, then that individual would have recovered their losses by 2017. In fact, their $100 purchase on January 1, 2014 would be worth $933.39 if they continued to HODL until January 1, 2020.

And what about the 72% drop in 2018? Well, nothing is perfect. 😉

Does Bitcoin perform well as a hedge against inflation? My calculations above use the same methodology that many investment banks use when promoting mutual funds, and they indicate that Bitcoin does this job quite well, despite it's relatively short lifespan to date. I'm not sure how Goldman determined there is no evidence of hedging against inflation.

Reason #5.5 - Cryptocurrencies are primarily dependent on whether someone else is willing to pay a higher price for it

Goldman also stated in the presentation, "We believe that a security whose appreciation is primarily dependent on whether someone else is willing to pay a higher price for it is not a suitable investment for our clients,". I included this as Reason #5.5 because it's one of the most frequently heard criticisms against the crypto industry. I'm a bit tired of this, so I'll respond with two rebuttals.

Firstly, the expectation that someone will pay a higher price than the previous purchase price is a common reason why many individuals buy antiques, art, or even sports memorabilia. These are all asset classes that the insurance industry caters to, and they all also have industry-accepted methods of value appraisal.

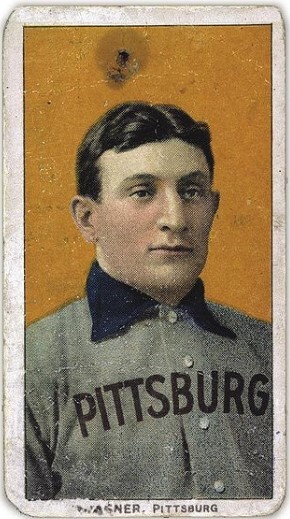

For instance, some people would laugh that an image of an athlete on a piece of cardboard would be highly sought after. But it's well known that many collectors are willing to pay a lot of money for some of these items.

Source: Wikipedia - Published by the American Tobacco Company. Photograph by the National Baseball Hall of Fame and Museum. - Cropped from http://events.mnhs.org/Media/Images/Events/2281/1800_Honusbbcard_300.jpg

A 1909 Honus Wagner rookie card in good condition can fetch $300,000 in the open market. In particular, one that is in near-mint condition has been chronicled frequently because it has soared in value over the past 30 years:

- Purchased in 1991 for $451,000

- Purchased in 1995 for $500,000

- Purchased in 1996 for $640,000

- Purchased in 2000 for $1.265 million

- Purchased in 2007 for $2.350 million

- Purchased in 2008 for $2.800 million

In fact, it is valued to be worth more than $3 million today. Not bad for an investment that depends on waiting for someone else to pay a higher price to acquire it!

Secondly, I'll refer to a quote from Robert Herjavec, of Shark Tank fame.

There's a great movie called The Tulip Wars, and these guys are selling tulip bulbs, and the kid says "Why is it worth, this....", and the guy says to him, "Well because someone is willing to pay for it,".

So why is cryptocurrency worth what it is, is it's because someone's willing to pay for it, - Robert Herjavec on BNN Bloomberg in 2017

The bottom line is that there will be markets where something scarce will rise in value because someone is willing to pay for it. Another way to look at it is one person's garbage is another person's treasure!

Final verdict?

I think it's pretty clear that Goldman Sachs didn't do their homework before creating their presentation.

Thanks for reading!

Good luck, and stay safe!

Cover art by JESHOOTS.COM on Unsplash (cropped)

{kind=link}