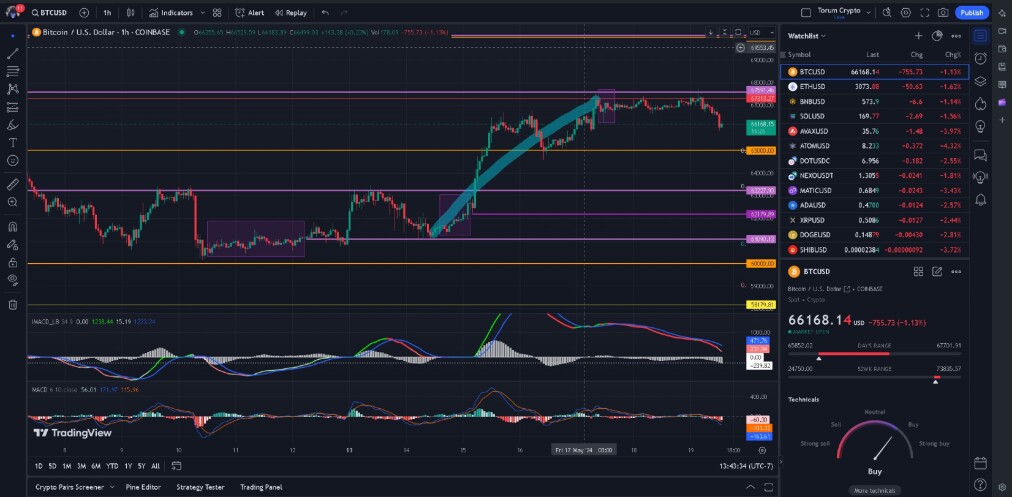

Last Thursday's Analysis Partially Played Out

In my analysis last Thursday, I had anticipated that the market would break through the Fibonacci swing high at 67,313.27 and the old consolidation line from March 18th. This would have cleared the way for further upside momentum.

However, while we did see follow-through from the previous day's strength early on Thursday, the rally stalled out right at the Fibonacci swing high. The market was unable to break through that key Fibonacci resistance level and the old consolidation line at 67,313.27 and 67,591.46 respectively.

Instead of a clean breakout, we formed a long consolidation range over the past few days, trading in a tight range just below that major resistance zone. The market appears to have met a buying barrier that is capping upside for now.

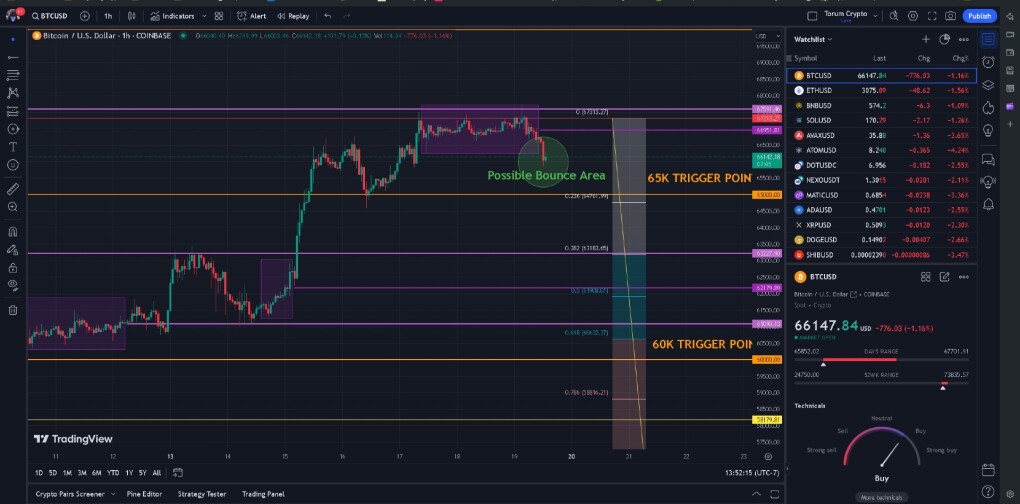

Looking Ahead to a Bounce

My focus now turns to the support level we are currently testing in the 66,339.66 area. This was a previous resistance zone that had the potential to act as a floor for prices. If this support can hold, I'm hopeful we may get a bounce that finally allows us to break through the 67,313.27 swing high and the old consolidation resistance.

A clean break above 67,591.46 would clear the way for further upside towards the next major resistance levels around 70K where we have once again a consolidation line and Tigger/Profit line. However, if 66,339.66 fails as support, we could see a pullback towards the 63,183.65, area next.

While the past few days of consolidation were not exactly as anticipated, the key levels are still holding true. Let's see if buyers can regain their momentum from this current support zone. As always managing risk remains crucial in this volatile crypto environment, which we all love so much.