Even the Federal Reserve officials are sounding the alarm on the alarming trend, where investors are moving away from the U.S. as the safest place to invest.

Although the U.S markets closed this week on a solid note, the underlying turbulence caused by the tariff war is evident. Stocks rose Friday afternoon (April 11) on comments from the White House that President Donald Trump is “optimistic” China will seek a deal with the U.S. Nevertheless, the situation remains very fluid and evolving. Just for context, the baseline tariff rate remains 10% for most countries, but Washington has opted to slam Beijing with a 145% levy.

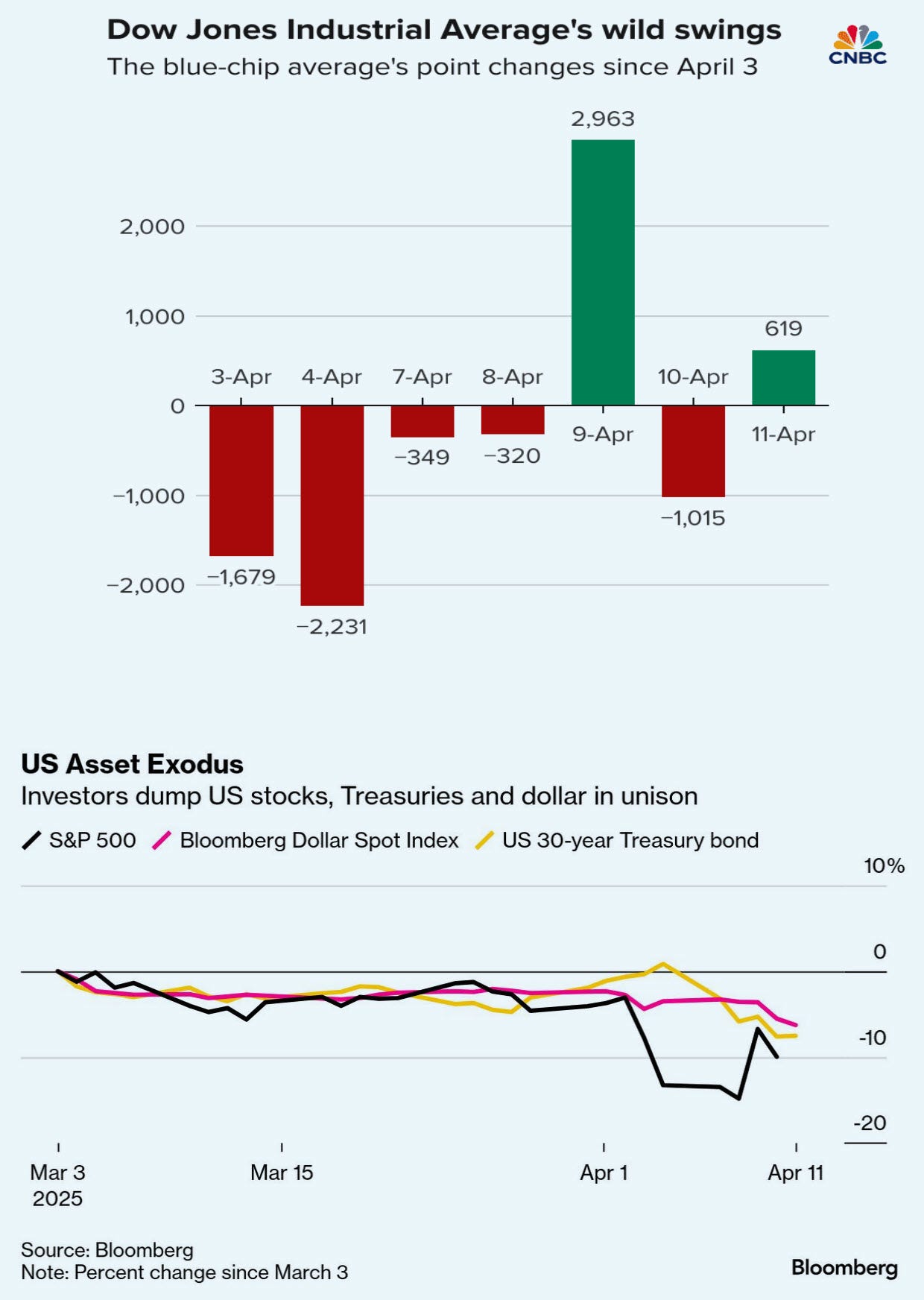

Wall Street experienced an exceptionally turbulent week, marked by significant price swings (top chart below). A sharp downturn hit major indices on Thursday as investors retreated from risk, largely due to uncertainty surrounding trade policy. This erased a substantial portion of the impressive gains seen on Wednesday, which followed President Trump's announcement of a 90-day delay on some of his proposed tariffs. The CBOE Volatility Index (VIX) reflected this instability, initially surging above 50 before settling around 37 by Friday afternoon.

Broader U.S Asset Exodus

Despite a robust final week that saw the S&P 500 gain 5.7% (its best since November 2023), the Nasdaq surge 7.3% (its strongest since November 2022), and the Dow climb nearly 5%, the overall trend for U.S. assets over the preceding five weeks reveals a worrying "asset exodus."

As the bottom chart (below) illustrates, the S&P 500, the Bloomberg Dollar Spot Index, and the price of the US 30-year Treasury bond have all experienced significant declines since March 3, 2025, indicating a broad move away from these key U.S. markets.

This downward pressure, coupled with concerning economic data like U.S. consumer sentiment, suggests that the recent positive weekly performance may be a temporary reprieve within a larger context of investor unease and a significant outflow from U.S. assets. Let’s zoom in on two of the traditional safe haven bets to see a clearer picture - US Treasury bonds & the US Dollar.

Treasury Yields Climb

Fuelled by President Donald Trump's unpredictable trade actions that triggered a move out of U.S. assets and into global safe havens, the 10-year Treasury yield continued its sharp weekly ascent on Friday. The benchmark yield gained more than 17 basis points, reaching 4.567% – its highest level since February 13. The 30-year Treasury yield also saw an increase, climbing to 4.877%.

Traditionally viewed on Wall Street as an exceptionally safe, risk-free asset, U.S. Treasury bonds have historically provided a refuge for investors during periods of market panic, demonstrating resilience during events like the global financial crisis and even a U.S. credit downgrade. However, President Donald Trump's escalating trade war is challenging their long-held position as the world's primary safe haven.

Recent market movements reveal a surge in longer-term Treasury yields and a weakening dollar. A particularly concerning trend is the synchronized trading of Treasuries with riskier assets; investors are selling and buying them at the same time as stocks and cryptocurrencies. This correlation implies that Treasuries are behaving more like a risky asset themselves, with potentially far-reaching implications for the global financial system.

A circulating theory among analysts suggests that China and Japan appeared to be selling Treasurys amid the heightened trade tensions. This selling by the two biggest holders of U.S debt may be contributing to the recent rise in 30-year yields, though concrete evidence is lacking. Furthermore, there is debate whether China might resort to further offloading of U.S. debt as a retaliatory measure against substantial American tariffs.

Weakening Greenback

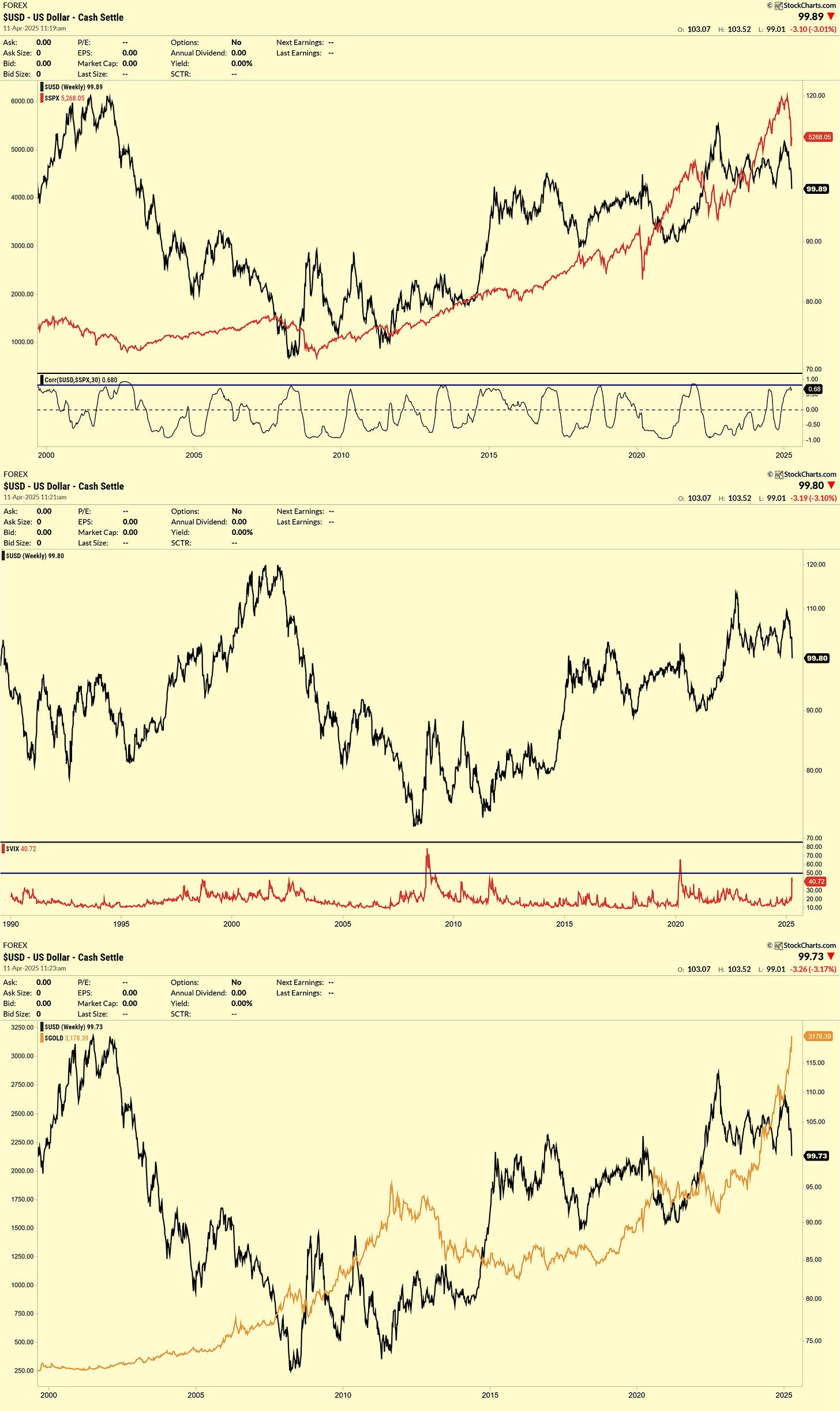

➤ DXY-SPX Correlation: The simultaneous decline of the U.S. dollar and the S&P 500, marking their first positive correlation (at 0.66) in months (Chart 1, above), points to a potential "structural risk-off" environment rooted in macroeconomic stress. With the DXY failing to hold above 106-107 and the SPX pulling back from roughly 5300, this synchronized movement is atypical, as these assets usually act as offsets.

This unusual correlation suggests investors are potentially exiting both markets. This could be due to a "flight to cash," indicating extreme risk aversion and a move towards safer assets, or a "broad-based macro repricing," reflecting a simultaneous reassessment of interest rate expectations and the global economic outlook, negatively impacting both the dollar and equity valuations. Historically, such strong correlations between these assets tend to be short-lived and followed by sharp reversals.

➤ Surging VIX, Falling USD: The unusual lack of strength in the DXY amid a sharp rise in volatility (VIX) signals a potential departure from historical crisis responses (Chart 2, above). This suggests that the market may view current risks as distinct from past events or that the U.S. dollar's status as an automatic safe haven is being questioned.

If the DXY's downward pressure persists while the VIX stays high, a break below critical support levels for the dollar index could occur, reinforcing the idea of a fundamental shift in intermarket leadership. This break in the traditional inverse relationship between these two indicators could imply a structural weakening of the USD, a preference for alternative safe havens like long-duration bonds, gold, or physical cash, or even point to underlying liquidity stress or market dislocations affecting typical asset correlations.

➤ Gold Dominance: Historically, a clear and consistent inverse relationship has linked the performance of the U.S. dollar and gold across various economic cycles (2001, 2008, 2020): a weaker dollar typically led to stronger gold prices, a dynamic largely explained by gold's pricing in USD. However, since 2022, this traditional correlation has experienced a partial breakdown.

Notably, gold has maintained a strong upward trajectory even during periods of dollar strength, especially between 2023 and 2025. This indicates a significant shift, suggesting that gold's appreciation is no longer solely reliant on a weakening dollar. This evolving behavior could be attributed to factors such as anticipated structural inflation, increasing skepticism towards traditional financial assets, and the strategic build-up of gold reserves by non-Western central banks.

Warning Shots & Changing Dynamics

Minneapolis Federal Reserve President Neel Kashkari observed on Friday that investor behavior is indicating a shift away from viewing the United States as the premier safe-haven investment destination amid escalating trade tensions under President Donald Trump's administration.

"Typically, substantial tariff hikes would be expected to strengthen the dollar. The concurrent weakening of the dollar adds weight to the narrative that investors are changing their allocation preferences," Kashkari said.

A confluence of intermarket signals – a depreciating dollar, a yield curve steepening following a historic inversion, and gold prices surging to new peaks – hints at a potential paradigm shift in global markets. These combined movements suggest a possible entry into a new era marked by heightened risk aversion, a change in macroeconomic drivers, and a re-evaluation of traditional safe-haven assets.

Nevertheless, the decisive catalyst for the next major market move likely resides within the political sphere, contingent on the future trajectory of U.S. fiscal, monetary, and trade policy, particularly the possibility of implementing new tariffs.

Originally published on Substack.