As tariff revenues hit record highs, U.S. economic growth, labor markets, and institutional trust show worrying signs of erosion.

With fresh U.S tariffs imposed on numerous global trading partners and trade deals forged on steep new terms, the evidence is mounting: while tariff revenue has surged, the broader economic picture is deteriorating at home. The latest economic data, visualized through charts from Bloomberg and Statista, tells a sobering tale of a country that may be winning the trade battle, but at a significant economic cost.

Trade Deals: More ‘America First’

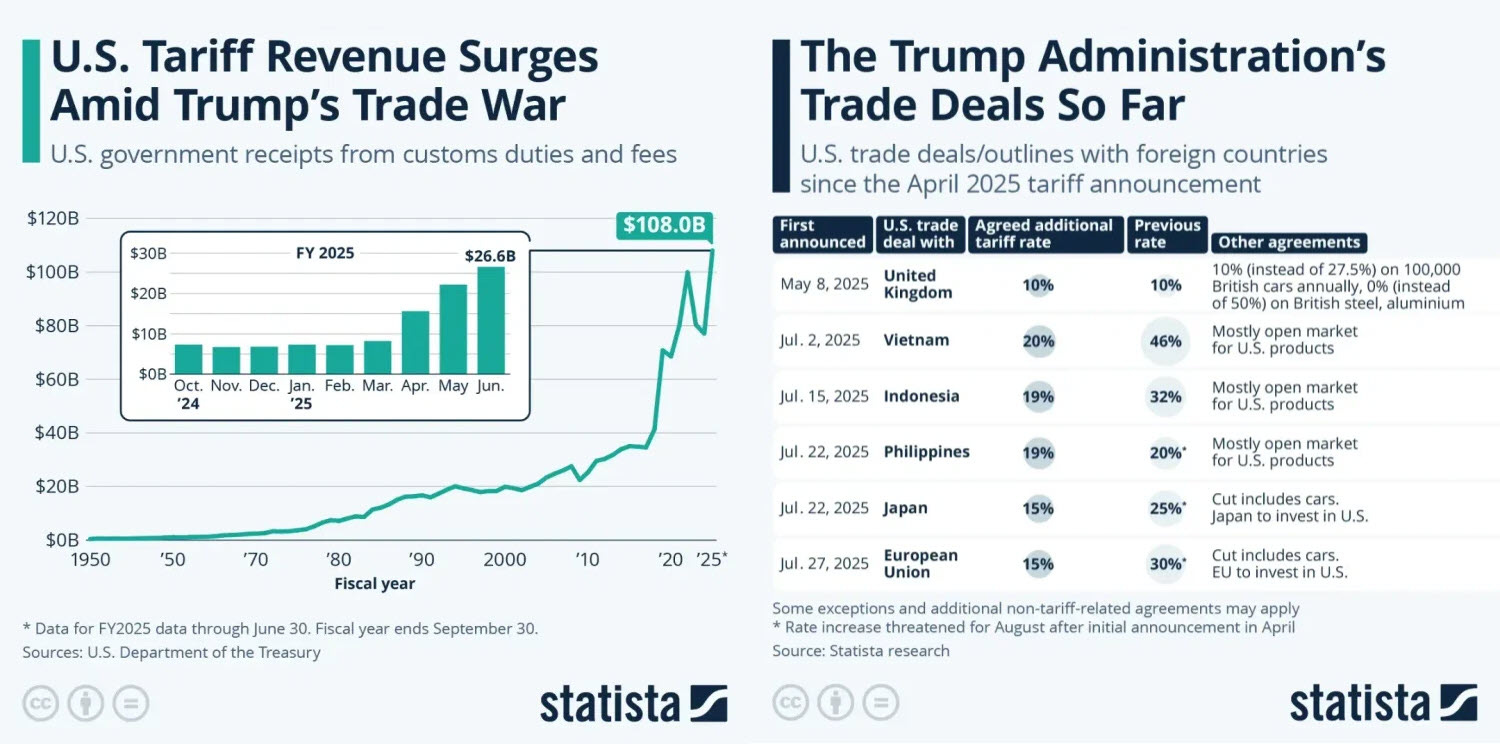

Since April 2025, the U.S. has announced a flurry of trade deals with key partners, including the United Kingdom, Vietnam, Indonesia, the Philippines, Japan, and the European Union. But these agreements come with a twist: the new “understandings” require foreign nations to accept significant additional tariff rates:

-

United Kingdom: 10% added tariffs, with a 10% levy on $27.5B of British cars.

-

Vietnam: 16%

-

Indonesia: 19%

-

Philippines: 19%

-

Japan: 15%

-

European Union: 15%

These are steep rates by any historical measure and represent a major departure from traditional free trade principles. While they do offer better market access for U.S. products, they also risk enflaming diplomatic tensions and could trigger retaliatory trade barriers.

Notably, some deals include clauses that allow foreign investment in U.S. sectors or promise access to U.S. markets. However, the broad perception is that these are heavily skewed in favor of U.S. demands, reinforcing the transactional nature of Trump’s foreign policy.

Tariffs Bring a Cash Windfall

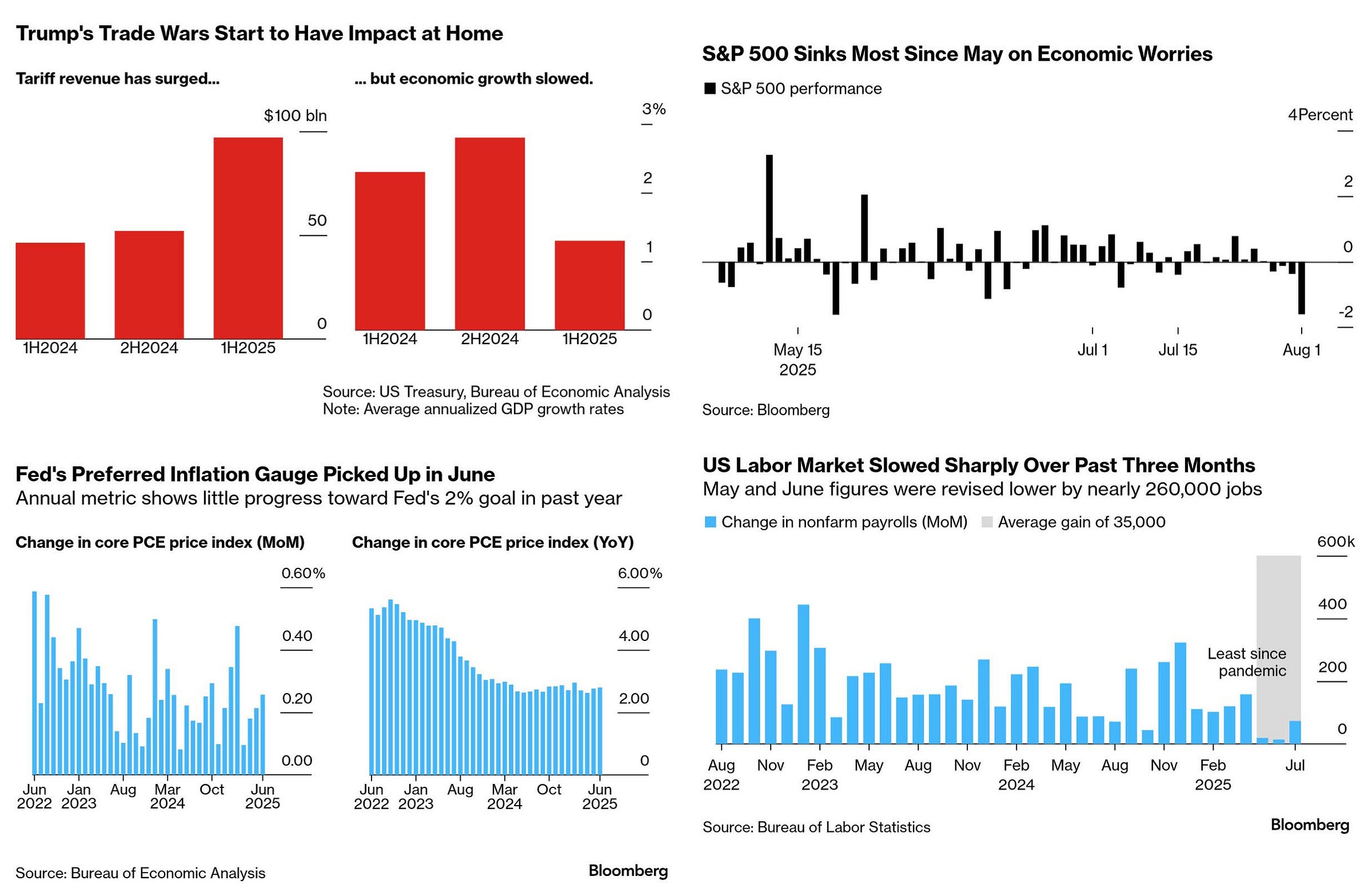

Let’s start with the apparent victory. According to the U.S. Department of the Treasury, tariff revenues have skyrocketed to $108.0 billion in the current fiscal year, with $26.6 billion collected between April and June 2025 alone (chart below). This is a striking increase from prior years and a direct consequence of the renewed tariff push that began after the August 1 deadline ended Trump’s self-imposed 90-day delay on “reciprocal” tariffs.

From a fiscal standpoint, this revenue influx provides the Treasury with short-term breathing room. However, this cash windfall is not without significant caveats. The burden of these tariffs is ultimately borne by American businesses and consumers through higher prices, which could fuel inflationary pressures and reduce consumption.

Growth Stalls Even as Revenue Rises

The economic data, however, suggests a clear divergence: A more concerning aspect of the current trade war strategy is the inverse relationship between tariff revenue and economic growth. While customs receipts have soared, GDP growth has decelerated significantly. The data reveals a troubling pattern: as tariff revenue surged from the first half of 2024 through the first half of 2025, economic growth rates simultaneously declined from approximately 2% to nearly 1%.

This growth slowdown reflects the broader economic reality that tariffs, while generating government revenue, function essentially as taxes on American consumers and businesses. When companies face higher costs for imported materials and goods, they typically pass these costs along to consumers through higher prices, effectively reducing purchasing power and dampening economic activity.

Market Reaction to Economic Anxiety

The financial markets, traditionally seen as forward-looking indicators, are also flashing warning signs. Wall Street endured its most turbulent week (ending Aug. 1) since late May, as a confluence of disappointing economic data, escalating trade tensions, and questions about federal independence jolted investor sentiment.

The benchmark index S&P 500 suffered its worst losses since May, largely in response to economic concerns triggered by slowing growth and labor market weakness. The steepest decline in months illustrates that investor sentiment is turning wary amid fears of a deeper economic slowdown.

Labor Market Deterioration

Nowhere are the consequences of the tariff policy more visible—and troubling—than in the labor market. According to the latest data from the Bureau of Labor Statistics:

-

Nonfarm payrolls rose by only 73,000 in July, a number that missed virtually all expectations.

-

Revisions to May and June subtracted a combined 258,000 jobs from previous estimates.

-

The average three-month payroll gain has fallen to just 35,000, the lowest since the pandemic era.

-

Unemployment rose to 4.2%, up from 3.7% earlier this year.

These employment trends suggest that the broader economic impact of trade wars is beginning to manifest in the labor market. As businesses face uncertainty about future trade policies and higher input costs, many are becoming more cautious about hiring and expansion plans. The service sector, which had been a consistent source of job growth, is showing signs of slowing as consumer spending becomes more constrained by higher prices on imported goods.

Trump’s reaction was characteristically aggressive: he reportedly ordered the dismissal of Erika McEntarfer, the BLS commissioner, accusing her of undermining his economic narrative by faking the job numbers. This unprecedented move calls into question the independence of key government agencies and stokes broader concerns about political interference in official data reporting.

Fed Under Fire, Inflation Still Sticky

One of the most direct consequences of the tariff strategy has been upward pressure on prices across a wide range of consumer goods. The Federal Reserve's preferred inflation measure, the core Personal Consumption Expenditures (PCE) price index (bottom chart above), has shown concerning trends that appear linked to tariff implementation.

-

The month-over-month change was 0.20%.

-

The year-over-year change hovered near 3.5%, well above the Fed’s 2% target.

The stickiness of core inflation limits the Fed’s ability to ease monetary policy, despite growing signs of economic weakness. Trump’s persistent verbal attacks on Fed Chair Jerome Powell—calling for lower rates and blaming the Fed for not doing enough to stimulate the economy—have only added to institutional anxiety.

A Dangerous Precedent: The Politicization of Data

Perhaps the most alarming development isn’t economic, but institutional. Trump’s directive to fire the head of the BLS, combined with his ongoing pressure on the Fed, has intensified concerns over the independence of U.S. economic institutions. The Supreme Court’s recent rulings in Trump’s favor have added to fears that the executive branch is increasingly unchecked.

The broader pattern of attempting to influence or control independent agencies raises fundamental questions about the separation of monetary policy from political interference. Markets and international partners rely on the credibility of these institutions, and any perception that they are subject to political manipulation could have far-reaching consequences for confidence in the U.S. economy.

The Double-Edged Sword of Tariff Economics

The current U.S. tariff regime, reinvigorated under Trump’s leadership in 2025, has undeniably delivered short-term gains in terms of tariff revenue and trade leverage. However, the broader economic fallout paints a far more complex picture.

-

GDP growth is slowing.

-

Inflation remains sticky.

-

The labor market is weakening.

-

Market confidence is wavering.

-

Institutional trust is eroding.

In sum, while tariffs may be an effective negotiation tool or revenue generator in the short run, they are far from a panacea. The mounting evidence suggests that they may be exacerbating the very economic challenges they are supposed to solve.

The challenge for American policymakers is finding a balance between legitimate concerns about unfair trade practices and the economic benefits that international trade provides to American consumers and businesses. The current approach, while generating substantial government revenue, appears to be creating broader economic costs that may ultimately outweigh its benefits.

Originally Published on Substack.