The financial ecosystem across Southeast Asia is currently navigating an intense shift in capital allocation, deeply dividing global market sentiments. A dominant market narrative, widely discussed as Sell Indonesia, has taken center stage across international trading floors and macroeconomic forums. This wave of sentiment has sparked a massive capital migration out of Jakarta, with global fund managers reallocating their liquid assets into Singapore effectively triggering a textbook Sell Indonesia, Buy Singapore rotation. For macro strategists and Web3 investors, dissecting the core fundamental drivers and technical price structures behind this migration is vital for navigating regional portfolios.

Beyond the immediate volatility in equity markets, major cross border infrastructure initiatives are encountering strategic pauses. The multi gigawatt blueprint aimed at exporting 3.4 Gigawatts of clean renewable energy from Indonesia to Singapore has officially been put on hold. State authorities confirmed that establishing the necessary subsea transmission grids requires an extended timeline of roughly 12 to 18 months. On a positive note, bilateral negotiations secured a reciprocal framework guaranteeing Singapore's direct commitment to co developing Sustainable Industrial Zones across the Batam, Bintan, and Karimun regions.

On the trading floor, the aggressive liquidation of Indonesian equities stems from a mixture of macroeconomic headwinds, international rating downgrades speculation, and a tightening grip on sovereign commodity pipelines. Asset managers remain highly defensive regarding fiscal trajectories and structural market interventions implemented by the administration. This highly centralized regulatory approach is perceived by global markets as a fiscal risk that could potentially widen the national budget deficit.

Compounding this market anxiety are widespread rumors pointing toward a potential sovereign index downgrade by tier-one international rating firms, alongside an outlook revision to negative. This combined weight triggered a aggressive sell off of the Rupiah currency, forcing Bank Indonesia into an emergency 25 basis point interest rate hike to 5.5% to defend the foreign exchange market from destabilizing further.

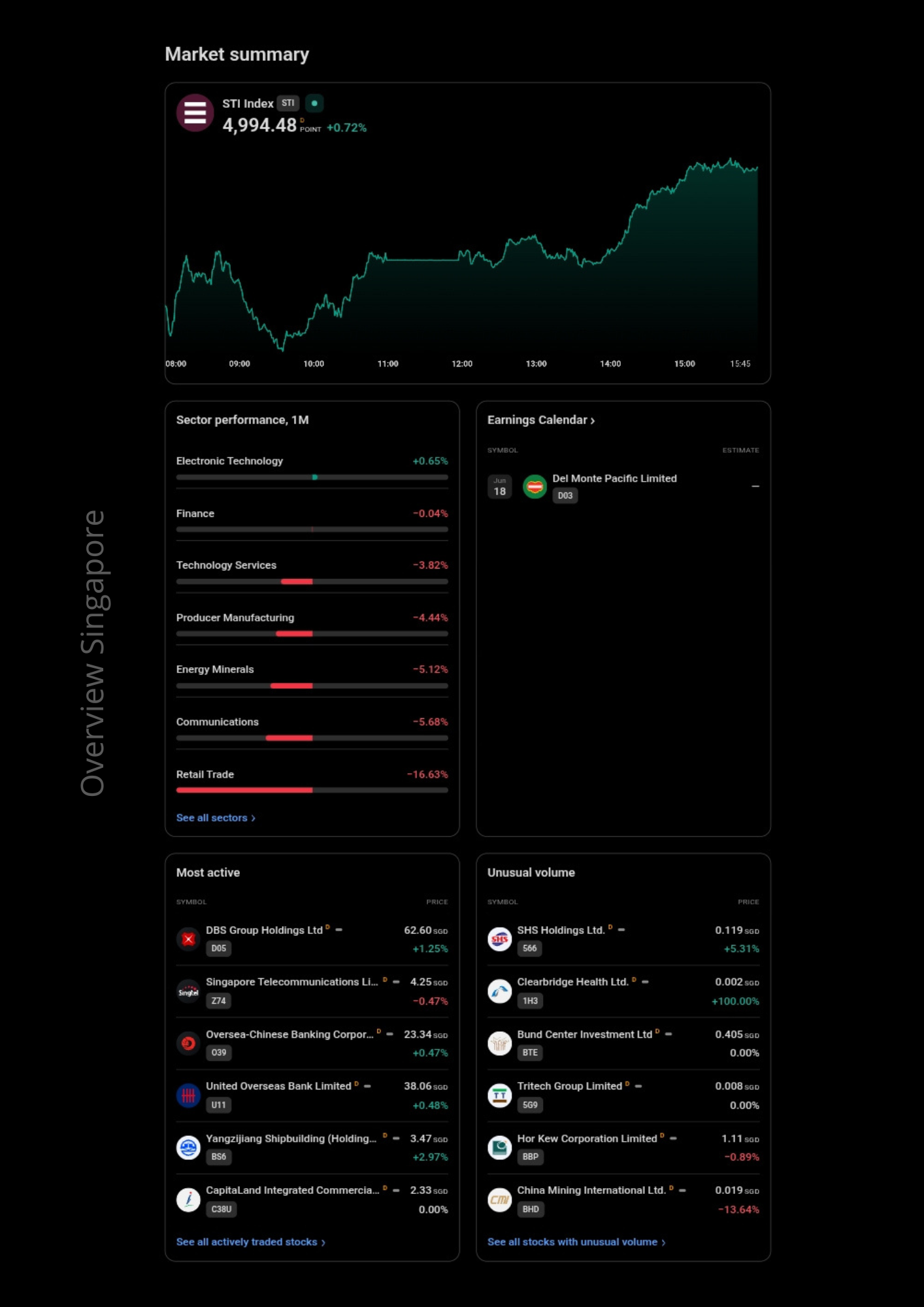

In stark contrast, Singapore has naturally re established itself as the primary institutional safe haven across the Southeast Asian corridor. As capital drains away from Jakarta, the Singaporean equity market has captured that exact momentum. Consequently, Singapore’s total market capitalization has once again climbed above Indonesia's to claim the top spot in the region, heavily anchored by its predictable political environment and ironclad financial infrastructure.

From a pure technical analysis viewpoint, both the underlying sector performance data and live price charts visually map this aggressive regional capital migration with absolute precision.

Indonesian Equity Market

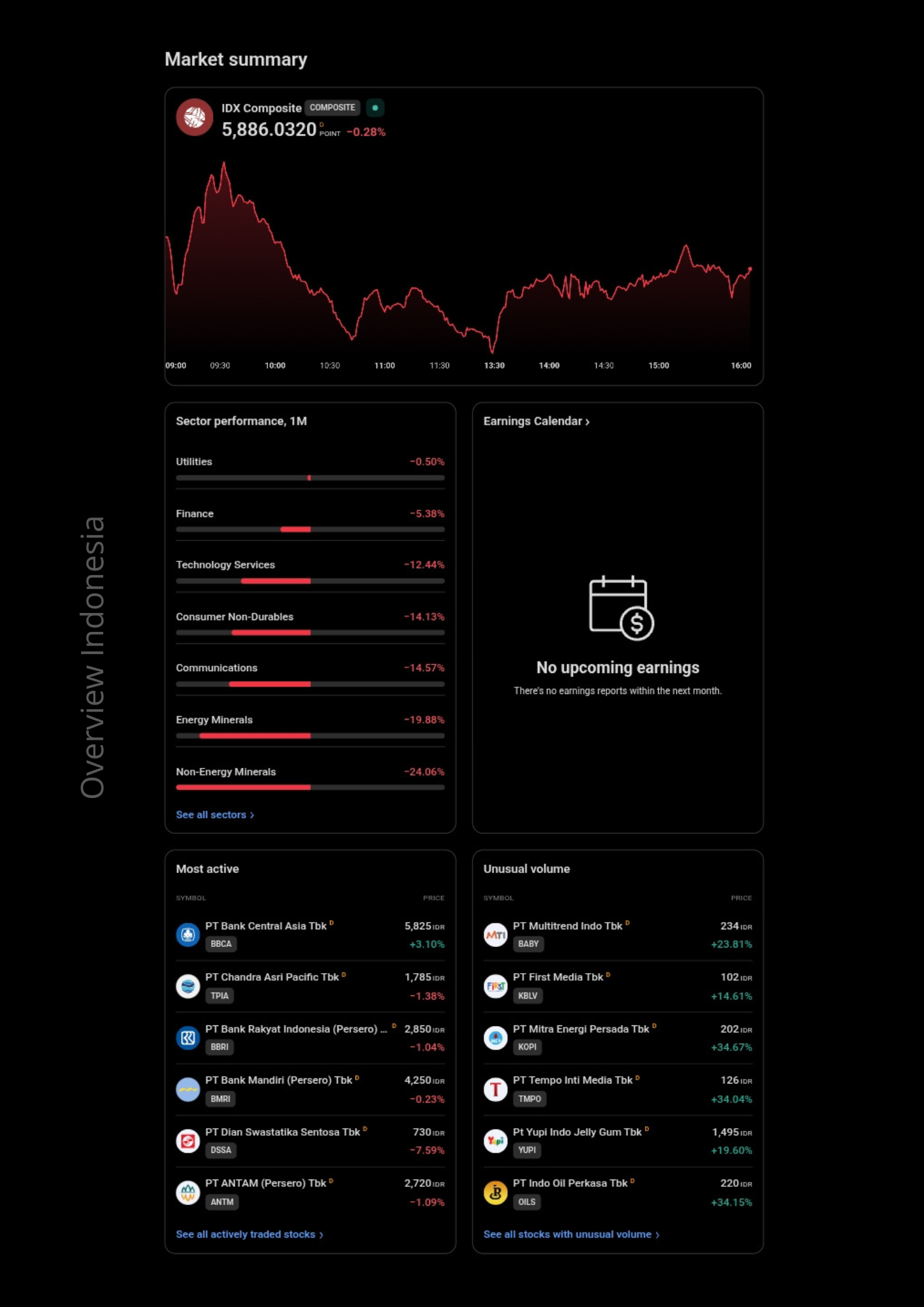

According to macro market feeds as of June 2026, the JCI is hovering around the 5,886.03 mark, booking a daily loss of 0.28%. The most severe damage over the last 30 days is concentrated within the non energy mineral sector, which crashed by minus 24.06%, followed closely by energy minerals at minus 19.88%, and telecommunications at minus 14.57%. Fast moving consumer goods and tech sectors have similarly sustained deep structural damage. This restricted systemic liquidity, exacerbated by the central bank's defensive rate hike to 5.5%, leaves local equities facing a steep uphill battle.

From a structural standpoint, the Jakarta Composite Index has locked into a definitive bearish cycle on macro timeframes. The daily chart reveals that this intense distribution phase ultimately broke the long term bullish market structure downward after price action failed to hold a vital daily support shelf. Dropping down to the one hour chart, the index attempted to build a temporary accumulation base, but persistent overhead supply continuously forced prices into fresh local lows. Traders should stay patient and watch for clear signs of seller exhaustion or historical weekly demand zones before anticipating any meaningful or sustainable bullish structural shift.

Singapore Equity Market

Conversely, while Jakarta battles persistent capital outflows, Singapore’s STI index remains exceptionally resilient, trading firmly at the 4,994.48 level with a solid daily gain of 0.72%. The Singaporean sector wrap shows broad-based strength, spearheaded by electronic technology gaining plus 0.65%, while defensive sectors are primarily trading flat or down by mere fractions. This represents a flawless, real time sector rotation institutional capital exceeding $2,000,000,000 (or written as >$2B) exiting blue chip Indonesian names is finding an immediate home across Singapore's liquid asset classes.

The Singapore Straits Times Index chart displays a defensive and highly bullish market structure. On the daily timeframe, the long term uptrend has been maintained with great consistency since the beginning of 2026. More interestingly, on the one hour timeframe, the STI price action has formed a clean falling wedge chart pattern and successfully breakout upward. This pattern confirms a short term upside continuation toward the gray resistance area above the 5,020 level. This technical trend remains in a strong bullish condition as long as the higher timeframe support level holds.

My Opinion

The Sell Indonesia and Buy Singapore narrative currently presents a highly polarized situation that requires an objective view. Critically, the massive capital flight and sharp drop from all-time highs expose a severe vulnerability in domestic market liquidity when facing regulatory uncertainty. Relying on sudden interest rate hikes to save the currency feels like a short term sedative that accidentally punishes the growth of domestic equities.

The government's bold move to implement a single gate export policy for strategic commodities through PT Danantara Sumberdaya Indonesia (DSI) as of June 1, 2026, has also sparked mixed reactions. This centralized policy for palm oil, coal, and ferroalloys is designed to eliminate price manipulation practices and stop the flight of export revenues. While this policy creates short term uncertainty for foreign investors, it is a crucial step to strengthen national economic sovereignty in the long run.

The impact of this single gate policy was also directly felt regionally, particularly in Singapore, which is one of Indonesia's main trading partners. This tightening policy even briefly dragged down the shares of palm oil companies listed on the Singapore exchange due to fears of upstream supply disruptions. The Deputy Prime Minister of Singapore himself responded directly, stating that they respect Indonesia's strategic export priorities and are committed to maintaining dialogue with the business community to strengthen supply chain resilience between the two nations so that trade flows smoothly. Once a technical bottom forms on the JCI and the transition of this export regulation is fully understood by the global market, the underlying economic fundamentals could trigger a very powerful reversal for domestic assets.

Click here to read my authentic and original analysis

Source

- Crypto Wave

- The Straits Times

- Respons Singapura Soal Kebijakan Ekspor Satu Pintu RI Lewat PT DSI

- Rupiah slide and ‘Sell Indonesia’ stocks: Jakarta’s counter moves useful but experts flag deeper fiscal concerns

⛔ Disclaimer: This article is strictly for informational and educational purposes only. It is not intended as financial advice, and I do not provide any trading signals. All investment decisions are your sole responsibility. Please ensure you conduct your own research (DYOR) before making any trades.