As if we needed another reason to decentralize finance from the central banks, four IMF policy writers Arnoud Boot, Peter Hoffmann, Luc Laeven, and Lev Ratnovski are creating a new paper which will outline plans to place tighter constraints on those seeking credit by incorporating not just their payment history but their non-financial data such as searches.

The use of non-financial data will have large effects on the provision of financial services. Traditionally, banks rely on the analysis of customer financial information from payment flows and accounting records. The rise of the internet permits the use of new types of nonfinancial customer data, such as browsing histories and online shopping behavior of individuals, or customer ratings for online vendors. The literature suggests that such non-financial data are valuable for financial decision making. Berg et al. (2019) show that easy-to-collect information such as the so-called “digital footprint” (email provider, mobile carrier, operating system, etc.) performs as well as traditional credit scores in assessing borrower risk. Moreover, there are complementarities between financial and non-financial data: combining credit scores and digital footprint further improves loan default predictions. Accordingly, the incorporation of non-financial data can lead to significant efficiency gains in financial intermediation. Large technology firms collect vast amounts of non-financial data through their consumerfacing platforms in the areas of e-commerce, social networking, and online search. The sheer

amount of data enables the use of “big data” analysis tools such as artificial intelligence and machine learning. The literature confirms their usefulness in finance.

SCARY STUFF!

Thankfully us peons and proles no longer have to be at the mercy of central banks anymore as we have options in cryptocurrency that neither require a FICO score or highly invasive personal data beyond standard KYC. The LTV and interest rates vary and I feel as time goes on competition will increase in the space.

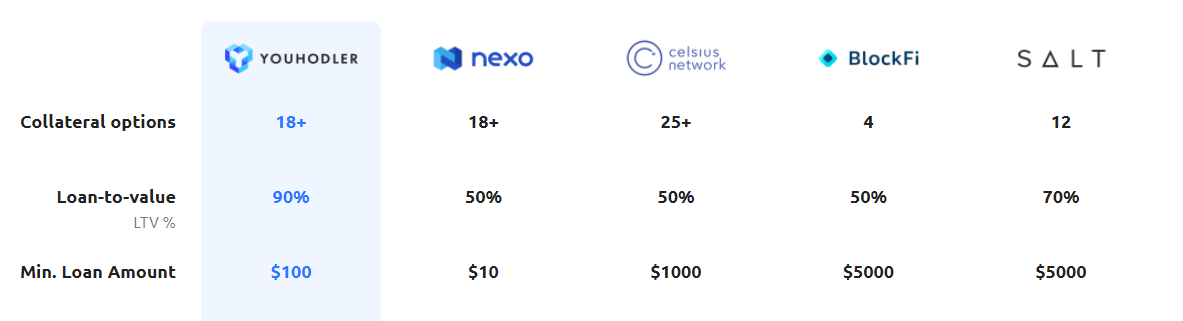

1.) YouHolder (Not Available in: Afghanistan, Bangladesh, China, Cuba, Germany, Iran, Iraq, North Korea, Pakistan, Sudan, South Sudan, Switzerland, Syria, United States of America, US Minor Outlying Islands, US Virgin Islands, Republic of Crimea)

2.) Celsius Network

3.) SALT Lending (United States Only)

4.) BlockFi Borrow

5.) Nexo

It's only a matter of time until we have crypto collateral for mortgages in my opinion. Now there is a token idea I'd ape into. If it means more competition for these IMF ghouls looking to trace and database your queries in Google for credit-worthiness then I am all for it.