Digitization is reshaping society: The way we work, relate, exchange information and now also how we carry out financial transactions have been changing rapidly, leading us to adapt and change paradigms.

In the last decade, the financial services sector has been affected by a number of new technologies and the creation of Bitcoin has been present strongly influencing this process. A popularization of decentralized digital currencies and the demand for faster and cheaper means of payment are what makes crypto, stable coins and solutions for the resolution by FinTech’s have a very big adoption potential.

At the same time, the interest of Big Techs in the financial sector, such as Amazon, Alibaba, Google and Facebook, with their giant platforms where it would be possible to integrate their own digital currencies into their convenient database, led central banks to act and join the game. before evolution passes them by, leaving them behind.

The Libra Project was a wake-up call: a Facebook user base is equivalent to about 40% of the world population and stable coin would have an unprecedented reach, which means a threat to current payment systems, so much so that efforts by some regulators in an attempt to stop the project.

With the initial objective of positioning itself in this digital revolution, they emerged as initiatives by central banks to create their Central Bank Digital Currencies (CBDCs), whose term refers to digital versions of their fiat currencies.

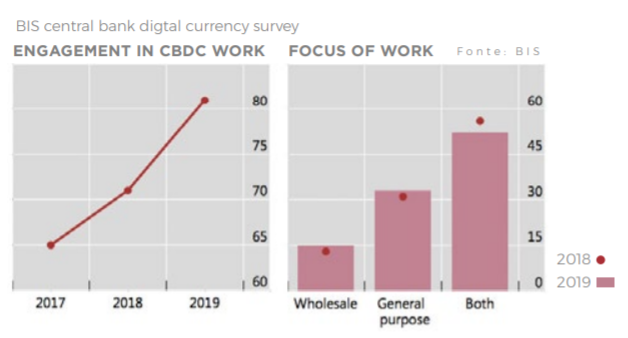

As CBDCs offer a new digital payment, more secure and affordable accessible, but the impacts can be deeper, and can provide considerable changes. According to the BIS (Bank for International Settlements), currently 80% of central banks around the world consider introducing some form of CBDC in their markets in the coming years, among them, the countries that are testing a CBDC, are Japan, Sweden, France, Switzerland, Philippines, Uruguay, Russia and Saudi Arabia.

Much of the effort was catalysed by the Covid-19 pandemic, due to the unhygienic handling of banknotes.

China was the first country to announce an intention to develop a CBDC. In Brazil, following the trend of digitization by the PIX, there is already the formation of a study group to discuss the impacts of a digital currency and it is even commented on in a “Real Digital” ready in 2022.

It is important to note that a CBDC will not be an original cryptocurrency in itself, nor will it necessarily use blockchain and will represent an approach totally contrary to decentralization, as trading with a CBDC does not imply anonymity nor much less privacy.

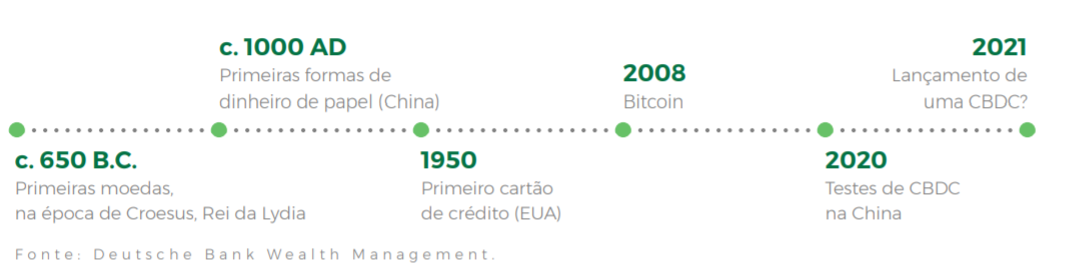

TIME LINE WITH THE HISTORY OF CURRENCY IN THE WORLD

To take a closer look at a CBDC, let's take the example of the one that is most advanced in terms of development, the digital yuan. Although there is still no date launch, the People's Bank of China is likely to be the first major central bank to issue a digital version of its currency, seeking to keep pace with a rapidly growing economy digitization and the intention to become a world leader in science and innovation by 2050.

It is expected to be a digital ledger that will replace local currency variants and will compete against the US dollar and different cryptocurrencies. Tests are already being carried out in the cities of Shenzhen, Suzhou, Chengdu and Xiongan, through local companies and more tests are planned for the 2022 Winter Olympics.

The digital yuan, when launched, will represent an aggressive consolidation of economic power, as it will subject more than 1.3 billion of people to the even greater surveillance of a government that will have much easier access to all transactions carried out by the population. All of this facilitated by the great adherence to digital payments, which already represent the majority of transactions there compared to those made in cash.

It is important to note that the Chinese authorities made the decision to become pioneers in CBDCs after they emerged concerns after the possibility of launching the Facebook Libra, which triggered the countries' alert for maintaining the sovereignty as more privately organized initiatives may emerge.

With the successful launch, China could stop using the SWIFT system (Society for Worldwide Interbank Financial Telecommunications), making the country more independent from international exchange systems.

The launch of the digital yuan would be a relevant event, considering China's population and economic size.

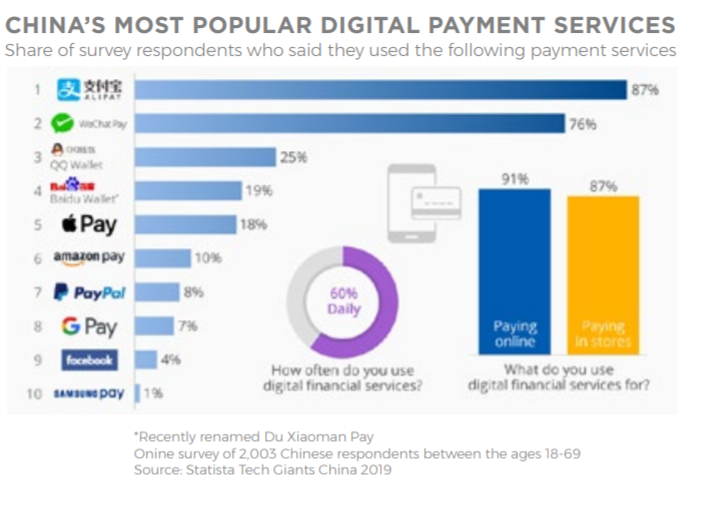

Most of the transactions carried out by the Chinese are made through channels and digital tools.

These are the main payment services used by the Chinese.

Alipay and WeChat are preferred by consumers.

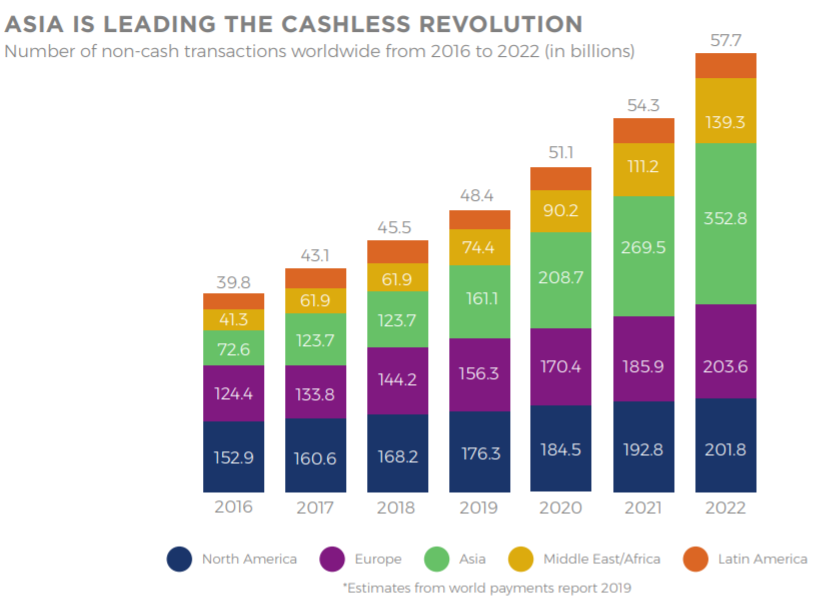

Asians are the most familiar with digital means of payment. In a Visa survey, it was found that about 64% of consumers in Southeast Asia are confident that they do not need to use paper money.

The World Payments Report shows that the value of non-monetary transactions in Asia is expected to grow to $352.8 billion in 2022.

The motivations for research on CBDCs are diverse and there are advantages and disadvantages in their implementation, both for individuals and for the BCs themselves.

ADVANTAGES FOR INDIVIDUALS:

- They are basically related to speed, ease and security in monetary transactions, providing access to a system with operation and availability 24 hours a day, 7 days a week.

- Some existing risks of poor corporate governance can be reduced by better transparency and traceability of transactions.

- CBDCs would help in some way to improve financial inclusion by being available to anyone who has a smartphone, especially residents of rural areas without access to physical banking infrastructure, such as ATMs.

ADVANTAGES FOR CENTRAL BANKS:

- It represents better traceability of transactions in real time, being able to assist them in combating money laundering, in addition to agility and efficiency in commercial transactions and risk reduction.

- Monetary policy can flow more quickly and continuously. It would help with the transfer of “helicopter money” to individuals as it would be a mechanism for sending funds directly to people.

CBDC can give governments visibility on individual transactions, improving traceability and user identification, theoretically helping to combat money laundering and tax evasion.

RISKS FOR INDIVIDUALS:

- The main threat is related to privacy, since the inspection bodies would have much easier access to the financial information of the population, which can lead a government to exceed the limits of privacy rights. Thus, people would be much more vulnerable to censorship and control

RISKS FOR CENTRAL BANKS:

- One of the main fears of central bankers is that a digital currency, by its very nature, can be quickly withdrawn from banks and exchanged for CBDC, which could facilitate a rush effect not only for a bank, but for the entire banking system of the parents. This would cause a financial shock with the danger of making institutions insolvent.

- Many central bankers believe that issuing a CBDC can have a negative effect on the way people view banks, leading them to legitimize and see the true value of decentralized cryptocurrencies, such as Bitcoin, assets that are just intended to replace the current system.

- In addition, the issue of cybersecurity and the infrastructure needed to mitigate the risks of attacks must also be taken into account, as it will be a centralized system and the target of attacks.

SOME IMPORTANT MOVEMENTS BY THE GOVERNMENTS IN RELATION TO THE ADOPTION OF A CBDC:

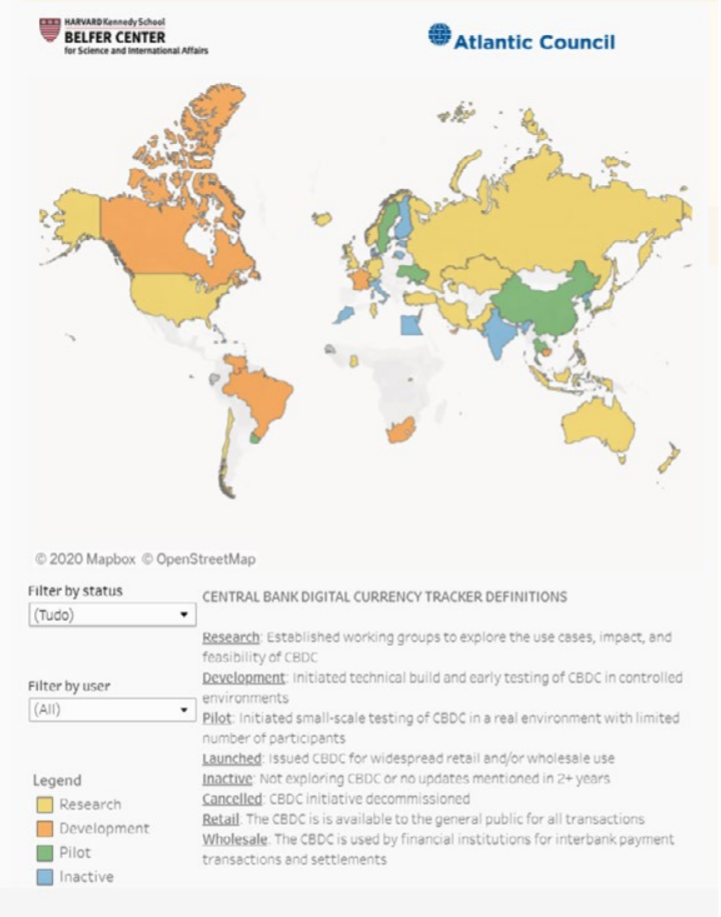

The atlantic council website has updated data from countries regarding the development of their CBDCs.

China, Sweden and Ukraine are the only ones so far to have pilot projects for CBDCs. Brazil, Canada, South Africa and France have a project under development.

USA, Russia, Australia, New Zealand, United Kingdom, Turkey, Iran, Chile and the Philippines are under research. India, Egypt, Morocco, Denmark and Italy have ongoing initiatives related to their own currency.

Data from the BIS (Bank for International Settlements) shows that in 2020, global searches on the Internet for CBDCs outperformed even searches for Facebook's Bitcoin (BTC) and Libra.

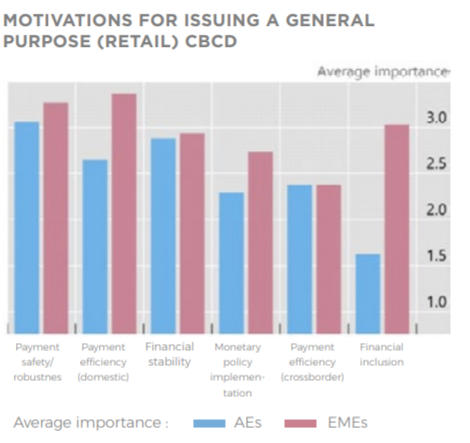

Security, efficiency in payments and financial inclusion are the main motivators for the implementation of a CBDC, according to BIS data. In addition, it is also possible to see that emerging countries show more urgency for these changes.

Data from the BIS (Bank for International Settlements) shows that in 2020, global searches on the Internet for CBDCs outperformed even searches for Facebook's Bitcoin (BTC) and Libra.

Security, efficiency in payments and financial inclusion are the main motivators for the implementation of a CBDC, according to BIS data. In addition, it is also possible to see that emerging countries show more urgency for these changes.

Despite the opposing opinions, many believe that CBDCs could contribute to the adoption of cryptocurrencies on a larger scale. However, the increase in control by issuers is a matter of concern. A CBDC is just the digital version of a fiat currency, which gives it some improvements in terms of user experience, however, being under the command of a central body, it will be much more easily under surveillance. It is convenience at the expense of privacy.

Great uncertainties remain regarding interoperability, infrastructure and what power imbalances this could result. Furthermore, what if some countries migrate to a CBDC and others do not? These implications will go far beyond making transactions easier and improving the effectiveness of monetary policy.

It is a development that needs to be closely monitored, as a CBDC may soon become part of our lives.