1. Martingale type’s betting systems

Martingale betting systems are considered the oldest optimal betting systems, which guaranty a positive profit to a player if the player has infinite starting capital (bankroll). In these systems a size of bets is adjusted in such way that new winnings compensate for the previous loses (see [1-2]).

Let us consider a simple martingale system that uses the same size of a minimal bet, if the previous outcome was a win, and in the case of a loss the new size of the bet is doubled. As we can see, after a series of loses the first winning bet covers all previous loses and gives a positive profit to this player. In theory (infinite starting capital) this strategy works fine, but in the real life an amount of a starting capital is always limited. If accumulated loses will be larger than the available capital then the player will not be able to place the next bet. This situation is called a ruin problem.

Such type of strategies are known from ancient times. In 18-th century French mathematicians adjusted them to card games and roulette in French casinos. Such betting systems become popular when some people won millions by using them. Casino owners hired mathematicians to determine if it is good or bad for casinos if people will be using such systems. The mathematicians come to the conclusion that usage of such systems will be profitable to casinos, because losses from those who gets into the ruin problem will exceed winnings from those who will be lucky and win.

A casino owner by name Martindale popularized this strategy among his casino’s clients. The story tells us that the word “martingale” was derived from this person name. In our days, some traders, investors and gamblers still use this strategy.

If a trader has $10,000 starting capital and places 100 trades (with the first trade of $100) according to the martingale system, where she/he wins a trade with a probability 0.51 (51%) and loses the trade with a probability 0.49 (49%), then the probability of ruin during these 100 trades is over 0.34 (34%).

The martingale type’s strategies have the following drawbacks:

-they do not take into account probabilities to win/lose;

-they have a very high probability of ruin.

2. Optimal strategies based on Kelly’s criterion

In 1956, a mathematician John Kelly, Jr. published an article in which the optimal solution was found for games with positive expected value (edge). Kelly avoided the ruin problem by allowing bets to be infinitely divisible (see [3-6]). This resulted in a nice and beautiful optimal solution of a mathematical problem.

If a player can win $1 with a probability p and lose $1 with a probability q, where p>q, then Kelly’s strategy is to bet p-q fraction of the current capital (bankroll). If p-q<=0 then players should not play the game. In theory (infinite time to play) this strategy gives the fastest speed of growth in capital for players.

A mathematician, Edward Thorp, was the first person who successfully applied Kelly’s strategy to blackjack card games in casinos and trading in financial markets. His fund Princeton Newport had never had a down quarter and his fund Convertible Hedge Associates, from November 1969 trough December 1973 had cumulative gains of 102.9 percent, versus a loss of -0.5 percent for the Dow Jones average in the same period (see [7]).

In practical situations with a finite number of bets and limits on minimal and maximal bets, Kelly’s strategy is not the optimal strategy for many players/investors with different risk-reward preferences (see the example below).

3. Minimax optimal strategies

Minimax type of strategies also known from ancient times. They were used by military leaders to find optimal strategies in wars with an adversary, which maximize success from own actions and minimize losses from the adversary actions. After the World War II, some information on this topic was declassified and published.

In 1997, the world chess champion Garry Kasparov lost games to Dip Blue computer. Dip Blue used minimax strategy to win the games (see [9]). Since then minimax type of strategies are popular among game theorists and artificial intelligence systems developers. Strange enough, that majority of financial advisers do not know this type of strategy and do not advise their clients to use it.

In simple words, we define a minimax type of strategy as a strategy that minimize some criteria (for example, loss, probability of ruin, etc.) and maximize other criteria (for example, profit, gain, capital growth, etc.) on the given set of restrictions (for example, maximal and minimal limits on bets/investments, total number of bets/trades, etc.)

Let us consider three persons with different risk-reward preferences. Alisa is a day trader on crypto and stock exchanges. She buys in the morning derivatives with the best profit potential and sells at the end of the same day. On average, she has 51% of correctly determined directions of price movements and 10% profit/loss per trade. She is a risk averse person and wants her probability to have positive gains after 365 days of trading to be over 60% and risk of ruin less than 10^-6. Alisa also wants that the strategy to be robust to 1% error in an estimation of the probability to win.

Sue trades crypto and currency derivatives with performance similar to Alisa’s performance. Sue is a risk taker and wants her probability to have loses after 365 days of trading to be less than 48% and risk of ruin less than 10^-5.

Peter is gambling on penny stocks and hopes to hit a big jackpot. He is able to tolerate that a probability of ruin after 365 days not exceeds 0.0001, if an average profit is not less than 25%. Assuming that the minimal investment is 1% of the initial capital, what fractions of capital (as bets/trades) will be optimal to Alisa, Peter and Sue?

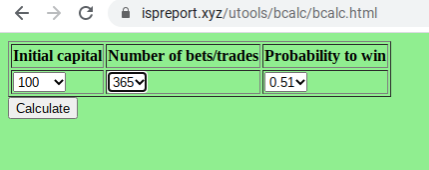

Firstly, we go to the URL: https://www.ispreport.xyz/utools/bcalc/bcalc.html and select input parameters as 100 for initial capital in minimal bets (IC), 0.51 for probability to win (p), and 365 for number of bets/trades (nb). These are input parameters for all traders.

Secondly, we click on the “Calculate” button to get results. In the first column of the result’s table are sizes of bets/trades as fractions of the available capital (%). In the second column are average amounts of capital after 365 bets/trades (AvrC). In the third column are probabilities (PrW) that after 365 bets/trades it will be a positive gain (increase in the initial capital). In the fourth column are average values of the capital in cases of a profit (AvrCW). In the fifth column are probabilities that at the end it will be a loss (PrL). In the sixth column are average values of the capital in cases of a loss (AvrCL). In the seventh column are estimations of a probability of ruin (PrR). These estimations do not take into account trading fees.

Kelly’s criterion (p-q=51%-49%=2%) gives the optimal bet size of 2% from the current capital as the optimal strategy. As we can see from the results, the Kelly’s strategy does not satisfy requirements of any trader. For Peter, the optimal strategy is to bet 4% of the current capital, for Sue, the optimal strategy is to bet 3% of the current capital. To find a robust strategy for Alisa we need to calculate results for p=0.5 and compare them with the results for p=0.51.

We again enter new input data and click on the “Calculate” button. The results are shown in the table below.

As we can see from the results, in a case of 1% error in estimating the probability to win, an average loss of the initial capital is less than 0.01%. This means that the strategy with 1% bets is the optimal robust strategy for Alisa.

Now, let us compare the minimax strategy with the popular SMA & RSI strategy (see, for example

https://www.publish0x.com/dutchcryptodad/sma-and-rsi-trading-strategy-is-it-profitable-or-not-xknqkjq ). The SMA & RSI strategy has the same 51% probability to win, but it has the probability of ruin 0.96 (96%), which is more than on four order of magnitude bigger than minimax strategies of Sue, Alisa and Peter.

As we can see from the above, minimax optimal strategies give the best performance with regards to risk-reward profiles, the probability of ruin, and limitations in the real life situations. But there are no free gains without risks involved. Those who can not tolerate risks, should use strategies with zero market risk, for example friendly arbitrage, which has zero market risk and infinite return on investment (see [12]), and guaranties positive gains regardless of an outcome in the future.

It should be noted that a minimax strategy is not a gambling strategy, it is a trading/investment/betting risk management strategy, which puts at risk only a small fixed fraction of the current capital.

Key differences between traders/investors and gamblers are presented in the table below.

A famous example of what happen when people underestimate a probability of ruin is the case of Long-Term Capital Management (LTCM) hedge fund (see [10-11]).

P.S. 1. The service used is not free, you need to buy a license to use it.

2. Historical results do not guaranty that in the future will be similar results.

3. Always estimate your possible loses to manage your risks.

4. Kelly initial motivation was to find a strategy which maximize growth of capital for investors having the same logarithmic utility function. Later it was discovered (by mathematicians) that Kelly’s strategy also minimize time to reach the goal. Therefore, today we can classify Kelly’s strategy as minimax type of strategy.

In the next post we consider a simple way to make money when values of cryptos go down.

References

[1] Martingale (betting system), From Wikipedia

https://en.wikipedia.org/wiki/Martingale_(betting_system)

[2] Martingale System

https://www.investopedia.com/terms/m/martingalesystem.asp

[3] Practical Implementation of the Kelly Criterion: Optimal Growth Rate, Number of Trades, and Rebalancing Frequency for Equity Portfolios

https://www.frontiersin.org/articles/10.3389/fams.2020.577050/full

[4] Using the Kelly Criterion for Asset Allocation and Money Management

https://www.investopedia.com/articles/trading/04/091504.asp

[5] Kelly criterion, From Wikipedia

https://en.wikipedia.org/wiki/Kelly_criterion

[6] The Kelly Criterion: You Don't Know the Half of It

https://blogs.cfainstitute.org/investor/2018/06/14/the-kelly-criterion-you-dont-know-the-half-of-it/

[7] Fortune’s Formula (The untold story of the scientific betting system that beat the casinos and Wall street), William Poundstone, 2005, Hill and Wang (a division of Farrar, Straus and Giroux)

[8] Mixed Strategy Play and the Minimax Hypothesis

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=10759

[9] Deep Blue -The IBM Chess Computer That Beat Chess Grand Master Garry Kasparov in 1997

https://www.ststworld.com/deep-blue/

[10] Long-Term Capital Management (LTCM)

https://www.investopedia.com/terms/l/longtermcapital.asp

[11] When Genius Failed: Lowenstein Talks LTCM

https://www.thestreet.com/opinion/when-genius-failed-lowenstein-talks-ltcm-11060196

[12] Friendly arbitrage