Commodity trading strategies. Part 1:

https://www.publish0x.com/real-world-assets/commodity-trading-strategies-xxzkjyk

Commodity trading strategies. Part :

https://www.publish0x.com/real-world-assets/commodity-trading-strategies-part-2-xkplkkg

Convergent and divergent risk raking:

One of the most, if not the most popular divergent trading strategies, i.e., momentum. These strategies mean buying assets that performed well in the recent past, and selling ones that performed poorly. It seems that momentum or trend-following should not work; nothing can be simpler than this - just buy winners, and get rid of losers. However, there is extensive research showing that momentum strategies work in different asset classes. Looking at the recent performance (3-12 months) and then going long the winners and going short the losers leads to statistically significant profits almost in all markets.

Erb and Harvey in their classical paper, “The Tactical and Strategic Value of Commodity Futures”, describe a simple diversified trend-following trading strategy - buying all commodities with positive return during the past 12 months and selling all commodities with negative return. Based on the data from 1983 to 2004, the strategy produced a Sharpe ratio of 0.85. Their finding is not unique; other researchers also came to a similar conclusion which is that extrapolating the recent performance (3-12 months) to the near future (with a holding period of 1-3 months) is a profitable strategy.

There are many rules for trend-following strategies. The most popular one is based on moving averages which produces a buy signal when the price is above the moving average; and when the price is under the moving average, it is a signal to sell. Another common rule is a moving average crossover which employs long- and short-term moving averages. If short-term MA is higher than long-term MA, it is a buy signal; the opposite produces a sell signal.

Crude oil is one of the most traded commodities. In the article “Structural Positions in Crude Oil Futures Contracts”, Hilary Till describes a trading strategy involving oil futures. She notes that one can take a long-term position in crude oil futures mainly to diversify a portfolio.

By going long and rolling WTI futures an investor could realize an excess return (return over T-bills) of 6.2 percent from 1987 through 2014. Is it possible to improve this return? The answer to this question is yes. You may remember the discussion on the term structure of futures contracts. When the curve is backwardated it implies that inventories are low which can result in price spike. You also may recall that commodities that historically tended to trade in backwardation exhibited a positive roll yield, while the commodities that traded in contango had a negative roll yield. So we can tweak our very simple strategy of holding crude oil futures slightly: we will hold and roll Brent futures only when the term structure is backwardated. To be more clear, we will buy and roll Brent futures only when front-to-back spread is in backwardation. It turns out that this has a substantial effect on the return difference - the excess return jumps from 6.2 percent to 12.8 percent.

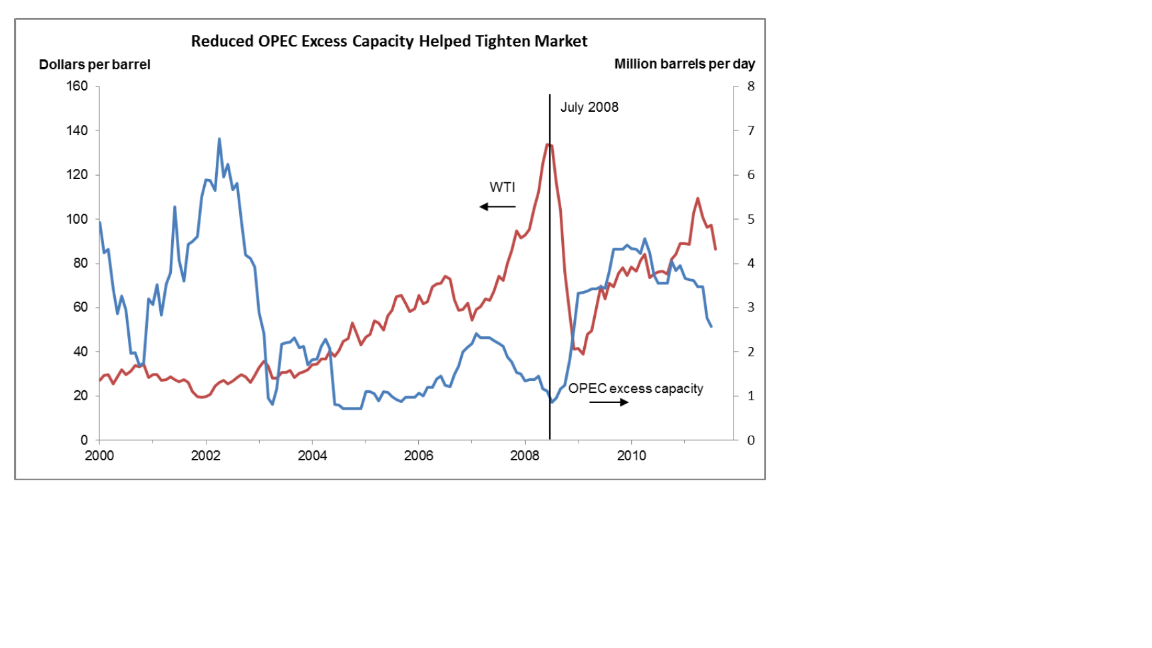

However, we all know that crude oil futures contract is a crash-prone asset. To avoid crash risk, we add the second variable to our strategy, namely OPEC spare capacity. When spare capacity is at historical lows, it can be followed by a collapse in oil price as in 2008.

Our second requirement for taking a structural position in oil futures is that OPEC spare capacity should be more than 1.8 mbd( million barrels per day). Holding and rolling Brent futures unconditionally from 1999 through 2014 had a monthly return of 1.2 percent with a negative skew. However, if one only holds and rolls Brent futures when front-to-back spread is backwardated, and OPEC spare capacity is greater than 1.8 mbd, the monthly return increases to 2.0 percent. And this simple strategy exhibits a positive skew.