Did you know that 1.9 BILLION dollars is given to American children in allowance annually? Sounds ridiculous, right? Well, it’s certainly an issue. Giving children an allowance isn’t a great idea because it creates a restricted view of the financial world in a sense, as well as making children dependent on parents and others for money. But what exactly proves this?

First of all, an allowance teaches kids a way of “making money” that isn’t something realistic in the real world, creating a limited financial view and diminishing the possibility of them going out to find their own ways of making money. It’s like giving them birthday gifts constantly without it actually being their birthday. According to an article from Money Prodigy:

“An allowance is supposed to be consistent, so as long as your child meets the baseline requirements you have for them to receive it, they'll get the money each week/every other week/etc. In some kids, this could develop into an attitude that's not all together grateful. Meaning, they feel entitled to the money.”

This shows how and why the allowance can come across as an entitlement rather than doing work for the money. Kids can very easily take it for granted and the true value of money isn’t taught to them. Children receiving easy money from their parents would spend it all, since they know they’ll always have more.

On the other hand, a child without an allowance will likely manage their money much better, since it’s their hard-earned money rather than their parents, and they need to take care of it properly. Personally, I’ve never gotten an allowance. It taught me how to make money on my own, sent me scouring the internet, and made me work hard to successfully learn about, make, and manage money at an early age. There are a variety of alternatives to an allowance that can achieve the same goals without the potential negative consequences. Once they’re aware of how money can be managed and the value of it, the rest is up to them if they want to buy things or spend money. A Destination Innovation article even says:

“Children have the benefit of not knowing what is not possible. For them everything is feasible. What’s more, young children get praise and encouragement from their parents and teachers for almost any work they do – particularly for imaginative stories or weird pieces of art. They have heard tales of magic and they see around them technology doing all sorts of amazing things. … Adults on the other hand are only too well versed in what they cannot achieve and what cannot be done. They are surrounded by rules, regulations, laws and compliance. … If we want to be truly creative we need to think like children again. We need to imagine an ideal solution and then ask ‘Why not?”

It’s been proven that children are much more creative, with less limits and a plethora of ideas at their disposal. They can even learn new skills better than adults. With that creativity they can use it to work things out on their own, developing other beneficial skills along the way.

Another reason children should not have allowances is because it makes kids much more dependent on their parents and others for money, getting rations of it like slaves. Prominent business magnate, millionaire and author of the award-winning financial book Rich Dad Poor Dad, Robert T. Kiyosaki has said, “Don’t work for money; make it work for you” and “Don’t be addicted to money. Work to learn. Don’t work for money. Work for knowledge.” In other words, he believes in financial independence gained through financial literacy. If a child gets an allowance, they’re relying on their parents to periodically provide them with money. It becomes an expectation that they get paid, and then they don’t manage the money. Are they really learning anything, or is it more of an artificial effect? Unfortunately, the latter may be true in many cases. This is mainly because it’s not technically theirs, but willfully given to the child by their parents. It could be possible that the money would be all that they would care about and lead to greed in a subtle way.

Financial dependency isn’t a good thing to have, because if you’re tied to one source of income it could be harmful. In the context of allowance in the real world, let’s say a person has a job. He uses that job as his only source of income and makes no effort to find another way to make money. He is fully dependent on that one job to support his life. Essentially, this is the same thing that happens to a child with an allowance. Then, when the person loses his job, he would go broke since not only did he fail to budget his money correctly, but he relied too much on the job that didn’t fully rely on him to help. When the kid gets into the real world, it will be much harder for them to gain that financial stability and independence when they’ve been relying on one source of income for many years. Unless that gap can be bridged, it poses a huge issue to many families. Simply because of allowances, these issues have been brought forth.

While some may argue that giving a child an allowance is a splendid way to introduce them to money and the financial world in general, in the long run it ends up being a negative thing. For example, a Business Insider article states:

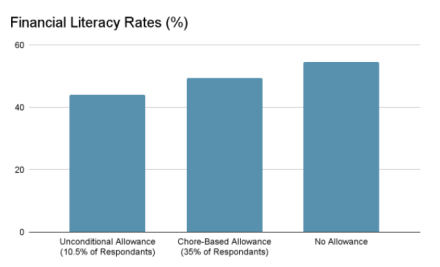

“According to the 2000 Jumpstart Coalition survey “Improving Financial Literacy—What Schools and Parents Can and Cannot Do,” 35% of the total respondents, American high school seniors, received an allowance based on chores, and 10.5% received an unconditional allowance. Those who received no allowance had the highest mean financial literacy score of 52.5%. Those who received an allowance dependent on chores followed closely, at 52.1%. But those who received an unconditional allowance—in other words, those children who parenting experts say should have the best money habits—had the lowest rates of financial literacy (49.1%).”

A visual representation of this:

The stats give you all the information you need.

Yes, it may seem that the child at first could have a jumpstart in their financial education, but in the long run it’s proven that an allowance can worsen financial literacy. The allowance would be pointless, and it could result in them spending all the money they earn. The reason behind this? Actual financial discussion and incorporation into the family isn’t involved. Rather than giving that child an allowance to “develop” their financial knowledge, one could explicitly teach them about financial literacy or give them the resources they need to do so themselves. There’s a load of different alternatives, and the internet today only expands them. They just need to be used.

In conclusion, many parents worldwide give their children allowances for work or even unconditionally. With the popularization of this, the effect it has on people is only increasing. However, allowances aren’t a fantastic way to introduce financial literacy to children, since it gives youngsters a limited picture of the financial world and makes them monetarily reliant on their parents or others. Every step towards changing this for the benefit of children helps, small or large, parent or not!