In our time, data is a new commodity (like unrefined gold) from which we can derive ideas, insights, knowledge, etc. Basic skills in acquiring and analyzing data are essential skills for modern skilled workers. In this post, we consider a problem of web scraping crypto prices and determine if conditions for triangle arbitrage exist, based on these prices.

There are many tools to scrap crypto prices (see [1-6]). We use python package yfinance to scrap prices of crypto and fiat currencies.

First of all we load the required packages with the following commands:

import pandas as pd

import yfinance as yf

Now we can scrap crypto prices with the following command:

df=yf.download(tickers=’BTC-USD’,period='48h',interval='1m')

This command downloads BTC-USD prices over the last 48 hours with interval of 1 minute into df.

We can do the same for other crypto prices and calculate ROIs on triangle arbitrage.

The script below accomplishes this task. ROI is return on investments in triangle arbitrage without trading fees and ROI1 is return on investments in triangle arbitrage with trading fees of 0.1%.

import pandas as pd

import yfinance as yf

def download_data(t1,t2,t3):

p1=t2+"-"+t1

p2=t3+"-"+t2

p3=t3+"-"+t1

p1a=t1+"-"+t2

p2a=t2+"-"+t3

p3a=t1+"-"+t3

df1=yf.download(tickers=p1,period='48h',interval='1m')

df2=yf.download(tickers=p2,period='48h',interval='1m')

df3=yf.download(tickers=p3,period='48h',interval='1m')

return [df1,df2,df3]

def process_data(t1,t2,t3,df1,df2,df3):

p1=t2+"-"+t1

p2=t3+"-"+t2

p3=t3+"-"+t1

df1['Datetime']=df1.index

df1n=df1[['Open']]

df1n.rename(columns={'Open':p1},inplace=True)

df2['Datetime']=df2.index

df2n=df2[['Open']]

df2n.rename(columns={'Open':p2},inplace=True)

df3['Datetime']=df3.index

df3n=df3[['Open']]

df3n.rename(columns={'Open':p3},inplace=True)

print(df3.head())

df=pd.merge(df2n,df1n,on='Datetime')

print(df.head())

df=pd.merge(df,df3n,on='Datetime')

df['roi']=abs(1/(df[p1]*df[p2])-1/df[p3])*100

df['roi1']=df['roi']-0.1

print(df.head(20))

print("averages ",df['roi'].mean(),df['roi1'].mean())

return df

#main

t1="USD";t2="BTC";t3="ETH"

[df1,df2,df3]=download_data(t1,t2,t3)

print(df1.head())

process_data(t1,t2,t3,df1,df2,df3)

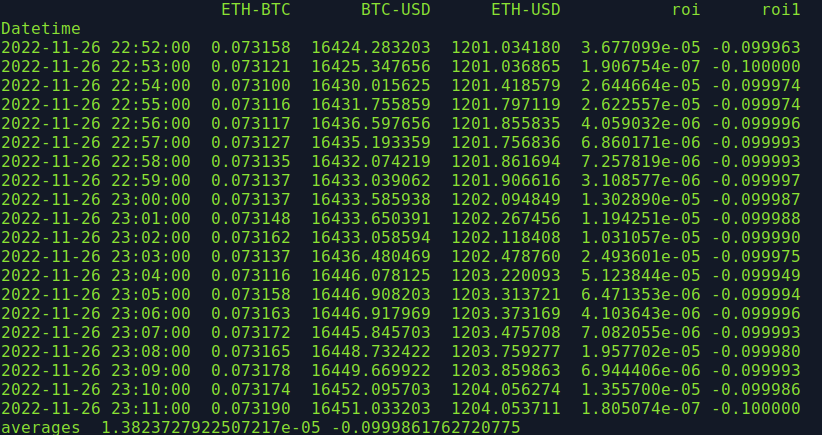

The results are shown below.

As we can see, for those traders who have opportunities to trade cryptos without trading fees, there are opportunities to get small positive ROI in triangle arbitrage USD_BTC_ETH. These opportunities disappear when trading fees are applied.

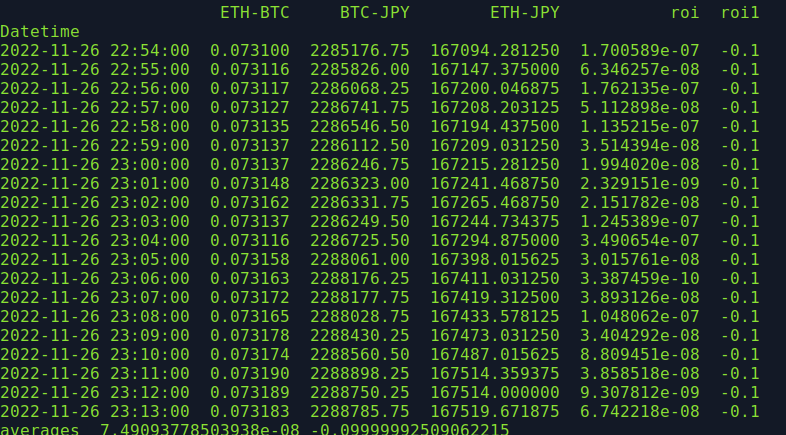

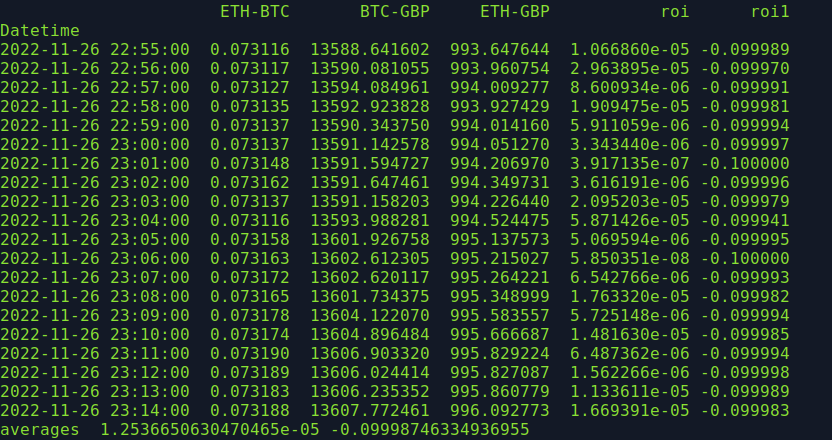

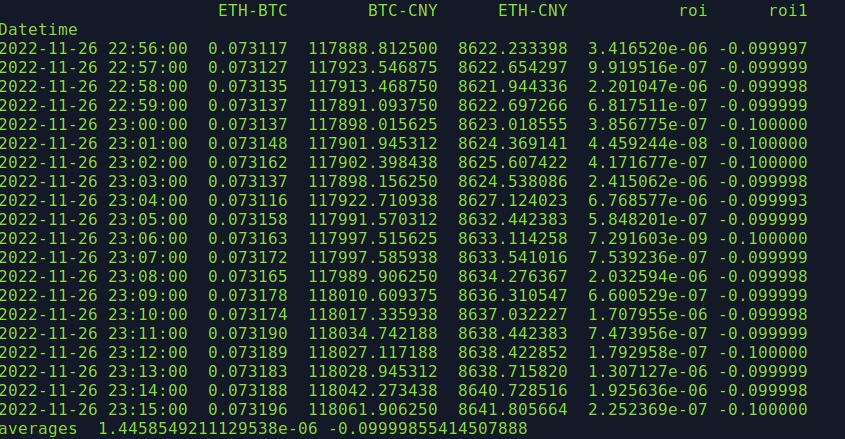

With other base currencies (EUR, JPY, GBP, CNY) we get similar results, which are shown below.

References:

[1] https://beautiful-soup-4.readthedocs.io/en/latest/

[3] https://zzhu17.medium.com/web-scraping-yahoo-finance-news-a18f9b20ee8a

[5] https://www.scrapehero.com/scrape-yahoo-finance-stock-market-data/

[6] https://levelup.gitconnected.com/yahoo-finance-web-scraping-with-r-5584d226c3a6