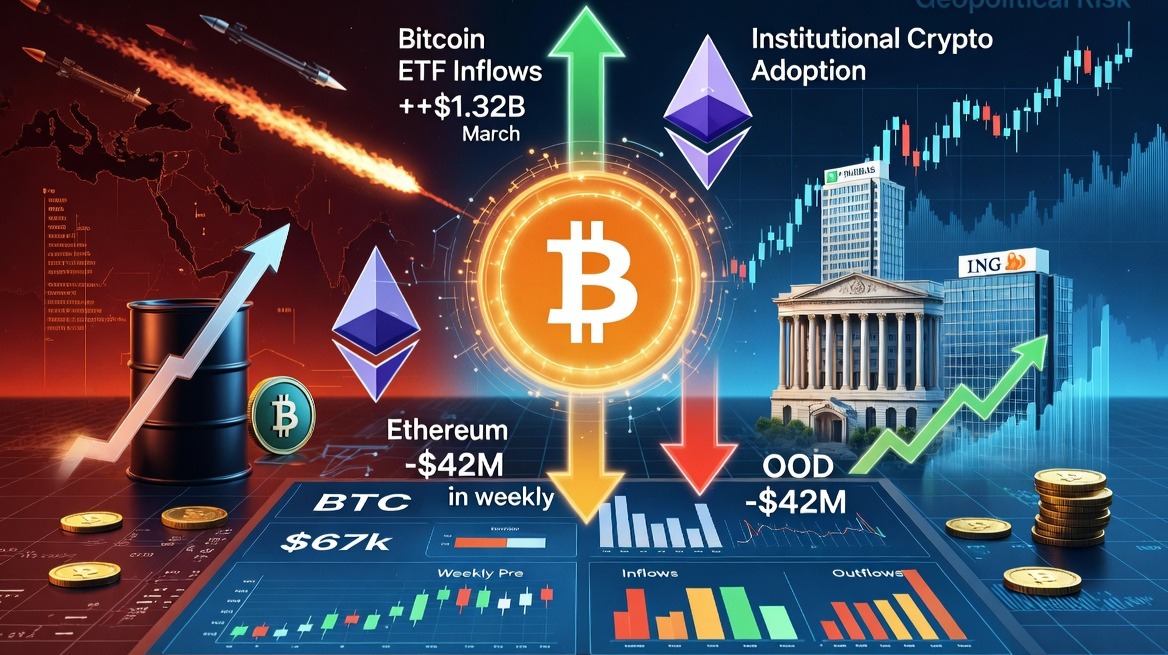

The year, which began with great hopes, entered a period of escalating geopolitical tensions and market uncertainty approximately five weeks ago, following the US and Israeli missile attack on Iran. While oil prices continued to rise during the uncertain past week, precious metals and stocks experienced significant declines. Cryptocurrencies also had a tight and directionless week; Bitcoin neither fully proved a safe haven nor faced intense selling pressure. BTC, which was at $66,500 on February 28th when the conflict began, was trading in the $67,000-$67,600 range at the time of writing. Although there was a weekly decline, it showed more resilience compared to other assets amidst the chaos. Bitcoin's performance is significant, but the main factor determining market direction remains ETF inflows.

The week beginning March 30th closed with a net positive inflow of $22.34 million into Bitcoin ETFs. Although the week saw volatile movements, the overall balance remained positive despite strong inflows and sharp outflows. Monthly data offers a clearer picture. Bitcoin ETFs, which closed negatively for four months from November to February, finished March with a net inflow of $1.32 billion. During the same period, the BTC price increased by 1.8%. This recovery after five months of negative closing in Bitcoin is an indication that investor interest is regaining strength. The main question here is: Are these inflows a temporary reaction or the beginning of a recovery process? The current data suggests that the market has entered a new accumulation cycle.

Ethereum ETFs had a more challenging week. While limited inflows were seen in the early days of the week, the situation reversed in the last two days. With an outflow of $71.17 million on April 2nd, spot ETH ETFs closed the week down $42.15 million. The five-month negative closing streak that began in November continued in March. Although the ETH price declined in the first days of April, March ended with a 7.14% gain. This divergence between ETF flows and the spot price is noteworthy. Institutional and individual investors are looking at the same story from different perspectives.

XRP ETFs closed the week with outflows of $3.56 million. After four months of positive performance following their launch in November, these products experienced their first negative close in March with outflows of $31.16 million. Such corrections can be considered normal for new products. Solana, however, exhibits a different divergence. While there were limited outflows on a weekly basis, the uninterrupted positive flow since its launch in October 2024 shows that Solana has secured a permanent place among institutional investors. In recent weeks, VanEck, Fidelity, and Grayscale have updated and revised their existing spot Bitcoin and altcoin ETF applications to the SEC; although there were no new applications, the interest of large institutions and the activity in the process continue.

Developments in Europe show that crypto assets are solidifying their place in the financial system. BNP Paribas' inclusion of Bitcoin and Ethereum-indexed crypto-linked ETN products on its investment platform is one of the most concrete examples of this transformation. The important aspect of this step is not just the product diversification. The ETN structure offers investors access to price movements without directly holding digital assets, while paving the way for owning crypto through regulated financial instruments. More critically, these products are now offered not only to a limited group of investors, but to a wide segment ranging from individual investors to private banking clients. This indicates a new threshold in the accessibility of crypto assets. The fact that the Netherlands-based ING Bank has begun offering similar products on its banking platform used by clients in Germany, the Netherlands, and Belgium shows a steady expansion of institutional crypto infrastructure in Europe.

ETFs are now at the heart of the crypto ecosystem. The figures point to a clear divergence. The strong are coming to the forefront, while the uncertain are lagging behind. Even in a period of increased geopolitical risk, the continued institutional interest demonstrates that crypto assets are no longer an alternative, but a permanent part of the financial system. From this point on, the real distinction is not whether crypto will be included in portfolios, but which assets will be permanent fixtures in this new order.