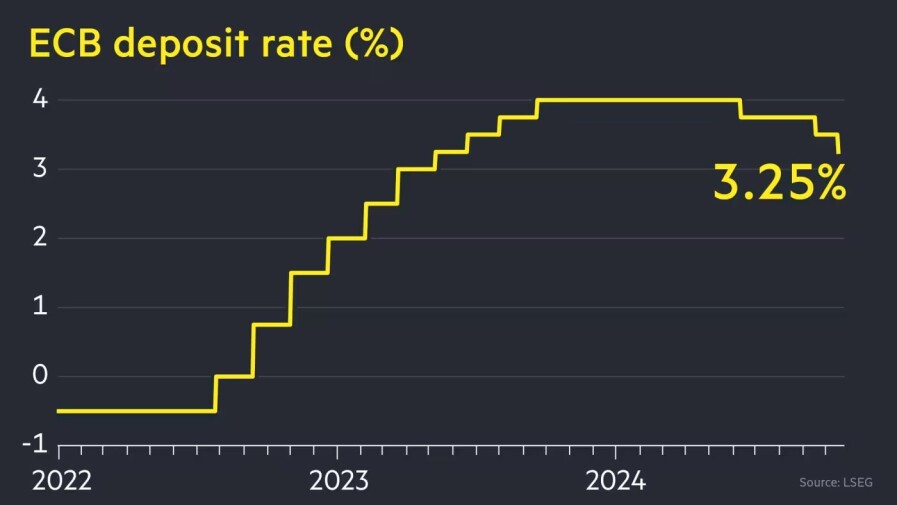

The ECB has cut interest rates for the first time in 13 years at two consecutive meetings, reducing the benchmark deposit rate by 25 basis points to 3.25%, the lowest level since May 2023. The ECB also reduced the main refinancing rate from 3.65% to 3.40% and the marginal funding rate from 3.90% to 3.65%. The decision text emphasized that the disinflation process in the Eurozone is on track. Speaking after the decision, President Lagarde said, "Recent data point to a more sluggish recovery. We expect a gradual recovery in household spending."

Eurozone inflation fell to 1.7% on an annual basis in September, falling below 2% for the first time in more than three years. The fact that the latest interest rate cut was made only five weeks later and with very little economic data shows the ECB's concerns about growth. The euro has lost more than 2% against the dollar in the past month as expectations grew that the ECB would cut interest rates faster than the Fed. The euro weakened to $1.083 after the announcement. Investors in swap markets are expecting four or five quarter-point rate cuts by the middle of next year.

The German Federal Statistical Office (destatis) announced that corporate bankruptcies increased by 13.7% in September 2024 compared to the same period last year. This increase was considered a reflection of the general economic stagnation and global recession experienced in Germany. The highest bankruptcy rate was seen in the transportation and storage sector, with 10.8 bankruptcies per 10,000 companies. The transportation and storage sector is followed by the construction sector. In addition to corporate bankruptcies, personal bankruptcy applications also increased by 18% year-on-year, reaching 6,690. Data in Germany indicate difficult economic conditions.

On October 9, the country's annual growth forecast was revised from 0.3% growth to 0.2% contraction. This means that Germany has faced two consecutive years of recession for the first time in the last 20 years, following a 0.3% contraction last year. We can talk about 2 structural problems in the German economy. First, the end of the cheap energy story after the war in Eastern Europe, and the other is the strain on German manufacturing industry caused by excess capacity from China.

Energy-intensive sectors such as chemicals, metalworking and papermaking have been hit particularly hard recently. Although these sectors account for only 16 percent of German industrial production, they consume almost 80 percent of industrial energy. In the past, Germany used to sell cars, chemical products and machinery to China, while buying consumer goods and intermediate products such as batteries from China, through complementary trade structures. However, China now produces most of these products itself and competes with Germany in some areas.

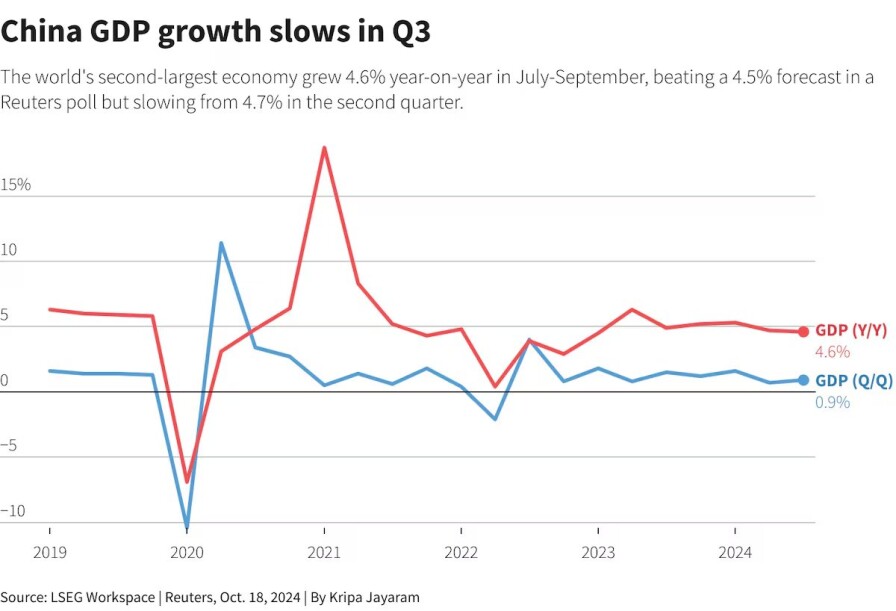

There are concerns about deflation in China. According to data from the National Bureau of Statistics, consumer prices rose only 0.4 percent annually, below expectations. The decline in producer prices accelerated to 2.8 percent. This data highlights China’s deep housing crisis, which has seen household demand fall and the economy stagnate. The Chinese economy grew by 4.6 percent in the third quarter of 2024, exceeding expectations of 4.5 percent, but this growth rate is still below China’s annual growth target of 5 percent.

New measures are also on the table. China’s Housing and Urban-Rural Development Minister Ni Hong announced that bank loans will be increased by 4 trillion yuan (about $562 billion). While weak growth has forced the Chinese government to take stronger stimulus measures, markets expect Beijing to take more steps. However, the government is expected to be cautious, given that past stimulus has led to a real estate bubble. Recent measures include increasing local government debt quotas and implementing local government bonds and tax policies to support the distressed real estate sector.

Vice Minister Liao Min emphasized that local government bonds can help property developers buy unsold homes and reclaim unused land. It was also announced that special treasury bonds will be issued to strengthen the capital structure of major state banks. Last month, the People's Bank of China supported the market by lowering mortgage interest rates and banks' reserve requirements.

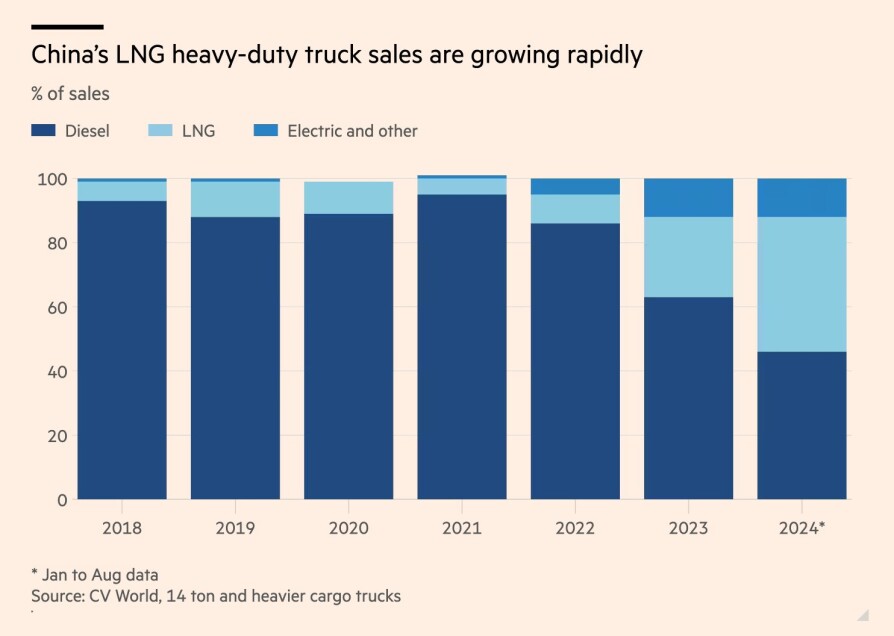

The recent low natural gas prices in the world are encouraging players in the commercial vehicle sector in China to switch from fuel-powered vehicles to natural gas-powered trucks. I mentioned the section on the German economy above. It would be right to read this news along with it. This new trend is reducing the country's demand for oil, causing sales of German Daimler Truck, one of the world's largest truck manufacturers, to fall sharply in China.

While the rapid adoption of electric vehicles is the main trend, significant changes are also taking place in the transportation sector in China. Analysts state that the rapid increase in natural gas-powered trucks, especially in heavy vehicles weighing 14 tons and above, has saturated China's diesel demand and brought the country a little closer to peak oil demand. Speaking to the Financial Times, LNG analyst Sun Yang stated that diesel demand peaked earlier than expected and that LNG is rapidly replacing diesel in heavy vehicles. Diesel use in China is expected to fall by 4 percent this year and this decline is expected to continue in the coming years. Switching to natural gas-powered trucks also helps Beijing ease security concerns about its dependence on imported oil. China imports about three-quarters of the oil it needs, compared with just 40 percent of natural gas.

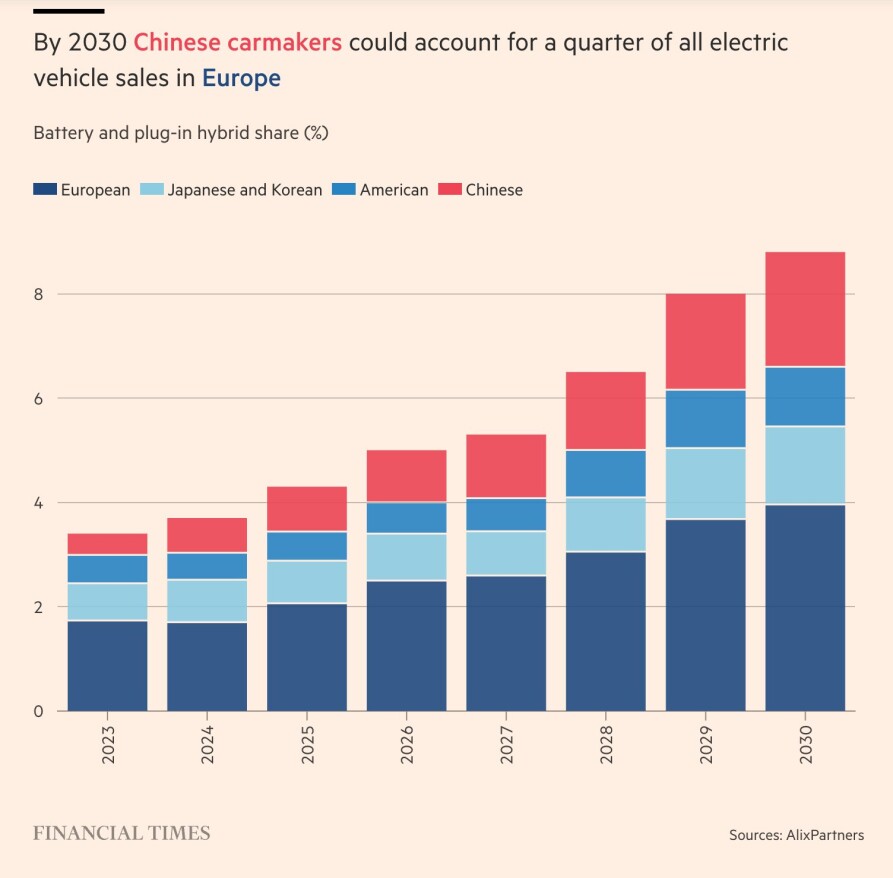

European carmakers are preparing to launch affordable electric vehicle models next year as they prepare for new EU carbon emission targets and strong competition from China. Falling demand and rising costs are putting pressure on European automotive giants. Renault CEO Luca de Meo told the Financial Times that this process will not be easy, but that there is great potential ahead. The slowdown in electric vehicle sales, consumers becoming more cost-conscious, and the reduction of subsidies in major markets such as Germany are making it harder to achieve the targets. Major players such as Stellantis say that the changes brought by the rules are imposing additional costs on manufacturers.

While competition in the market is increasing rapidly; Chinese brands in particular are gaining an important place in the European market with affordable electric vehicles. European manufacturers are trying to stand out with more expensive models, but this puts them at a disadvantage against Chinese manufacturers. High costs and low profit margins are putting pressure on European giants. While the average price of an electric vehicle in Europe is currently over 40 thousand Euros, Chinese brands are selling vehicles at prices around 20 thousand Euros. This difference makes it difficult for Europeans to find a permanent solution in the market.

The information, comments and recommendations contained herein are not within the scope of investment consultancy. Investment consultancy services are provided within the framework of the investment consultancy agreement to be signed between brokerage firms, portfolio management companies, banks that do not accept deposits and customers. The comments in this article are only my personal comments and these comments may not be appropriate for your financial situation and risk return. For this reason, investments should not be made based on the information and comments in my articles.