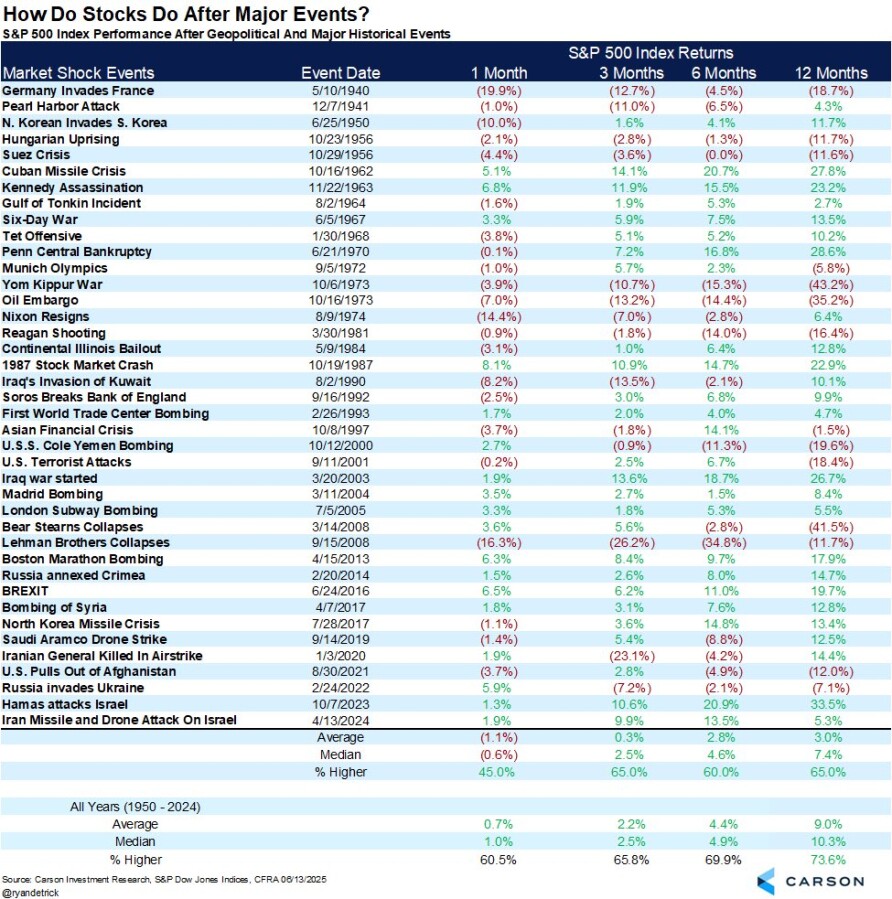

The visual shows the 1, 3, 6 and 12-month performances of the S&P 500 index after major geopolitical and historical events since 1940. In this chain of posts, I examined events that yielded more than 6% negative returns at the end of 12 months and tried to find their common features. I think it is instructive in terms of understanding when the market failed to cope with structural difficulties.

The German invasion of France on May 10, 1940 turned World War II into a full-scale conflict in Europe. Although the US had not yet joined the war, global panic shook investor confidence and there were major sell-offs in the markets. In this environment, the S&P 500 lost 18.7% of its value at the end of 12 months.

The uprising that began in Hungary on October 23, 1956 triggered popular resistance against the Soviet Union and increased Cold War tensions. Instability in Eastern Europe created insecurity in Western markets. During this period, the S&P 500 fell 11.7% in 12 months.

The Suez Crisis on October 29, 1956, broke out with the military intervention of England, France and Israel in Egypt. While the energy supply in the Middle East was at risk, geopolitical tensions made investors nervous. The S&P 500 fell 11.6% at the end of 12 months.

The Six-Day War, which began on June 5, 1967, increased geopolitical risks on a global scale with rapidly escalating conflicts in the Middle East. When concerns about energy supply combined with Cold War tensions, the S&P 500 lost 43.2% at the end of 12 months.

The Oil Embargo, which broke out on October 19, 1973, was triggered by OPEC countries stopping oil exports to Western countries that supported Israel. Energy prices skyrocketed, an inflation shock began and the US entered a period of stagflation. (Stagflation: Inflation combined with high unemployment—the 1973–75 recession was part of this structural problem.) The market reacted strongly to these developments, and the index fell 35.2%.

The assassination attempt on US President Ronald Reagan on March 30, 1981 raised serious concerns about political stability. Fear of a leadership vacuum increased short-term risk perception. However, the interest rate hikes of the early 1980s also had an impact: the Fed implemented sharp interest rate hikes to combat double-digit annual inflation; this increased risk premiums. In this environment, the S&P 500 fell 16.4% in 12 months.

The bombing of the USS Cole warship in the Port of Aden, Yemen on October 12, 2000 raised questions about US security in the Middle East. In addition, the dot-com crash was also taking place: technology stocks fell sharply in 2000–2002; This made the S&P’s losses a trend that preceded them in the US. The S&P 500 lost 19.6% in the first year.

The Twin Towers terrorist attacks on September 11, 2001 created a security crisis unprecedented in US history. As economic activity came to a standstill, investors fled risk. The market, which had not recovered post-dot-com, was already fragile due to the wars of 2001 and later. Following these developments, the S&P 500 lost 18.4% in the 12 months following this development.

The collapse of Bear Stearns on March 14, 2008 was the first major signal of the 2008 global financial crisis. Perceptions of systemic risk escalated rapidly in markets that were in a liquidity crisis. The index lost 41.5% in the following 12 months.

The collapse of Lehman Brothers on September 15, 2008 paralyzed the global credit system. Confidence completely collapsed, central banks were forced to take extraordinary measures. Following this development, the S&P 500 fell by 11.7% in 12 months.

The US's global reputation was questioned on August 30, 2021, with the US withdrawal from Afghanistan and the sudden and chaotic end of the 20-year war. The geopolitical power vacuum and uncertainty increased the perception of risk. There was also economic stress after COVID during this period. The supply chain was disrupted after the pandemic, and recession concerns arose. As inflation data increased, the Fed's tapering and interest rate expectations began to strain the markets. The S&P 500 lost 12% of its value at the end of 12 months.

Russia's invasion of Ukraine on February 24, 2022 created a hot war environment in Europe and increased the pressure on energy supply. There were situational problems in both energy and agricultural products. The Fed's fight against inflation, tight monetary policies, and rising interest rates negatively affected stock values. The S&P 500 fell 7.1% at the end of the year.

In other words, along with every major geopolitical shock, the following common factors have weighed on markets:

Economic cycle stagnation; Oil shock, interest rate hike, post-pandemic recovery, etc.

Inflation pressure & interest rate moves; Post-shock cost increase, tightening of central banks such as the Fed/ECB.

Panic and psychological fatigue; Insecurity of investors who are constantly exposed to major crises.

Credit and liquidity crises; Waves of panic in the financial system in times like 2008.

As a result, these events not only created a sudden shock, but also created a long-term environment of uncertainty and systemic risk. While wars shook investor confidence, energy crises triggered inflation, and financial collapses locked the credit system. Permanent sales occurred because the market perceived such developments not as temporary but as structural threats.

Today's Iran-Israel war, like historical examples, could be a serious test for the market. If the conflict is limited, does not directly disrupt energy supplies, and does not require the intervention of major powers such as the United States, Russia, and China, its impact will be short-term: a few weeks of volatility, an increase in defense and energy stocks, and a limited pullback in broad indices.

However, if the war spreads to the Gulf, if oil shipments through the Strait of Hormuz are jeopardized, and if a direct military conflict occurs between the United States and Iran, this could increase both energy inflation and the risk of a global recession, creating long-term, structural pressure on the market. In short, if the geographic and economic scope of the war is limited, it could cause a temporary shock, and if it spreads, it could cause damage similar to 1973.

The information, comments and recommendations contained herein are not within the scope of investment consultancy. Investment consultancy services are provided within the framework of the investment consultancy agreement to be signed between brokerage firms, portfolio management companies, banks that do not accept deposits and customers. The comments in this article are only my personal comments and these comments may not be appropriate for your financial situation and risk return. For this reason, investments should not be made based on the information and comments in my articles.