As the volatility of early 2026 rattles the technology sector, investors are frantically searching for safe harbors. The high-beta growth trade that dominated the headlines last year is showing cracks, with inflation proving stickier than the Federal Reserve anticipated. In this chaotic environment, the Aquamarine Fund's strategy stands out not for what it is buying, but for what it refuses to sell. A deep dive into the Aquamarine Fund's holdings reveals a portfolio built almost entirely on two concepts: Pricing Power and Customer Loyalty.

Unlike the crowded "AI" trade, Guy Spier has positioned his capital in companies that can raise prices without losing customers. This is the ultimate hedge against currency debasement. Whether it is the ultra-wealthy clientele of Ferrari or the entrenched payment rails of American Express, the theme is resilience over speed.

The "Veblen Good" Defense Mechanism

While consumer discretionary stocks are tanking due to a weakening middle class, one holding in Spier's book continues to defy gravity: Ferrari (RACE). This is the textbook definition of a "Veblen Good"—a product where demand actually increases as the price goes up.

Spier’s heavy allocation here is a bet on the widening wealth gap. In 2026, the mass market is squeezing, but the ultra-rich are spending more than ever. By holding Ferrari, the portfolio captures the upside of global wealth creation without the operational risks of a standard auto manufacturer. It is a luxury goods company disguised as a car maker, boasting profit margins that put Silicon Valley to shame.

💳 THE "TOLL BRIDGE" BUSINESS MODEL

If Ferrari plays offense, the payment processors play defense. The second pillar of this strategy involves owning the "rails" of the global economy.

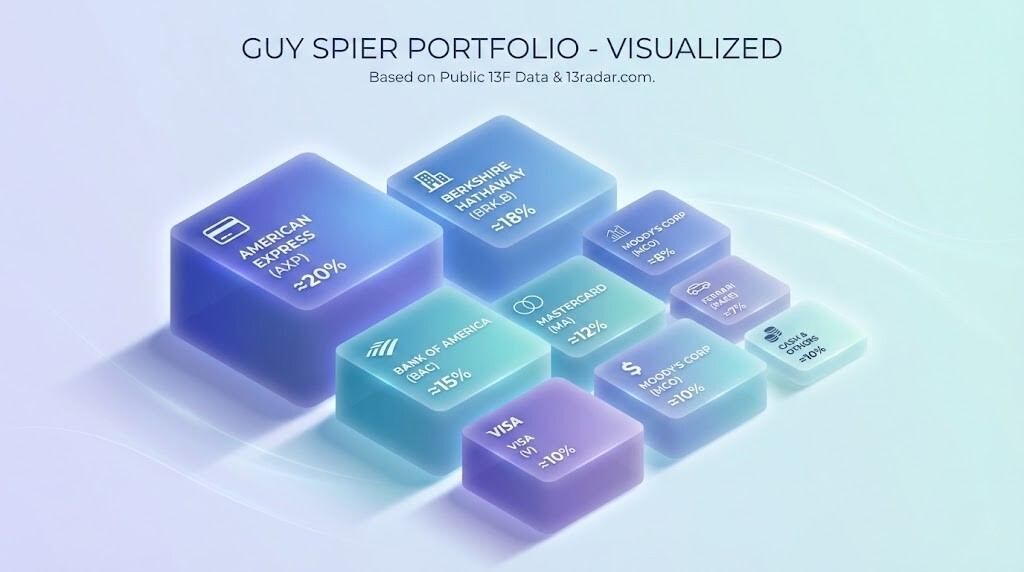

- American Express (AXP):

Benefiting from higher spending volumes and a closed-loop network that captures data both ways. - Mastercard (MA):

An inflation-protected royalty on global GDP. If prices go up, their fees go up automatically.

These companies act as economic toll bridges. You cannot cross the river of commerce without paying them a fee. This business model is virtually impossible to disrupt, providing a steady stream of free cash flow regardless of who wins the next election or what the Fed does with rates.

Ignoring the Noise

The most striking aspect of the current 13F filings is the lack of turnover. While other funds are churning their portfolios to chase momentum, Spier sits on his hands. This inactivity is a feature, not a bug. For investors looking to replicate this high-conviction, low-stress approach, analyzing the guy spier portfolio offers a blueprint for sanity. It proves that you do not need to find the "next NVIDIA" to generate superior returns; you just need to own the best businesses in the world and never sell them.