In a market environment deafened by the roar of AI hype and momentum trading, it is easy to forget the foundational principles that built Wall Street. While retail investors are frantically chasing the next tech breakout, the "Old Money" accounts are quietly moving in the opposite direction. This divergence is most evident when examining the latest moves from Tweedy, Browne & Company.

With a history dating back to 1920, this firm doesn't care about FOMO. They care about intrinsic value. Their Q4 activity is a testament to the discipline required to sit on your hands when everything looks expensive, and to strike only when the math makes undeniable sense.

The "Cigar Butt" Approach in a Growth World

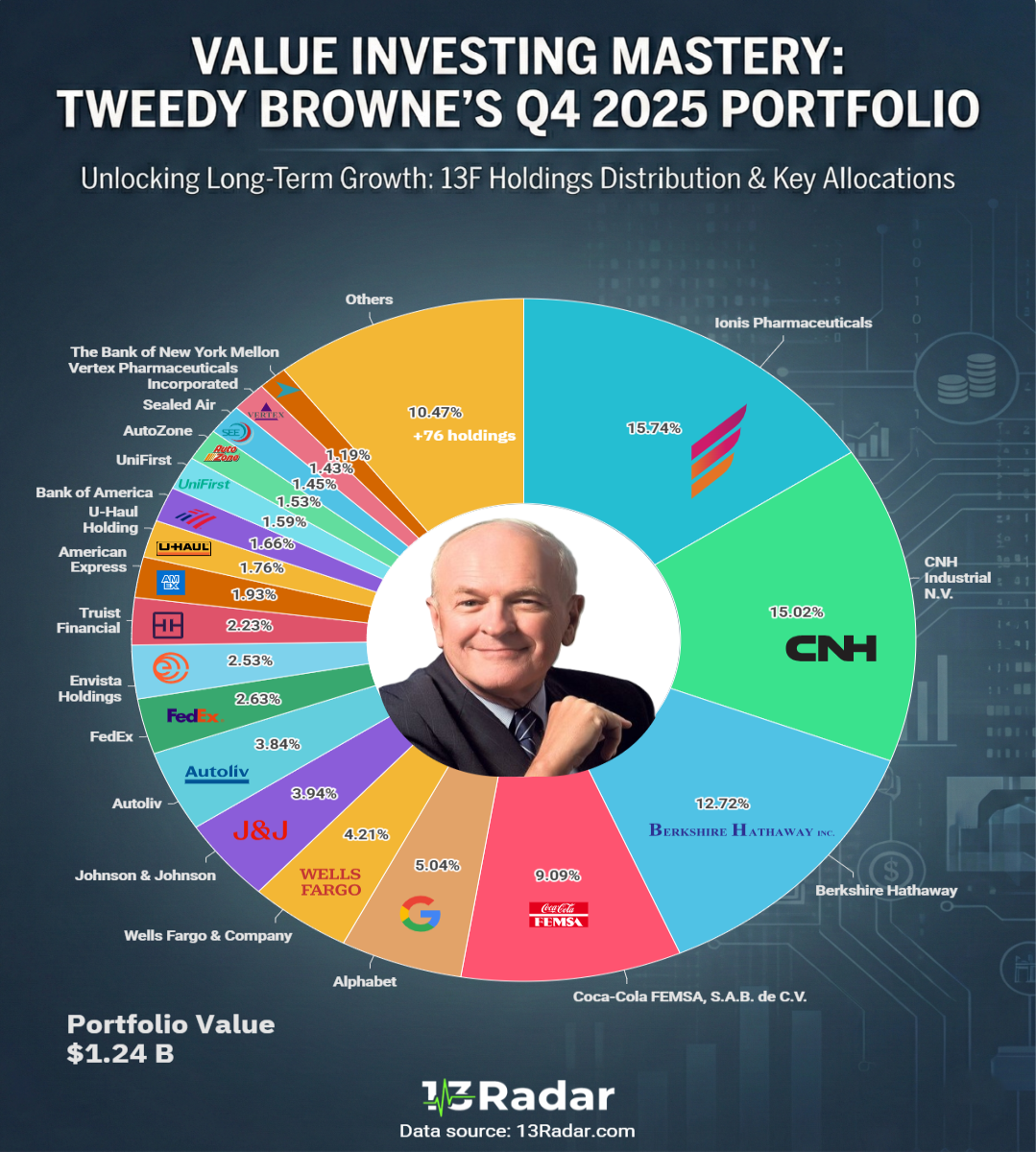

Tweedy Browne has always adhered to the Benjamin Graham style of investing: buying a dollar for 50 cents. In Q4, while the S&P 500 P/E ratios expanded, Tweedy Browne appeared to be digging through the bargain bin of neglected sectors. We aren't seeing them buy the "Magnificent Seven"; we are seeing them accumulate positions in boring, cash-generative businesses—industrials, financial services, and consumer staples that have been left for dead by the growth crowd.

Analyzing the Tweedy Browne portfolio Q4 2025 reveals a clear preference for companies with tangible assets and shareholder-friendly management (dividends and buybacks) over pie-in-the-sky growth promises.

🚩 RED FLAGS: What They Are Selling Matters More

Sometimes, what a guru sells is more telling than what they buy. In recent quarters, Tweedy Browne has shown a willingness to trim positions that have reached their valuation targets.

- Valuation Discipline: If a stock price exceeds their calculation of intrinsic value, they sell. Period.

- Cash Buildup: A reduction in total equity exposure often signals that they struggle to find bargains, serving as a silent warning to the broader market.

- Avoiding the Crowd: You likely won't find the trendiest stocks in their top holdings, protecting them from the inevitable mean reversion.

Why "Boring" is the New "Safe"

The beauty of Tweedy Browne's strategy lies in its defensive nature. By focusing on high-quality companies with low debt and steady cash flows, they build a portfolio designed to survive a recession, not just thrive in a bubble. For investors worried about a 2026 correction, their portfolio offers a blueprint on how to construct a "bunker" against volatility without going typically to cash.