In the hyper-competitive semiconductor and Electronic Design Automation (EDA) sectors, data is the ultimate currency. While retail traders often obsess over synchronized earnings calls and press releases, quantitative funds deploy sophisticated algorithms to scrape SEC databases seconds after a document drops. The true measure of a company's fundamental trajectory is frequently hidden within the rigid, unglamorous structure of mandatory regulatory disclosures.

The Mechanics of Executive Accountability

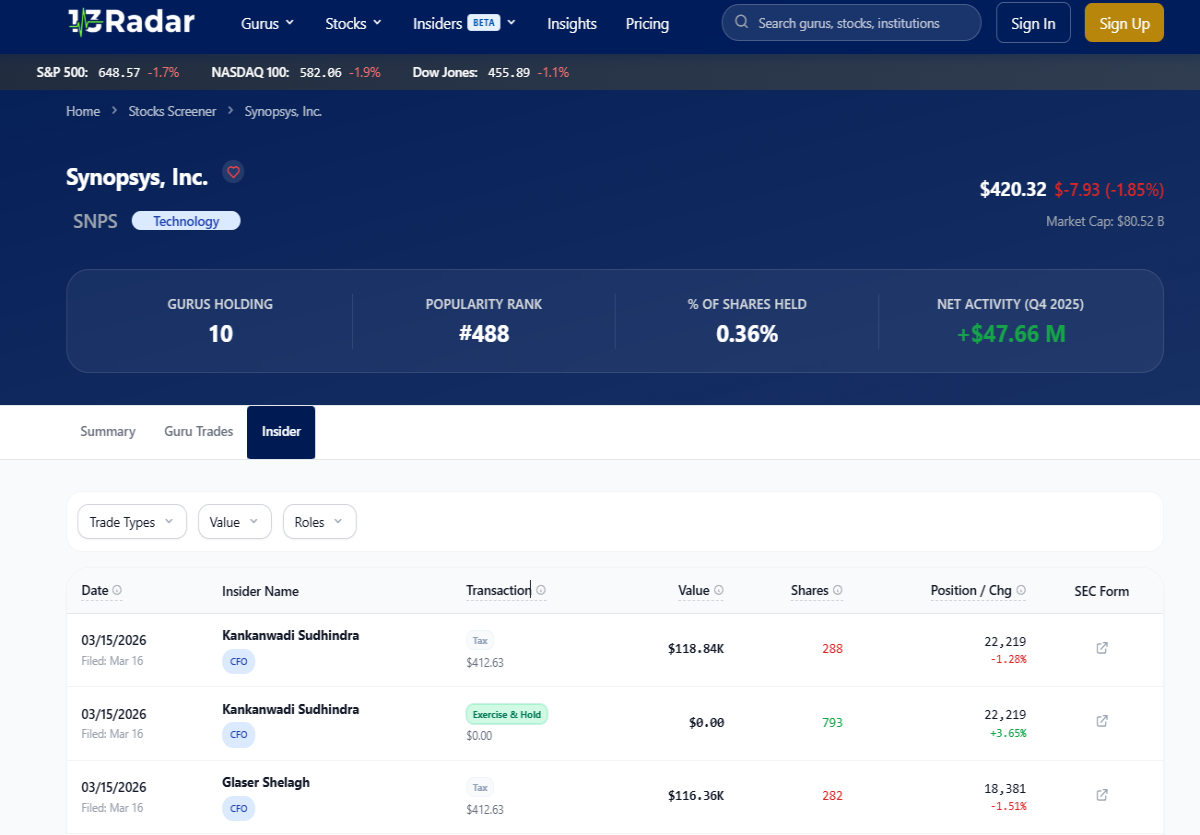

When corporate officers at foundational tech firms alter their personal equity positions, federal regulations mandate strict and immediate public disclosure. Recent Form 4 filings show a noticeable increase in executive sales across major tech companies, reflecting a broader macroeconomic trend of liquidity management amidst extended market highs. However, distinguishing between routine, scheduled vesting events and sudden, discretionary offloading is what separates market noise from actionable institutional intelligence.

Deconstructing the Disclosure Architecture

The Anatomy of a Regulatory Submission

To extract real value, analysts look beyond the top-line dollar amount and focus on the metadata:

- Transaction Codes: Deciphering whether an event is an open market purchase (P), a scheduled sale (S), or an options exercise (M).

- The 48-Hour Window: Monitoring the precise timing of the submission relative to the actual transaction date to gauge administrative urgency.

- Footnote Context: Reading the fine print that explains the presence of 10b5-1 automated trading plans or specific tax-withholding mandates.

Transforming Raw Data into Institutional Strategy

Raw regulatory filings are merely isolated data points; their actual predictive value lies in aggregation and historical comparison. To accurately model the behavioral baseline of a specific leadership team, fundamental analysts must review the historical ledger in its entirety. Examining a specific SNPS Form 4 submission provides the granular transparency required to assess actual leadership conviction. Integrating this precise regulatory timeline into fundamental valuation models allows sophisticated investors to anticipate structural shifts before they ever manifest in quarterly revenue statements.