As many of you who have been around for a year may know, the DeFi space was absolute madness last summer. There’s a reason people refer to it as “DeFi summer.”

Projects were popping left and right. Every day we’d get a new protocol offering unbelievable APY’s for staking obscure shitcoins that were minted just hours ago. I remember vividly throwing a sizeable (for me) amount of money at a protocol offering me 64,000% APY. But because I was a DeFi novice, I had no idea what impermanent loss (IL) meant, and watched that money thin out as the token kept losing its value minute after minute. Now I get what they mean when they say that you’re not a true DeFi degen until you've been rug-pulled or rekt to IL at least a few times.

Bitter nostalgia aside, I’m fond of these memories because that’s what sparked my interest in DeFi. I was hooked. So I made a promise to myself to be a bit more responsible, do proper due diligence on the projects I invest in and differentiate between investing and gambling.

The important take from the above is that everything DeFi-related last summer took place on Uniswap. At that point, Sushiswap, 1inch, PancakeSwap, and all the other DEXs weren’t a thing. We had no other way to interact with these obscure protocols. There was only Uniswap.

Little did I know that there was something cooking. In September 2020, as I was browsing through Crypto Twitter, I saw plenty of people hyped about a Uniswap airdrop. So, I checked if I was eligible. And lucky me, I was! But so were almost all the people who had used the exchange for more than a couple of swaps. We all got at least 400 UNI tokens.

At this point, I sat down and started thinking - the airdrop was worth well over $1.5K at the time I could redeem it, which, for many, was a sizeable chunk of change. But in my case, I had no immediate need for that money, I knew that Uniswap was (at the time) the only major automated-market maker and DEX and even if others came (which they did), it would have the first-mover advantage. So I HODL'd. In fact, I even bought some more.

Fast forward to a few days ago, my UNI airdrop is worth more than $12K. My whole bag was worth a bit more, so being the diligent DeFi ape that I consider myself to be, I was thinking of ways to put that money to work. Sure, gains are nice, but after all, it’s dormant money - I don’t plan on selling UNI anytime soon because I think DeFi is just beginning. So how do I leverage my UNI to get access to additional capital?

That's where Yield Credit came in. At this point, if you’ve read any of my previous articles, you should know that I’m long-term bullish on Yield Credit. It’s a decentralized lending protocol where interest rates are fixed. And you’ve got tons of assets you can use as collateral to borrow against. UNI is one of them. Currently, there are more than 30, but every asset that has a Chainlink oracle can be integrated. So, in the near future, the collateral choice would be vastly expanded, though it’s still greater than existing competitors.

Borrowing $5K

To start off, I opened up the Yield Credit dApp and I created an offer. I wanted to propose a good deal so someone could take me up on it, but more than that - I wanted to get a loan so I could buy more YLD.

Here’s how it works. First, you hop on the dApp, and you choose whether you want to lend or to borrow - I wanted to borrow.

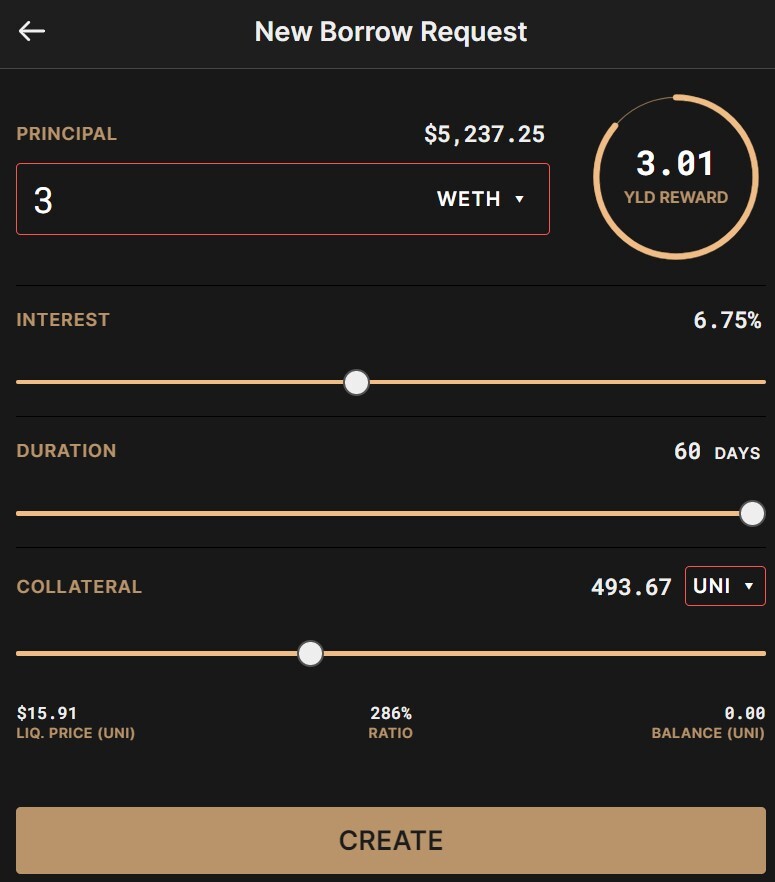

Second, you create an offer - you basically stipulate the terms of the contract - how much you want to borrow, how long do you want the contract to last for, what interest rate you’re willing to pay for it, and you select your collateral:

(This is how my offer would look now, but I created it three days ago and there are very slight differences as you’ll see in the following screenshot).

And that was that. My offer was there, I wanted to get 3 WETH, putting a bit less than 500 UNI in collateral so I have a nice leeway in case prices drop. With the WETH I would buy YLD, because my belief is that it will definitely grow by more than 6.75% (my interest) in the next 30 days.

And this is where it gets even better - Yield Credit rewards me as a borrower! If someone took me up on my offer, they would get the 6.75% interest, and I would get a bit more than 3 YLD in reward! At the time, it was worth a bit more than $300, and if my predictions are correct, at the time I repay my loan, it would be worth a whole lot more. This would offset the interest I have to pay, making that loan not just free, but net profitable. I couldn’t get that anywhere else but at Yield Credit.

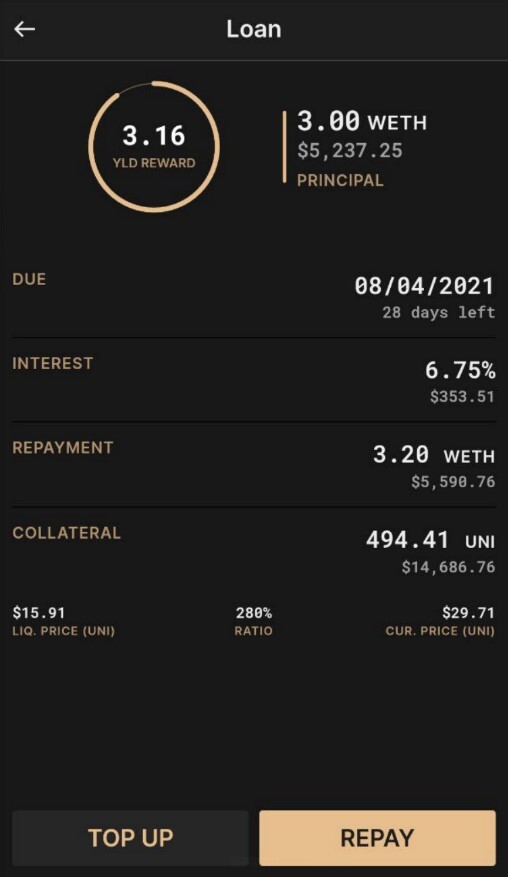

So I went ahead and just a few minutes later, someone took me up on my offer. Exciting!. Here’s how it looks now that I have the loan active:

As you can see, the interest I have to pay is around $353. The reward I get for repaying this loan (at current rates) is worth $357 (3.16 x $113 current price). Well, how about that? As it stands, barring any severe market downturns which no one is protected from anyways, I’ve borrowed 3 WETH for free.

Staying true to my investment strategy and faith in this project I did buy more YLD. Here’s the screenshot:

What’s Next?

I plan to let my investment play out. Hopefully, the price of YLD will go up as there are more and more developments the team is working on. And my profit will be even higher as a result.

Just yesterday the Yield Credit team revealed their Chainlink integration which was immediately published on Chainlink’s media channels. Yield Credit is starting to get serious exposure. It’s still sitting on a relatively small market cap of just over $30 million and when I compare it to that of existing competitors like Aave and Compound, I can see plenty of room for growth.

Not only that, but Yield Credit does offer something better than both because on those platforms borrowers are not incentivized to borrow at all. And for lenders, it's not much better either, as they get APY’s that are trending towards 0% because of the pooling dynamics. A race to the bottom. These are just some of the benefits.

The funny thing is I also received the 1inch latest airdrop in one of my wallets. Seeing how things played out with UNI, I definitely have no intentions of selling that one either, so I might tap into Yield Credit to see what my options are.

That’s pretty much it. I’m excited to see how all this pans out. If you have any questions about Yield Credit, you can check the official website or follow them on Twitter.

Additionally, their Telegram group is super helpful, you can check it out here.

That’s all folks, I’ll also be doing an explainer on the benefits of holding the YLD token soon and how to get your hands on it, so stay tuned for that!