The space of decentralized finance (DeFi) has exploded over the past year. It has become one of (if not the) most-heavily discussed areas, touted by many to be the future of finance. There’s serious merit to those claims, especially looking at how DeFi has grown over the past year alone.

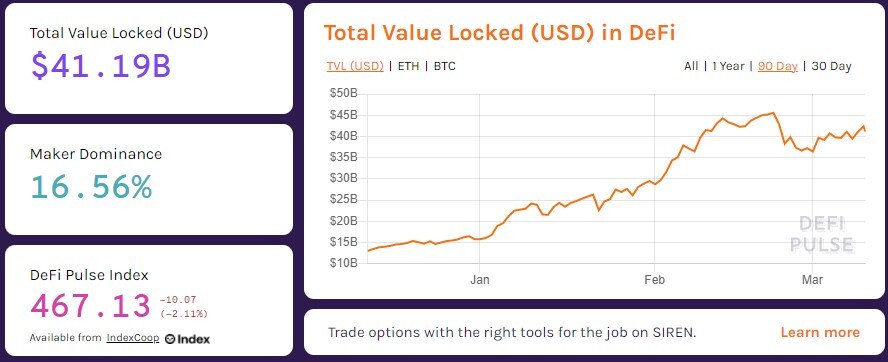

Data from DeFi Pulse reveals that there’s currently over $41 billion worth of value locked across various protocols.

For comparison, this figure in January 2020 was just shy of $700 million, indicating a total increase of more than 5,700%.

Looking at the DeFi Pulse index chart, which reveals how much value is locked in separate protocols, we can see that Maker, Compound, and Aave are at the forefront. They all share a common thread - they’re decentralized lending protocols.

In other words, lending (as well as automated-market making in the face of several DEXs such as Uniswap, Sushiswap, 1inch, etc.) is where all the rage is. But that’s not a surprise - after all, lending is also where all the rage is in traditional finance.

And while the value proposition is truly remarkable, it’s also flawed. Lending is a two-sided process, and for some reason, the DeFi space hasn’t yet recognized the value of the borrower. Aave, Compound, and Maker, as well as virtually any other protocol (with the exception of one, wink, wink), fail to provide incentives to the borrower. This, coupled with many inherent improvements and tons of added value, is where Yield Credit steps into the picture.

What is Yield Credit?

Please note that I’m not a part of the core team behind the project. I’m merely a contributor who has been following it for quite some time and believe in its value proposition.

Yield Credit is a decentralized lending protocol that has been in the making for quite some time now, and the team’s tireless efforts came to fruition recently with the launch of their mainnet product - the Yield Credit Platform itself.

In essence, it’s a peer-to-peer decentralized lending platform that is inherently different from existing solutions such as Aave and Compound.

To make it easier and more systematic, I’ll put the main characteristics forward:

Fixed Interest Rate

The problem with interest rates at Compound and Aave is that they are floating, and they are trending towards 0% because of the pooling. This makes it a lot less enticing for the lender as the system itself makes it a race to the bottom.

With Yield Credit, loans are individualized (not pooled), and users can set fixed interest rates for a specified period of time. Presently, the maximum interest rate a lender can set is capped at 12.5%, the maximum duration of the loan is 60 days, and the maximum loan amount is set at $50,000.

Even at a 2% monthly interest rate (which I assume is a lot less than what users would be willing to pay in the most raging bull market we’ve ever seen), this would put the APY at 24% - a lot more than what Aave and Compound are ever going to achieve. However, this 24% assumes the lender does not then roll the interest earned on loans into the initial principal offered on subsequent loans - i.e. in the absence of compounding. Compounding the interest earned will give a higher still APY

Another benefit of that is a certainty. You won’t have to worry about what your APY would look like tomorrow - it’s fixed, you know what to expect.

Incentivized Borrowers

This is a complete game-changer in the field of DeFi lending. No other protocol (to my knowledge) incentivizes borrowers.

For accurate repayment of their loans, borrowers receive a reward in the form of YLD tokens (the protocol’s native token).

Here’s how it looks in actuality:

This is a lending offer. Someone has put up 380 UNI for lending at an interest rate of 2.25% for 15 days. The potential borrower stands to make 1.52 YLD in rewards for repaying the debt, which is currently $172.88. The more people use the platform, the greater the face value of the YLD reward (in USD terms) will be! The interest he has to pay is $274.34.

So, to make matters easier (barring protocol fees for simplicity):

- You borrow $12,192.89 (380 UNI at current rate) at 2.25% ($274) interest for 15 days.

- For repayment, you get a 1.52 YLD ($172.88) reward.

- The reward essentially offsets the interest, making it even more appealing for the borrower.

So, not only are lenders incentivized through a fixed rate but so are borrowers - making the entire lending process mutually beneficial. Acknowledging the importance of both parties is a massive alpha which, in my opinion, will be a huge benefactor going forward.

Massively Expanded Collateral Options

Aave and Compound, as well as any other decentralized protocol, rely on their governance to determine which asset would be integrated and made possible to collateralize.

Yield Credit fixes that in the most elegant way. Any token based on the ERC-20 protocol standard (for now, more exciting stuff to come) with an integrated Chainlink Oracle can be selected as collateral.

The platform launched with a massive number of coins that can be put forward as collateral. These include but are not limited to YFI, AMPL, ANT, SUSHI, LINK (duh), USDC, WBTC (!!), USDT, 1INCH, UNI, and so forth. Just take a look at the below list of currently available collateral options:

The main benefit of DeFi loans is that you shouldn’t have to sell your crypto to access more capital. But up until this point, you were limited in what coins you could collateralize because Aave and Compound don’t support that many. In other words, you’d have to convert to supported crypto and put it up as collateral to access more capital.

No longer is this the case. The most popular assets are already supported on Yield Credit, and users don’t have to decrease their exposure to access funding.

The YLD Token

I know that regardless of how good the protocol is, in crypto, it oftentimes boils down to “when moon,” so let’s try to answer this question.

The native token of Yield Protocol is YLD (don’t get it confused with the YLDapp crap - it carries the same ticker, but unless you’re a fan of centralized solutions, in which case DeFi is not where your attention should be.)

In its essence, it’s a utility token, and it brings a few benefits to its holders who use the platform. These include:

- Lenders and borrowers who stake YLD are entitled to discounts on platform fees.

- Lenders and borrowers who stake YLD enjoy lower loan liquidation ratios.

When discounts are activated for the borrower, they will gain a -2.5 to -5 reduction in the liquidation ratio. Keep in mind that this may sound like a little, but the difference between being safe and being liquidated is sub 0.1%.

More utilities can be added up as needed.

The token is also mintable and burnable. It’s mintable because borrowers need to receive incentives. It’s burnable (and that’s the hot take) because all protocol fees go towards burning tokens. In essence, this eliminates the possibility of infinity minting through borrower rewards and creates healthy token economics.

Now, for those of you interested in “when moon,” I’ve a few things to say. First, the current market cap of the protocol sits at $33 million. Compare that to the billions that Aave and Compound sit on, and you can get an idea of where this might go. Also, if you aren’t convinced that it can claim at least a certain percentage of the lending market, please go back and read up on everything I’ve written once more. This is a value proposition that is hard to ignore or overlook.

Next up, there’s a highly professional team behind it who have delivered absolutely everything they’ve promised so far. With a clear roadmap and exciting integrations ahead, as well as the mainnet shipped, Yield Credit is, in my opinion, one of the next big things in DeFi.

All in all, this is the introduction to Yield Credit.

I plan on expanding this into a series, explaining many things, as well as giving potential strategies as to how users can benefit from using the protocol. Some of the upcoming writeups include, but are not limited to:

- How to borrow on Yield Credit

- How to lend on Yield Credit

- Terms everyone should be aware of (collateral, liquidation, liquidation ratio), etc.

- Some strategies in light of the current market structure.

These are the project's official resources:

Website: https://www.yield.credit/

Twitter: https://twitter.com/YieldCredit

Telegram (discussion group): t.me/yieldchat

That’s it for this, catch you soon :)

Now, here’s my tip jar. Any contribution is much appreciated as it helps me create more content and be more devoted to it.

ETH Address: 0x4179FF49AF205f30abFAb83d0b70687c2dfa2B3a

BTC Address: bc1ql47f2pxraxz3vny8ss5y2l3hzhqvh8m0a7t4g4