Hey folks, so if you’ve been following my articles for a while, you’ll know that I have a strong affinity and interest to find high yield plays, whether they be in stablecoins or in blue chip cryptocurriencies.

Today I’m going to be taking up the counter argument for why even though some of these yields might be extremely attractive, it’s important to weigh out your options and figure out what might be the best investment is for you in correspondence with your personal appetite for risk.

First, a bit of a primer…

Stablecoins have been losing ground for a long time

https://www.tradingview.com/script/HyKvfeEJ-Stablecoins-market-cap/

https://www.tradingview.com/script/HyKvfeEJ-Stablecoins-market-cap/

Since March 2022, the stablecoin total marketcap has been slowing draining away, going from ATH’s of around $160 billion to around $120 billion which is where it sits today — a nearly -25% decrease in about the last year and half.

If you’ve been in the crypto space for a while, you may be thinking… “so what? Most of my altcoins have lost 95% from ATH’s!” — this I won’t argue with, but what’s interesting is that stablecoins are supposed to be crypto’s flight to safety. And considering that during that same period of time the total crypto marketcap has had an even worse drop (roughly -50%), I think it’s safe to say that the reason why the stablecoin market has decreased, isn’t because it’s been flowing into alts.

So why are Stablecoins leaving the market?

The first take could be because even the so-called flight to safety may not be that safe anymore. Last March especially when we saw some huge banks like Silicon Valley go under, we saw many stablecoins, even overcollateralized ones like $DAI and $LUSD take significant depegs, which caused a great number of people (even at significant losses) exit into fiat as the crypto-sky was falling.

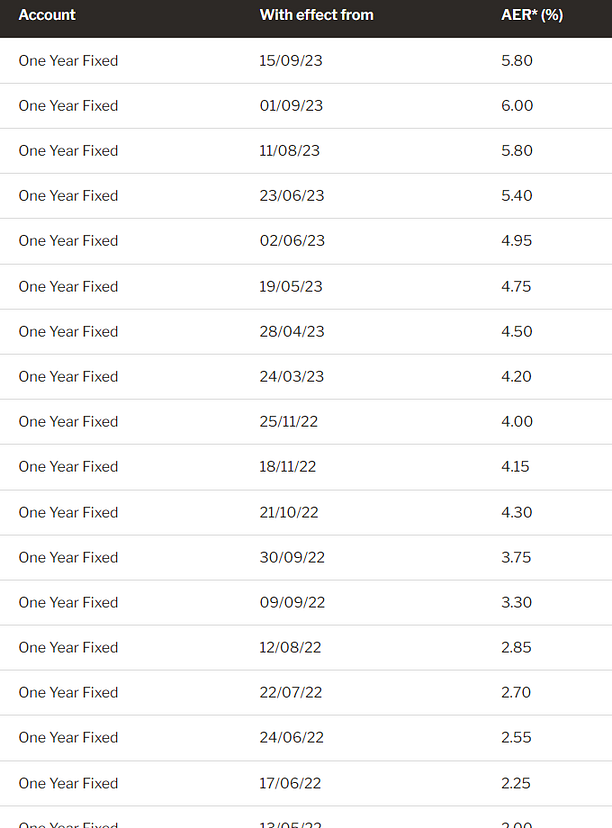

Now that we’re several months removed and still seeing significant outflows, I think what’s more likely and rational is because interest on savings accounts are reaching highs that we haven’t really seen since the 1980’s or 90's. Here’s just a sample from 1-year fixed rates from the last year:

As you can see above, the current trend has been going up steadily, breaking most recently in the 6% range. All of us in crypto know that banks have their own set of risks too, but it actually makes a lot of sense for those tied to the dollar to remove their uninsured crypto-dollar to a US-government backed (more specifically FDIC -backed) savings account that can give pretty decent returns. For this very reason, if you’re a TradFi institution, the smartest decision would be to not risk millions or billions of dollars in crypto to smart contract exploit that can drain your entire principal in seconds.

Do the math

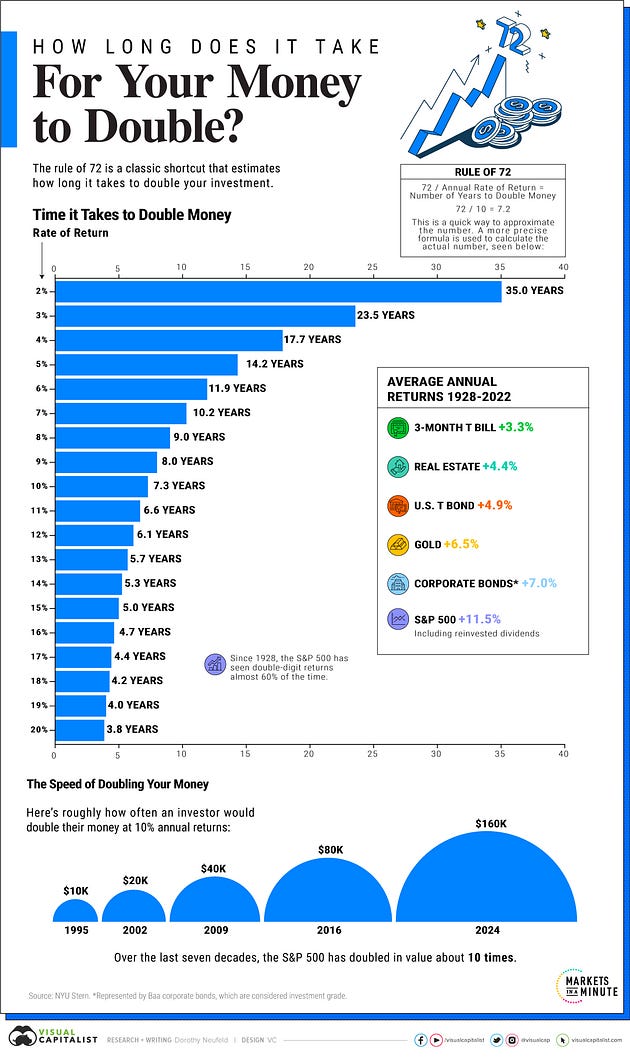

I’m not saying that crypto’s high yields shouldn’t be avoided, but the most prudent thing to do is to check the math for how much your risk is worth. A great graphic published by visualcapialist.com a couple of weeks ago shows how much you can expect to make over long periods of time depending on your interest rate:

Even at a “crazy high” interest rate of 20%, it would still take approximately 3.8 years to double your money, or in other words, you would have to trust that you won’t get hacked/phished/socially-engineered/exploited/rugged for 4 years to not only lose your interest + principal.

Thinking about the previous times where I was a victim to a scam or an exploit, the interest rates I was earning was barely breaking 15% APY. Over one year on a $1k investment, this would mean a profit of approximately $150 dollars. Conversely if I were to put $1k into a 6% FDIC-backed savings account I would earn $60. This means that the price of risk for me not to lose my crypto-principal for one year was $90 dollars. In other words, I was betting on the fact that over 12 months, that I was not going to get hacked/phished/socially-engineered/exploited/rugged for $90 dollars worth of profit.

Taking this one step further, if I wanted to double-down my investment to recover my lost $1k investment, according to the visualcapitalist graphic, at a 15% interest rate it would take me another 5 years to simply make up what I had lost.

Thinking you won’t get hacked/phished/socially-engineered/exploited/rugged?

It happened to Vitalik, it happened to Mark Cuban, it happened to so many of the most talented crypto OGs and devs — all people that I can bet pretty good money who are probably smarter than you (and smarter than me). Therefore I think it’s a bit foolish to think that we can’t fall victim to these ourselves. And for this very reason, to this very day I refuse to put any of my assets into a crypto IRA, no matter how good the tax implications might be. With how many exploits there have been over the past few years, it’s hard to stomach putting my crypto to any third party for more than 30 years.

Conclusion

Am I saying that people should stay away from crypto altogether? Emphatically no. I believe in the ethos of what decentralized money stands for and why it needs to be pursued. What I am saying though is that we’re never going to truly see the in-flows for the next bull market until there are more protections put in place for investors, just like what FDIC did for banks.

Like a moth to a flame, I will continue to write, research, and speculate on high yield projects, and also on projects that are trying break the barriers of what we thought weren’t possible (That and because I also have an indecent affinity towards gambling). But before aping into anything, I implore folks to make sure they don’t get blinded by high yield rates, flesh out your own good/bad takes, and to try to figure out beforehand what your risk appetite is for that next project that you might think will take you to the moon.

Thanks for taking the time to read this and be sure to follow me on twitter (https://twitter.com/CryptosWith) to get all my latest updates. Also, looking for a gift for your Crypto-loving/hating friend? Give them a REKT journal to cheer them up!

Disclaimer: And as a final reminder, this is not financial advice and this is for educational and entertainment purposes only. Please as always, do your own research and find what investments are best for you. Cheers everyone!