With all the volatility that we’ve seen from the latest CPI print, I’m suspecting that we might see even greater volatility shortly after the merge occurs, and that overall we’ll likely see a significant downturn over not just the entire crypto market, but stocks and equities as well. Call me a skeptic, but knowing that the market is always going from oversold to undersold, I think it’s just a matter of time that we see more significant market corrections. In addition the market has priced in the merge for the past month-or-so now, so once that’s over…well I think that’s a good enough reason to see another market correction soon.

Anticipating that prices may drop around 30%, I’m turning to Liquity to see if I can play the other side of the market, and to profit off of people’s liquidations. I’ve written about Liquity in the past, and I believe that it’s in potential market downfalls such as these where protocols like Liquity become especially lucrative.

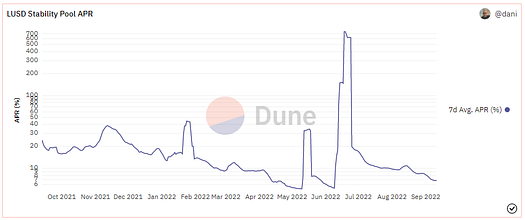

Earning 700%+ APR in the Last Market Crash

If you take a look at Liquity’s dune analytics page, you’ll see from their LUSD stability pool’s historical APRs, a huge spike around mid-to-late June:

What does this huge spike coincide with? Well if you don’t remember because you blacked out from the pain and anguish of this market crash, back in June the price of $ETH dropped to the $800 dollar range — prices we haven’t seen for $ETH since 2021:

Undoubtedly during this time people’s loans must have been getting liquidated left and right, yet at the same time $LUSD depositors were making returns in the range of 700% APR. Considering that this was a rolling 7-day average, I suspect that single-day returns were even higher.

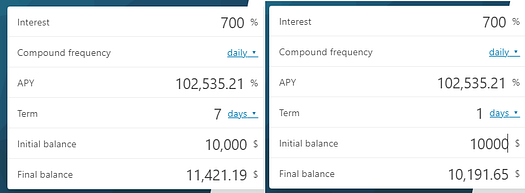

To put it into numbers, if you had $10,000 dollars worth of $LUSD deposited during this time, you could have made almost 20%, ROI in a single day, or more than 110% ROI over the course of a week:

Personally I’m expecting that even if there is a correction that we won’t see there be such a significant drop as we did back in June, but if the market does drop 30% or so, I imagine that there definitely will be liquidations in play and I plan to have some $LUSD ready to try to capitalize off of it.

Getting setup on Liquity

I’ve covered this in more general terms in a previous article, but essentially in order to participate in Liquity’s Stablepool you need to be in possession of $LUSD. $LUSD can be obtained in mainly two different ways, either on a DEX such as Uniswap or on Liquity itself by taking a loan. Weighing out the opportunity/sunk costs there are pros and cons either way, but if you have $ETH and would like to hold on to it (or if you’d like to try to avoid some tax complications) you could choose to put it up as collateral and take a loan out against it, borrowing $LUSD in the process.

Setting up a loan:

So this process might look different for whichever front end you use, (Liquity does not have it’s own frontend, but if you go to https://www.liquity.org/frontend you’ll see many to choose from), but I personally use liquity.app regardless if they have a 99% (opposed to 100%) kickback rate, mainly because by marketshare allocation, they are the most heavily utilized with more than 35% of Liquity’s Stablepool share. The Kickback rate is essentially the frontend’s fees, and you’ll see that the majority of them give either 99% or 100% back to the user.

Once you have selected your frontend, you must create a “liquity trove” and then deposit your $ETH, for which you will select your designated collateral ratio and receive your borrowed $LUSD, minus $200 dollars (this is the designated amount reserved to cover gas fees that goes to the liquidator in the case of your loan becoming liquidated). Liquity’s docs recommend that you keep your ratio at least above 150%, but the protocol has a minimum of 110%. In other words, if you fall below the 110% collateral ratio because your deposited $ETH drops significantly in value, then you are at risk for liquidation.

Important note: If you’re taking out a loan, be sure to keep track of whether or not Liquity is nearing entering “Recovery mode,” which according to the FAQ:

Recovery Mode kicks in when the Total Collateral Ratio (TCR) of the system falls below

150%. During Recovery Mode, Troves with a collateral ratio below 150% can be liquidated…The Total Collateral Ratio or TCR is the ratio of the Dollar value of the entire system collateral at the current ETH:USD price, to the entire system debt. In other words, it’s the sum of the collateral of all Troves expressed in USD, divided by the debt of all Troves expressed in LUSD.

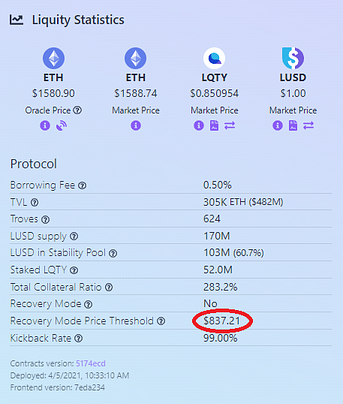

In other words, it’s probably not best to keep your collateral ratio around the 150% mark because if Liquity is stress-tested, then you could be subject to liquidation even if you’re above the 110% mark. To date, the liquidation rate is around the $800 dollar mark — this can also be found on the risky troves page:

A Couple Added Bonuses

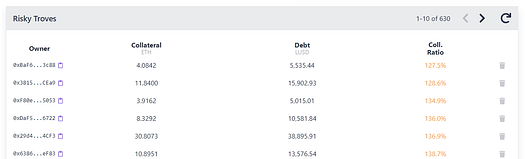

If you take a look at Liquity’s “Risky Troves” section, you’ll see all the current current outstanding loans sorted by ascending collateral ratio:

Once a loan falls below the 110% liquidation cutoff, if you are the lucky one that initiates the liquidation, you will be awarded a bonus of the loan holder’s $200 LUSD gas reserve deposit as well as 0.5% of the Trove’s collateral in $ETH.

Also, even if there’s not a huge wave of liquidations, you still will gain some decent rewards for staking your $LUSD in the stability pool. To date, the rolling 7-day average is around 6.87% APR which isn’t that bad:

However if you do decide to participate in LUSD’s stability pool, this leads me to explain some of the other factors to consider if you’re providing liquidity to the $LUSD Stability Pool…

Risks

First, this might not be consider an actual risk, but one has to remember that there is always an opportunity cost — if you’re putting a lot of liquidity into the $LUSD into the stability pool, this means you’re not putting [as much] liquidity somewhere else, namely funds that could be use on say a buy order waiting to cash in on a significant dip on the market.

Also, as I mentioned in my previous article there is a slight inconsistency with the peg of $LUSD to USD:

If you notice in the graph above, the peg has has styed relatively above the 1 LUSD:1 USD so if you buy into $LUSD, there is a possibility that when you cash in the peg climbs to $1.03 instead of $1.01, meaning that you could be potentially be losing 2 cents for every dollar’s worth of $LUSD that you put in. Vice versa, this could also be a benefit if you’re into playing the arbitrage game.

Conclusion

There are other profitable options for capitalizing off liquidations such as GMX.io, but as lucrative as GMX.io can be, the potential returns can’t compare to the upside that Liquity offers its depositors, especially if you’re expecting a pretty significant crash like me. And as long as the crypto-world has people wanting to take fee-free loans, there will continue to be people getting liquidated off of the market’s extreme volatility, and Liquity has truly created an ingenious system in which there are strong incentives for borrowers and the depositors to keep these incentives going.

Anyways, thanks for taking the time to read this and be sure to follow me on twitter (https://twitter.com/CryptosWith) to get all of those latest updates.

Disclaimer: And as a final reminder, this is not financial advice and this is for educational and entertainment purposes only. Please as always, do your own research and find what investments are best for you. Cheers everyone!