Bitcoin is the primeval blockchain prototype embodying the core concept that developed into a whole new paradigm in distributed systems design (pulling it from the relative obscurity of a fringe field in computer science to the forefront and focus of attention). It marks the first successful experiment in creating a peer-to-peer consensus network of circulating value by means of cryptographic proofs. It was more than a decade ago that Satoshi Nakamoto, the enigmatic architect of this modern day crypto-hawala published his white paper, “Bitcoin: A Peer-to-Peer Electronic Cash System”. The choice of the term itself already hints at something BitTorrent-like but for a kind of primitive techno-medieval coinage in the periphery of things. The first opening sentence in the abstract of the paper directly defines the problem Bitcoin is meant to provide a solution to: "A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution."

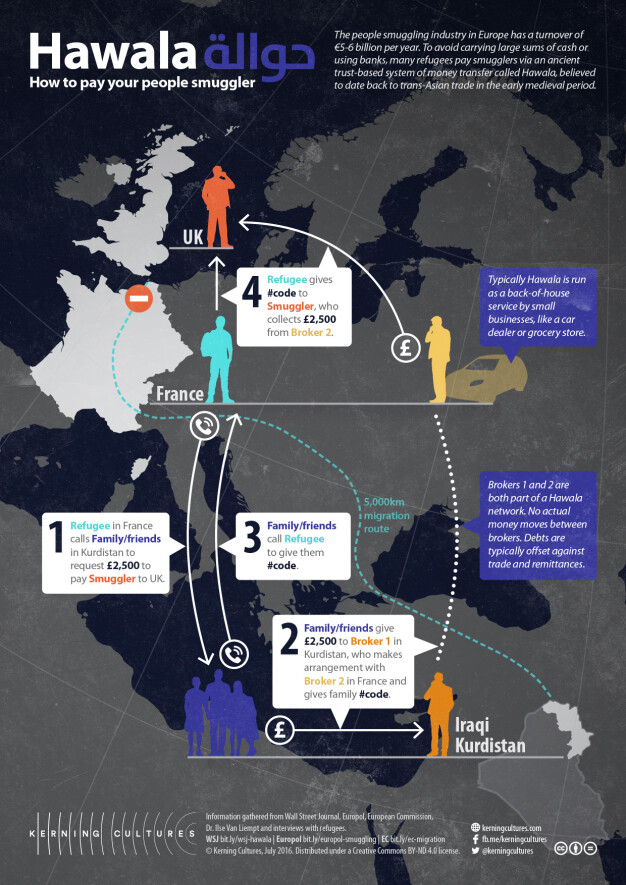

Hawala is an informal value transfer system operating parallel to traditional banking and financial channels and following Islamic traditions of honor. The hawala system (meaning transfer or trust in Arabic) has existed since the 8th century between Arabic and Muslim traders alongside the Silk Road and is based on the movement of cash through a huge network of money brokers changing hands.

The publication of the white paper and the subsequent launching of the network coincided with the immediate aftermath of the 2008 sub-prime mortgage crisis and at the same time fulfilled the need for a practical payment system for the flourishing online e-commerce. Both somewhat quaint and even bizarre in some of the assumptions contained and highly original and innovative at the same time, Bitcoin's technical assemblage initially attracted libertarian leaning technologist and cypherpunk types and various merchants of illegal goods (such as illegal drugs and stolen credit card information, with Silk Road being the first such "black market eBay" to launch in 2011). Bitcoin's entire history is marked by absurdity and controversy - which shouldn't come as a surprise when one considers how Bitcoin is also more generally an unregulated financial instrument, facilitating capital flows that slip through borders, legal jurisdictions and regulatory controls.

In October 2009 the first exchange rate of Bitcoin established its value at 1,309.03 BTC per 1 USD using a simple formula which includes the electricity expenses of running a node and generating bitcoins. And then July 2010 saw the launching of the MtGox Bitcoin exchange market by Jed McCaleb (which had previously functioned as Magic the Gathering fantasy game cards exchange), followed by a sudden ten-fold increase of the market value of Bitcoin within the span of just one week. And then the following month MtGox suffered a critical security breach compromising thousands of user accounts and their bitcoins. This would be the first in a long series of such failures, sunken exchanges and large amounts of stolen funds throughout the years.

An amusing explanation of Bitcoin.

More recent developments however indicate a gradual ongoing transition towards the domain of institutional finance and derivatives markets, hooking bitcoin to various financial instruments and adding additional market dimensions to it, while also in doing so making it subject to strict regulatory compliance on that side of its exposure and use. Perhaps most crucially, developments such as these tend to bring a range of natural, legitimate and reliable price discovery mechanisms which Bitcoin as it is severely lacks. Over the last few years significant forensic techniques and methodologies for analyzing the immutable records of the blockchain have been developed making it possible to deanonymize users and correlate specific patterns and events in many circumstances.

Design Rationale and Operational Logic

What Bitcoin provides a crucial solution to when it comes to digital cash is the so-called double-spend problem. Unlike with physical objects and cash, the nature of digital media is such that any data can be easily copied and replicated, corrupted or otherwise tampered with, presenting an inherent flaw in any digital cash schemes. The proposed solution is summed up so in the white paper:

"The network timestamps transactions by hashing them into an ongoing chain of hash-based proof-of-work, forming a record that cannot be changed without redoing the proof-of-work. The longest chain not only serves as proof of the sequence of events witnessed, but proof that it came from the largest pool of CPU power. As long as a majority of CPU power is controlled by nodes that are not cooperating to attack the network, they'll generate the longest chain and outpace attackers."

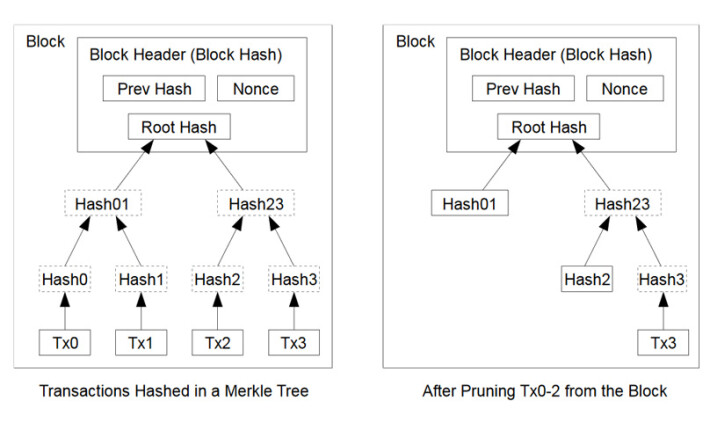

Essentially implementing an open ledger of crypto-accounting in a manner similar to how polygraphs operate, i.e. replicating the same output in multiple databases. A hash function is a useful cryptographic algorithm takes a variable size of data as an input and gives a fixed-length output. This is an extremely useful heuristic for checking data integrity. The Bitcoin protocol places transactions in Merkle tree arrangements - trees constructed by hashing paired data (the leaves), then pairing and hashing the results until a single hash remains, the merkle root. In Bitcoin, the leaves are almost always transactions from a single block and block headers must include a valid merkle root descended from all transactions in that block.

The polygraph, a device also known as a lie detector.

The continuous iterative hashing of basically everything in forming the growing chain of records is what prevents double-spends from taking place and provides the cryptographic proof that substitutes for the intermediation through trusted third-parties. To quote from the white paper:

"The only way to confirm the absence of a transaction is to be aware of all transactions. [...] To accomplish this without a trusted party, transactions must be publicly announced, and we need a system for participants to agree on a single history of the order in which they were received. The payee needs proof that at the time of each transaction, the majority of nodes agreed it was the first received."

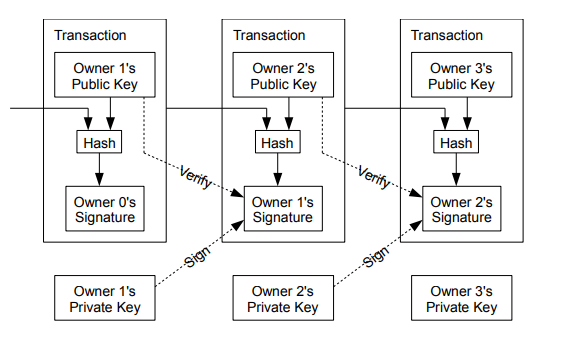

A coin is defined as a chain of digital signatures of ownership. An owner transfers a coin by digitally signing a hash of the previous transaction and the public key of the receiver as the next owner and adding these at the tail end of the coin. A payee can thus verify the signatures to verify the chain of ownership. This sometimes affects the fungibility of coins as they carry their entire history of exchange and trajectory of how they ended up in the possession of their current owner - and if traceable to some stolen funds associated with some hacked exchange or acts of ransom, etc. these coins may get blacklisted or have their owner incriminated. This has led to the sale of newly generated coins with no associated history at higher premium prices.

How bitcoin transactions are constructed. The process involves a series of cryptographic operations (hashing, signing, comparing/verifying) and the Bitcoin ledger keeps track of what are known as UTXOs, or Unspent Transaction Outputs. UTXOs are the main objects Bitcoin deals with and can be spent as an input in a new transaction. In order for value to be combined and/or split, transactions may have multiple inputs and outputs. Usually there's either one larger previous transaction input or multiple inputs combining smaller amounts, and at most two outputs - one for the payment to be carried out and one returning any remaining change back to the sender.

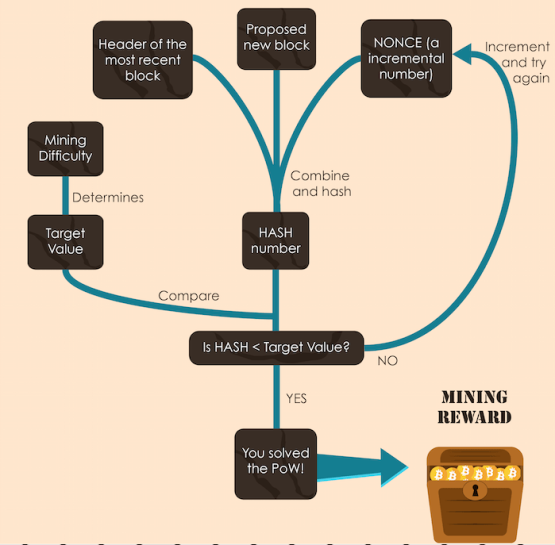

For the implementation of a distributed timestamp mechanism in a peer-to-peer setting Bitcoin uses a proof-of-work scheme similar in principle to the one used in Adam Back's Hashcash design. It involves scanning for a value such that when hashed, the resulted hash begins with a certain number of zeros. Blocks get chained together in a sequence by each block containing also the hash of the previously appended block preceding it. A valid block must hash to a value less than the current target, indicating the work that has been done generating it. Difficulty adapts so as to regulate the rate of block generation, keeping it at 10 minutes block time. Initially, proof-of-work could be performed by regular home computers and CPUs, but as the chain grows and network traffic increases mining has switched to GPUs and GPU rigs and eventually after that to specialized ASICs customized for more efficiently performing proof-of-work at much increased hashes per second.

Blocks are structured around Merkle trees structures which store the transactions. However, once a transaction is buried under enough blocks the spent transactions preceding it can be discarded in order to save disk space. Since only the root hash is included in the block header, old blocks can be compressed by pruning off some of the tree branches.

This proof-of-work (PoW) schema also solves the problem of representation in majority decision-making. Instead of based on spoofable and Sybil prone IP addresses (i.e., 1 IP = 1 vote), PoW is basically an one-CPU-one-vote arrangement with the majority decision represented by the longest chain with the most work invested in it. By convention, the first transaction in any block is a special transaction (called a coinbase transaction) creating a new coin which is awarded to the block creator. This both adds incentive for node operators to continually support the network and means for initially distributing coins into circulation. Additionally, fees are attached to every transaction and also get collected by the miner who ends up generating the winning block. Once all coins have entered into circulation the incentive can move to transaction fees only.

The networks operates in the following sequence of steps:

- New transactions are broadcast network wide

- Each node collects a subset of transactions to fit into a block and begins working on finding a valid PoW for that block

- When finding the PoW, it broadcasts the block to all nodes in the network

- Nodes accept the block if all the contained transactions are valid according to the rules of the protocol (i.e., not already spent)

- Block is confirmed and accepted with finality as nodes begin working on the next block, including in it the hash of the newly appended block

The PoW, together with the block selection lottery, scarcity of fixed total supply and incentive structure for rewarding miners for securing the network constitute what has come to be known as Nakamoto consensus. A collective socio-technical assemblage which was the first successful experiment at getting value to freely circulate within the domain of the Internet without relying on any other intermediating financial institution, payment processor or a trusted third party service provider. As the prototype and basis for further experimentation in distributed peer-to-peer network designs coordinating around a shared ledger, Bitcoin is fairly primitive and simple and in many ways far from ideal or even optimal long-term solution to many of the problems arising with the digital expression of transactable value.

The Bitcoin PoW mining process.

The transparent nature of Bitcoin's public ledger, for example, exposes the recorded history of all transactions, balances and corresponding addresses to the general public. However, the public keys which constitute the addresses are not in themselves directly associated with any one particular identity, so there's no information linking transactions to particular persons. This is known as pseudonymity. For an additional layer of privacy, new key pairs could be used for each transaction so as to prevent leaving audit trails of linkable common ownership.

Additionally, the rigid and high constrained design and regime of operation of Bitcoin prevent it from being useful in articulating more complex expressions of business logic or conditional transactions. Like some old Soviet era piece of machinery, it is slow, cumbersome, wasteful and not always too convenient, but nonetheless ultimately reliable in the one simple thing it is intended to do.

Is Bitcoin Money/Currency or a Separate Asset Class? A Medium-of-Exchange or a Store-of-Value? A Digital Commodity or a Clandestine Conduit for Unregulated Money Flows?

It seems appropriate to cite Martin Armstrong here, a well-known economic forecaster and institutional consultant who's an expert in monetary history. In a blog post entitled "Have Cryptocurrencies Become a Religion?" Armstrong explains:

"Socrates called the high in Bitcoin simply because it complied with the trading patterns like everything else that is really not the asset, but how humans interact with that asset (Behavioural Economics). Its value is based upon ANTICIPATION and that need not be real, possible, and it may be outright impossible. If you believe in something you react according to your beliefs even if it is completely irrational."

"Cryptocurrencies are trading vehicles. Cryptocurrencies will NEVER replace the dollar or world currencies. Do you really think governments will simply allow such a venture to take all their power away without a fight? Cryptocurrencies are worthless without a power grid. That is a disadvantage even to mackerel. That said, it does not stop Bitcoin from being a trading asset, but it is not money. It trades on a belief system of some that are completely irrational of which you will NEVER convince the majority to agree with them any more than they could with gold."

"I do not care what you call money. It is nothing more than a unit of account and a medium of exchange. It historically sits on the opposite side of assets. Bitcoin is still an asset – it is NOT money. If Bitcoin were money, then it would decline in purchasing power when assets rise."

And it is also true that trading Bitcoin, a decentralized digital asset, on centralized exchanges overlaid with traditional databases and keeping custody of funds largely defeats the intended purpose of Bitcoin and introduces a range of vulnerabilities which make it susceptible to strategic capture and appropriation. In another post, "So Long as Cryptocurrencies Remain Assets They Will Survive a Monetary Crisis", Armstrong writes:

"Tangible assets are on the opposite side of whatever the currency is in use. When the stock market rises, the purchasing power of the currency declines. When the stock market crashes, then the purchasing power of the currency rises. They are on OPPOSITE sides. Do you really want a cryptocurrency to be a currency or asset? Most people pitching them are really explaining an alternative asset – not a currency."

Given how computationally and energy intensive bitcoin transactions are and the fluctuating fees depending on network activity and congestion (a blockchain, being a single serialized lane of blocks and blocks, the containers of transactions, being capped by space and time, presents a natural bottleneck which limits throughput capacity of transactions that can be validated), it makes it impractical as everyday currency. It has however often shown significant correlations with the market price of gold. As capital tends to flow where safe and provided some assurances and guarantees, it makes sense that bitcoin would somewhat behave like gold since the latter is known to exhibit inverse correlation with the US dollar (i.e., whenever confidence in the dollar drops, capital flows into gold as safe haven).

"There are a lot of problems with the technology and it would clearly make the entire economy vulnerable to a crisis in the failure of platforms or the power grid. Goldman Sachs sees the opportunity because of all the fraud. They are looking at stepping in as a CUSTODIAN because the integrity of the security behind a cryptocurrency is often questionable.

In war, you target the electricity grid as a first objective and then the total economy would collapse as well as the effort to fund a war."

One popular Bitcoin narratives makes the claim that bitcoin could and most likely would end up becoming the new world reserve currency. A ridiculous proposition no doubt, if one simply begins by inquiring what should the desired properties of a world reserve currency be and what are the inherent properties of Bitcoin. Armstrong explains:

"We have people in Bitcoin swearing it is going to $100,000 and become the new reserve currency. That is such a joke for any currency to be worth that much would guarantee it cannot be used in commerce since most transactions are small. Then to be the reserve currency means governments would have to issue debt in Bitcoin. Come on! Are these claims even practical?"

He also makes a point of another very important and often under appreciated or altogether disregarded aspect of Bitcoin:

"Bitcoin became the LEADING means of money laundering and movement of cash out of China, circumventing their rule of law and currency controls. So do not think for one minute that Bitcoin rose because it was really a wonderful idea?"

Given the extensive track record of hacked exchanges and stolen bitcoins under dubious circumstances and without much conclusive explanation since Mt.Gox, coupled with the lack of much or any regulation at all and Bitcoin's status as a more or less rogue money vehicle, it becomes obvious how Bitcoin would prove the ideal means for carrying out money laundering operations or as a financial back alley for cross-border cash logistics under the radar. And it's also not entirely clear what the real motives of Bitcoin's creator had been given we don't know his identity - but it is not beyond reasonable doubt that he may have had certain hidden and ulterior motives. The likelihood of him actually being the criminal mastermind by the name of Paul Le Roux has even been speculated recently. And all things considered, it is an actually plausible scenario.

As for the (seasonally changing) narratives that define community discourse, the "digital gold" and store-of-value (SoV) perception of Bitcoin seems to have persisted the most. Since impractical as an everyday medium-of-exchange (MoE) and given its security guarantees and properties, as well as various factors which come into play in influencing its market price formation (e.g., expanded energy validating transactions and generating of new coins into circulation with each appended block), Bitcoin seems to have rather placed itself as a Schelling fence of sorts - as also testified by its firmly conservative attitudes which refuse to make any changes to the protocol. That is to say, the purpose of Bitcoin may in some important ways be precisely to cement itself as an always available familiar terrain and an always accessible, reliable mechanism for whatever purposes it may come useful.

Regulated Futures and Institutional Lending Market for Bitcoin

Bitwise Asset Management published an important piece research and analysis earlier in May, "Economic and Non-Economic Trading In Bitcoin: Exploring the Real Spot Market For The World’s First Digital Commodity." In it they point out how the efficiency of the bitcoin market has dramatically improved since December 2017 and that the bitcoin market of today bears little resemblance with the unregulated, grassroots history of the past. The U.S. market for regulated bitcoin futures was launched in December 2017, when both the Chicago Board Options Exchange (Cboe) and the Chicago Mercantile Exchange (CME) launched cash-settled bitcoin futures contracts. Since then, volume for these derivative contracts has grown considerably, with the majority of it linked to CME’s contract.

The series of developments since December 2017, the authors argue, have transformed the bitcoin market having had an overall equalibralizing effect. Bitcoin's all-time high happened to coincide to the day with the launch of the CME futures contract which directly contributed to the bear market of 2018 (the price of Bitcoin dropped by $2000 in a single day shortly after the launch), as the derivative introduced a financial lever making it possible to bet on the decline in bitcoin price and gave arbitrageurs the tool they needed to properly engage in arbitrage. The introduction of such market mechanisms contribute to market efficiency and tend to exert a stabilizing effect on curbing volatility.

Both the Cboe and CME contracts are monthly, cash-settled contracts, though using different methodologies for determining cash settlement price:

- Cboe: Draws prices from the 4pm Gemini exchange auction on the settlement day.

- CME: Uses a volume-weighted median pricing methodology drawing prices from Bitstamp, Coinbase Pro, itBit, and Kraken, from 3:00pm - 4:00pm on the settlement day.

More recently earlier in September the Intercontinental Exchange (ICE) launched its long-awaited Bitcoin futures trading platform, bringing Bakkt's daily and monthly Bitcoin futures contracts to the market. Bakkt together with ICE are working to bring federally regulated price discovery to bitcoin markets and provide institutional grade standards and services for institutional market participants to enter into the actor-networks of Bitcoin and crypto. These entry points of exposure of bitcoin to the domain of traditional finance bridges a long standing gap between the two worlds and brings some much needed clarity to the muddy waters of unregulated crypto markets and shady rogue exchanges that routinely fake volume and engage in wash trading (among many other forms of otherwise commonly illegal market manipulation).

The set of financial services around Bitcoin was further expanded in February 2018 when Genesis Capital rolled out the first institutional short lending market for bitcoin, followed by the entry of a large number of established, institutional, and algorithmic market makers into the space throughout the year (among which Jane Street, Susquehanna International Group and FlowTraders). All these developments appear to signal Bitcoin's likely transition from its anarchic grassroots cypherpunk past towards a more market efficient institutional future and level of maturity.

Entities and Organizations Dedicated to the Advancement and Development of Bitcoin

Blockstream is a blockchain technology company led by co-founder Adam Back and founded by Gregory Maxwell, Pieter Wuille and others. Blockstream employs a large number of prominent Bitcoin Core developers and is dedicated to developing Bitcoin side chains and other second layer scalability solutions. In October 2018 Blockstream launched its first production ready implementation of a (pegged) Bitcoin sidechain called Liquid Network. Liquid Network is meant to facilitate near instant bitcoin transactions, reducing delays and friction and loading off some of the main chain traffic onto the sidechain. It is described as an "inter-exchange settlement network linking together cryptocurrency exchanges and institutions around the world, enabling faster Bitcoin transactions and the issuance of digital assets."

Blockstream is also involved with the development of Lightning Network, another second layer approach to scalability involving an extended network of bidirectional off-chain payment channels (where only the opening and the closing of a channel is broadcasted to the blockchain). The Blockstream Satellite network was also launched in 2018, including five satellites across six coverage zones broadcasting the Bitcoin blockchain 24/7 for free, reducing the dependency on internet access and protecting against network interruptions. As of 2019 the network is still one-way (from node to user), but it is possible to send transactions via SMS.

Controversies, Backstage Intrigues and Unintended Consequences

Besides its popular use as means of transacting in the murkier corners of the darknet, in paying or getting paid for various illegal services and goods (both digital and physical), Bitcoin has also ended up positioning itself as the denominator of the entire crypto-assets market, having all other tokens and coins more or less synchronize with it. Already a potential systemic risk and central point of failure as such, but not yet quite the entire story. Bitcoin's meteoric rise in 2017, going from 1 to nearly 20 thousand USD in the span of a few months had obviously not been the result of any kind of organic process and has raised some inconvenient (for some) questions.

Market manipulation is commonplace in crypto, but the deliberate arrangement of bubble triggering circumstances and the releasing of untrustworthy and unverifiable fiat-fixed crypto-derivatives in circulation ranks as a much more serious a risk, one potentially setting off chain reactions of rapidly spreading systemic consequences, than say the regular wash trading taking place or the yet another trivial instance of a Telegram coordinated pump and dump operation.

This issue is covered in more detail in a separate post, "What is Tether USD (USDT)? The Stablecoin Fiasco".

Among other unintended consequences of Bitcoin's coming to the forefront of attention was also the spread of ransomware, with the 2017 WannaCry outbreak one of the most disruptive such attacks on a global scale.

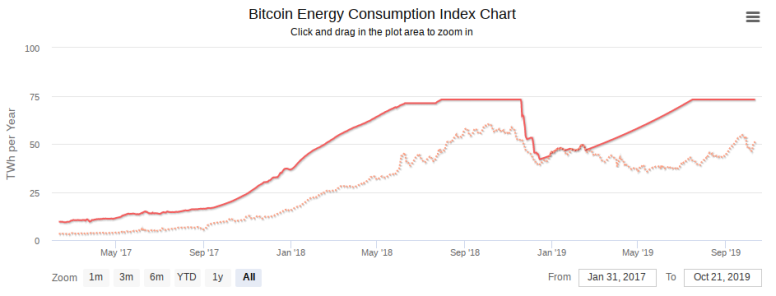

Bitcoin energy consumption chart (from May 2017 to October 2019). Source: Digiconomist.

Bitcoin's global power consumption and its tendency towards exponentially increasing in orders of magnitude is another worrisome trend which raises some alarms. As the network's overall computational power increases, the protocol accordingly adjusts difficulty to maintain operational parameters such as block times constant. Presently the Bitcoin network consumes as much energy as entire developed countries like Ireland or the Netherlands. And mining operations tend to cluster around rural areas where there's access to underutilized hydroelectric power. Together with the introduction of custom ASIC miners, all these factors have together contributed to a centralizing trajectory which puts the system at risk of capture.

Alternatives, Competitor Projects and Hard Forks

Just Bitcoin itself has spawned a number of hard forks as the inevitable consequence of how governance tends to be practiced in Bitcoin Core, leading to discontented community members to splinter off in different factions, fragmenting the network into diverging hard forks. Bitcoin Cash being the most significant contender claiming to represent "the real Bitcoin". Other projects have gone to fork the Bitcoin codebase and launch some slightly modified spinoff of the core protocol (as, for example, Litecoin, which is nearly identical to Bitcoin except for using different hashing algorithm and having decreased block generation times) while others have tried to improve upon the core concept, switching from an UTXO to an account-based ledger (tracking accounts and balances rather than unspent coins) so as to extend functionality with a simple stack-based virtual machine for executing code deployed on-chain.

Yet others have completely done away with the blockchain model substituting it instead with a directed acyclic graph (DAG) for mapping value flows and individual user hashchains for personal bookkeeping. Regardless, Bitcoin seems to have successfully established itself as a de facto standard in the space, maintaining until recently a firm monopoly over the market as the denominating unit pricing all other tokens, coins and assets.

Bitcoin Cash (BCH): The decisive schism and an ongoing rivalry

Bitcoin Cash (BCH or "Bcash") was the first major schism in the Bitcoin community which led to a hard fork taking place on August 2017. The main reason for the rift was to do with the ongoing block size debates where BCash members supported increasing the block size to meet demand while Core members were proponents of second layer scalability solutions. BCash remains the most successful hard fork of the original crypto-ledger and currency and it ranks fifth by market cap (a slightly misleading metric in crypto). It has the support of prominent community figures, industry leaders and well-known domain experts such as Roger Ver (its main proponent), Emin Gün Sirer and others.

BCash also reflects the difference between two Bitcoin narratives - Bitcoin as store-of-value and Bitcoin as medium-of-exchange. A block size increase is necessary in order to avoid the workflow bottlenecks that inevitably form with increased adoption of Bitcoin as a practical everyday medium of exchange. Bitcoin Cash supporters consider it to be the legitimate continuation of the Bitcoin project as peer-to-peer digital cash beyond the reach of state control and seizure.

A roadmap of the planned milestones in BCash's development is available here.

Ethereum Classic (ETC): Ethereum with a Bitcoin attitude

Ethereum Classic is the original Ethereum chain which represents that part of the Ethereum community which is guided by more conservative principles and alert precaution. After the infamous DAO hack, the Ethereum Classic community decided it will not take part in the setting of what they saw as a dangerous precedent of violating the immutability principle in reversing transactions and reorganizing the chain. The Ethereum project itself had been originally born from frustration with trying to build solutions on top of the Bitcoin protocol. It puts together a more general-purpose implementation of the blockchain-based transactional engine, one equipped with a simple run-time environment (the Ethereum Virtual Machine, a stack-based machine) for executing programmable business logic and immutable scripts from the ledger (known as smart contracts).

Philosophically ETC is closer to Bitcoin than it is to Ethereum's "world computer" concept and experimental approach of "moving fast and breaking things". And also like Bitcoin and unlike Ethereum, it sticks to the Proof-of-Work consensus schema (while Ethereum works towards transitioning to Proof-of-Stake).

Nano: Ultra-fast zero fee micro-transactions

Nano (formerly Raiblocks) is a fast, feeless and scalable DAG-based implementation of a 'pure' currency. It is built to be practical for common everyday use (i.e., a buy-coffee-with type of crypto-currency) and micro-transactions. There's no intensive proof-of-work mining process in Nano and its supply has been fixed in the first genesis transaction. It was initially distributed via a faucet and gained a lot of popularity in Venezuela and other such economically hampered countries at the time.

Cardano (ADA): Third-generation blockchain grounded in Bitcoin's foundational principles

Cardano is a third-generation blockchain which takes some of the basic underlying principles of Bitcoin and expands on them in efforts to create a highly secure and functional financial infrastructure capable of supporting mission critical applications and reliably securing trillions of dollars in value. Cardano was founded by Ethereum co-founder Charles Hoskinson and is developed under the umbrella of IOHK which also houses Ethereum Classic. Cardano likewise takes the slow and diligent approach, building on peer-reviewed protocols and specifications and extensively making use of formal methods and functional programming (i.e., Haskell-derived).

Cardano's settlement base layer of accounting (of its native currency, ADA) extends the Bitcoin UTxO model with functional scripts operating on the dataflow of transaction outputs in an effort to bring it on par with Ethereum’s expressive account-based scripting model. What especially sets Cardano apart is its use of formal verifications to provide mathematical proofs of correctness (of whether a piece of code does precisely what it has been intended to) and its building on Haskell, the programming language most representative of the functional programming paradigm (often considered to be somewhat closer to mathematics than programming as commonly thought of and increasingly making its way into the domain of finance).

Summary and Conclusion. Things to Keep in Mind and Take Into Consideration.

Given all the entangled complexities and interwoven interests surrounding Bitcoin, it's perhaps beyond our capacities to make any meaningful forecasts with much certainty or confidence. The cryptosphere is still a nascent and highly experimental field, subject to frequent destabilizing phrases of sharp volatility swings on markets suffering from numerous structural flaws and ill formed relationships and arrangements. Bitcoin is perhaps above all an ad hoc instrument that should be understood in terms of what it does and how it might be useful in certain circumstances such as those that called it into existence. As such, its market price may be a somewhat more arbitrary affair than we may think. Not least of all and somewhat contrary to common sense intuition, price does not necessarily reflect value, especially in markets as punctured with inefficiencies as those.

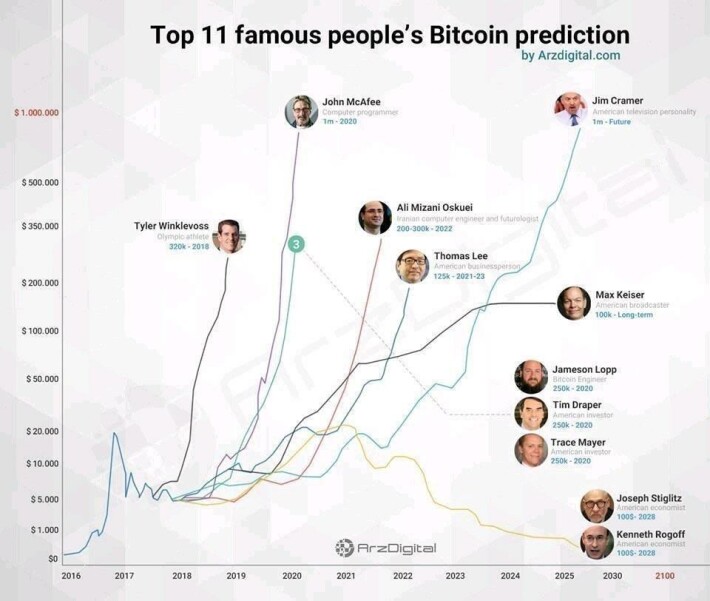

Some famous Bitcoin price predictions. Announced predictions from perceived authorities can sometimes disguise manipulative intentions or may be aimed to trigger a self-fulfilling prophecy effect followed by a Keynesian beauty contest chain reaction (where one bets on the lowest common denominator of how the crowd majority would react regardless of how preposterous the claims or whether or not there's anything of actual value behind a project or an asset). John McAfee is among those celebrity individuals that openly take full advantage of these facts. And TRON, an example of obvious vaporware solely running on marketing campaigns and ploys.

Furthermore, there is no single unified price of Bitcoin consolidated across all markets, exchanges and geographies. Bitwise Asset Management, a crypto index fund, have recently shown that roughly 95% of all reported daily bitcoin volume is either fake or wash trading. They identify eight exchanges which have real volume: Binance, bitFlyer, Bitstamp, Bittrex, Coinbase Pro, Gemini, itBit, and Kraken. The paper also points out that the data aggregated by CMC is highly misleading and not reflective of the reality of what actually takes place. Openmarketcap launched as a response, tracking only real volume and providing more accurate view of the market dynamics (Messari is another such similar service considered to be reliable).

Additionally, it must be kept in mind that the market cap metric can be rather misleading in the context of digital crypto assets since it derives from the last known price an asset had been bought for multiplied by the supply of tokens in circulation. This, especially given insufficient or sometimes even nonexistent liquidity on stagnant markets makes the market cap estimate easily manipulable and more or less meaningless. Bitwise's paper nonetheless points out that the actual efficient bitcoin market "bears little resemblance to the market that is represented in public data" and is "unfortunately, is obscured from public view by the foggy miasma of fake volume and bad data that clouds the bitcoin ecosystem."

In any case, Bitcoin's pivotal role has been in demonstrating the possibilities of assembling ad hoc peer-to-peer distributed networks on the basis of a common protocol and coordinated around a shared database of recorded events. A concept whose potential we've barely started tapping into and articulating viable solutions to long standing problems around the basis of which. And we mustn't forget the central importance of decentralization as resistance to capture, seizure and control as well as a highly robust and resilient mechanism against central points of systemic failure (something especially critically important in our present day and age of highly interconnected complex systems of non-linear correlations and dynamic socio-technical assemblages of ever accelerating speed). Neither should we disregard the dangers of appropriation of the technology for malevolent and malicious purposes (since technology as such is value-agnostic and depending on the intentions of its operator) or its potential for being weaponized in various circumstances.

-- @rhyzom (Martin B.)