People often wonder why the rich stay rich and the poor… well, poor! There’s a complexity of answers here. But one HUGE difference that has always stuck out to me is their habits with money. This is an area of detail that cannot be ignored.

Many will assume (and not without merit) that I’m about to say that the poor are bad with money. The thing is, people aren’t born good or bad with money! They develop habits over their lifetime that alter this course. It is a learned behavior.

There are stories of shoe cleaners and mailmen that at their death end up donating a sum in the millions (see The Millionaire Next Door by Thomas J. Stanley and William D. Danko, for example). Their friends and family often have no idea of their wealth. There are secret millionaires out there living among the lower class. These people weren’t born any better than the others. But somewhere along the way, they found the desire and the ability to learn more about money.

It’s common knowledge that wealth inequality is at its greatest point in the US. The 1% has grown exponentially, while the other percent is still… where it’s at. The entire US has been through a roughly 12 year bull market. But only some capitalized. Phrased differently, only some have known enough to capitalize.

As the economy stumbles a bit, that will only get worse! We know the best time to invest is when the economy is at its worst. Business is struggling. Investment (properties, the stock market) is at a discount. This discount comes with increased risk, during a time when things are inherently risky. But those that take the risk, often reap the benefit. The lower and middle class rarely take this risk.

The lower and middle class, if they do invest, often do so at a time when things are booming. And often ONLY then. So they miss out on this period of high risk but high reward. And we’ve all heard about the guy who invested at the market peak, and then lost thousands when the winds changed. This type of person often never invests again.

Why don’t we often invest at this time? Because we don’t have the capital. We don’t have the deep pockets held by the rich, to be bold when others are fearful. Capital on hand is often the biggest separator. A study in 2015 by the Pew Charitable Trust estimated that an average of 80% of Americans are in debt.

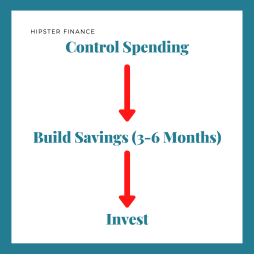

The only solution is fundamental change in behavior. How do you secure more capital in tough times when others are scrambling, losing jobs, and wondering where their next paycheck will come from? By tightening your belt in the best of times and the worst. By learning to control your budget.

Spending control and investment are linked. Most don’t realize this. But you can only feel confident about investing, if you feel confident about your savings. So if you’re curious about engaging in some of the tactics in this newsletter, ensure you have your capital properly set up.

Go about the task of building out a budget plan for yourself while you’re doing well! Don’t decide only to make this change when times get hard. It will be too late. And you’ll miss the upsides of investment. Focus on spending control now and this will result in you having extra. That extra is the difference maker when the economy isn’t doing well. It will enable you to take the leap, when others stay at home.

What do the rich have that we lack when it comes to investing? Confidence! Confidence comes from the feeling of security. And your savings can help provide that.

Investing is the glamorous side to wealth building. Spending control is the unglamorous. Investing is the player winning a tennis match on live TV in front of millions of people. Spending control is the hundreds of hours before that match that enabled the player to win. Find the way to controlling your spending, and you’ll find yourself with a surplus to invest.

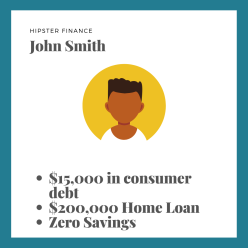

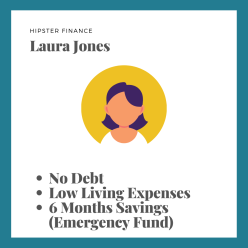

To close, I want to demonstrate this with a case study of two people. You may very well be in the same place as one of these two. And it will give you insight into why spending control is so important.

In the two examples above, it should be clear which person is ready to invest at the next opportunity. John will be stuck trying to pay off debt, and build up his savings in a bad economy. He will never find the solid footing to invest. Laura, on the other hand, is ready to invest now, and ready to continue to invest through an economic downturn. This can be the difference between Laura changing the wealth trajectory of her family, and John not.

Start thinking about your time and money as opportunities to build future capital for investment. Every dollar that leaves your hand in pure consumption is a dollar that could have gone to work for you. Increase your savings, and you will be able to confidently increase your investing.

Remember, these two concepts are completely joined. You save the income you have earned, and you use surplus from your savings to invest. Those investments will propel you on your path to wealth.