Legacy credit card markets are mathematically engineered to suppress retail yield. Banks extract massive interchange fees at the point of sale, keeping the lion's share and starving consumers with arbitrary "reward points" that hold zero liquid value.

This article breaks down how Jupiter Global, running on the Solana chain and integrated with Rain’s Visa network, bypasses this bottleneck to deliver a sustainable 4% baseline cashback. However, the current launch promotion – which includes a significant early-bird liquidity incentive – has a strict expiration date of June 30th. Residents in the United States and the APAC region have a narrow window to execute their deployment and secure this yield.

Jupiter Visa Platinum virtual card.

1. The Infrastructure: The Jupiter Mobile One-Stop Shop

To access the card, users must first download the Jupiter Mobile App directly from either the Google Play Store or the Apple App Store. The application acts as a dual-engine financial hub:

The Web3 Native Engine (100% Self-Custodial)

Upon installation, the app automatically generates a standard, Solana-based crypto wallet. You retain full control of your private keys. From this interface, you can seamlessly receive, send, and trade tokens across the ecosystem.

The Jupiter USDC Spend Engine (Custodial)

Crucial Funding Detail: The Jupiter Spend account operates strictly on the Solana network. To use the card, you must fund the Spend account by sending USDC on Solana directly to its generated on-chain address. Sending other stablecoins or routing USDC via Ethereum or other Layer 2s will not work and may result in asset loss. Once funded, the virtual Visa Platinum card activates instantly for Google Pay or Apple Pay.

Tap the image to watch the official Jupiter Global video on X / Twitter.

2. The Uncapped Velocity Advantage

By utilizing Rain, a Banking-as-a-Service infrastructure provider and Visa Principal Member, Jupiter issues a true Visa Platinum Bank Identification Number (BIN) tied to this spend account. This provides two massive structural advantages over standard crypto cards:

Uncapped Velocity

Because the card settles directly against your on-chain USDC wallet, there are no artificial daily or annual spending limits. It enables limitless capital deployment without legacy banks restricting your transaction flow.

High-Trust Routing

Standard crypto debit cards are frequently blocked by hotels and car rental agencies due to their low-tier prepaid classification. The Jupiter card registers at the terminal as a high-trust Visa Platinum BIN, allowing merchants to seamlessly process large pre-authorization security holds without auto-declining the transaction.

3. The Global Yield Equation: instant USDC

A sustainable, high-yield system requires sacrifice. Visa Platinum traditionally carries expensive insurance riders, such as rental vehicle coverage, extended warranties, purchase protection, and DragonPass lounge access. Issuers pay massive premiums to network partners to maintain these.

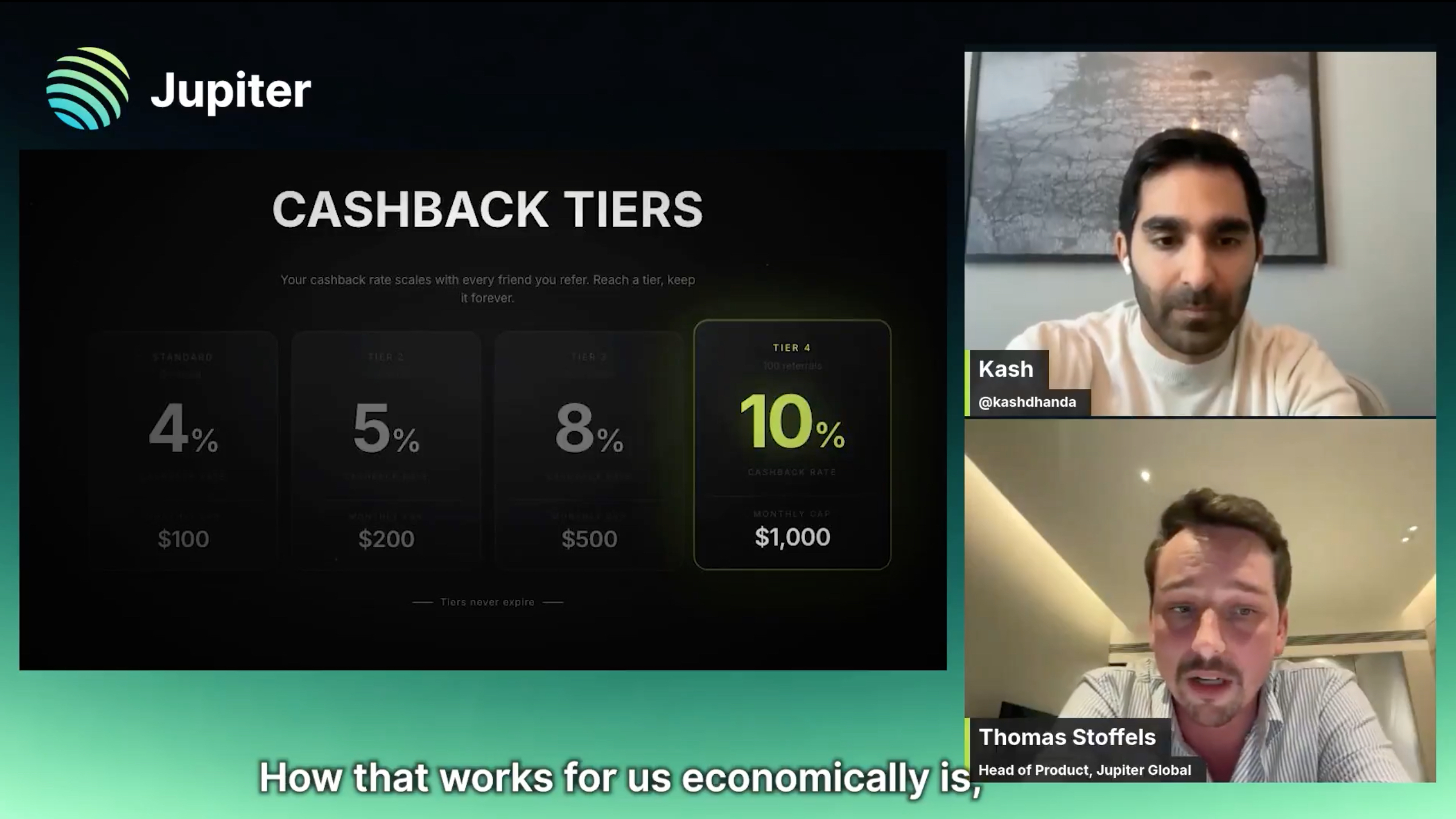

Jupiter made a strategic trade-off: they completely stripped away the traditional TradFi insurance and travel fluff. By eliminating these overhead costs, Jupiter redirects the entire premium budget into funding a massive 4% base cashback floor (which scales up to 10% via referrals).

Crucially, cashback is credited in USDC the exact moment a transaction settles. It lands instantly in your spend balance, ready to be deployed immediately for further purchases or sent back out to your self-custodial wallet. For active daily spenders, capturing raw, instant stablecoin yield is vastly mathematically superior to an extended warranty or a lounge pass utilized once a year.

Tap the image above to watch the 1-minute breakdown of the cashback tiers on X / Twitter.

Because the card operates globally, the net profitability varies depending on the FX penalty applied by the network when converting USDC to local fiat at the point of sale. The geographic arbitrage breaks down as follows:

- The US Baseline: 0% FX fee. Users capture the full, unadulterated 4% yield on all daily USDC spending.

- Global / APAC: 1.8% FX fee. Even at the highest penalty tier, users in Latin America and Asia net a minimum 2.2% pure profit, a rate virtually impossible to find in local TradFi markets outside the United States.

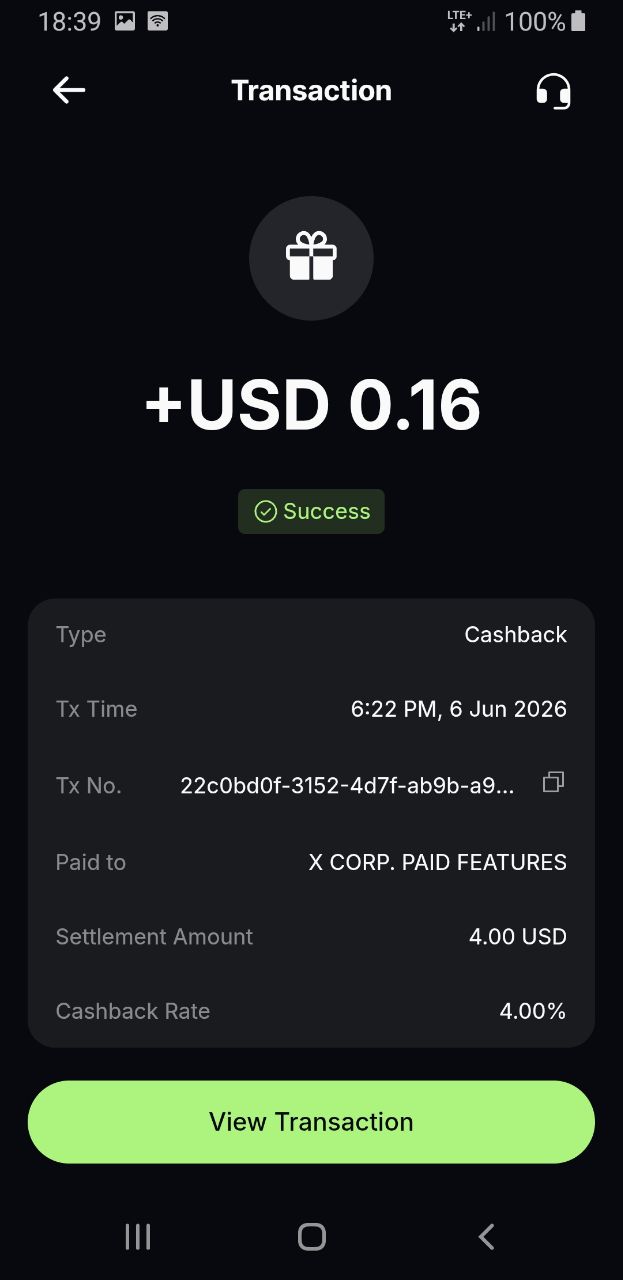

Live transaction settling on-chain: A USD-denominated subscription bypassing European FX fees to capture the pure 4% baseline.

4. The June Deadline & The $1,000 Early-Bird Arbitrage

This is a hard cutoff. Jupiter has officially signalled that the rewards program is undergoing a structural rebuild after July 1st. To capture the current launch promotion, you must reach $1,000 in cumulative spending by the end of June.

To lock this in:

- Navigate to the "Spend" tab in your Jupiter App to enter the the invite code RDLJCPH9.

- This hardcodes your eligibility for the $100 early-bird bonus.

- Activate the code and complete the KYC process and fund your account with USDC on Solana.

- Clear $1,000 in total cumulative spend before June 30th.

The Math: If a user routes $1,000 of organic monthly spending (groceries, utilities, or high-ticket items) through the card, they capture the $40 native baseline yield (4%) plus the $100 early-bird bonus. That is an effective 14% return ($140) credited in USDC.

The window for this specific liquidity incentive is closing. You are not choosing between a sign-up reward and daily yield: they do stack. If you are in the US or APAC, the time to deploy is now.

For more intel on blockchain tech, crypto & market insights from the perspective of {meta}cognitive and behavioural economics but not only, join me at my X / Twitter account and follow at Publish0x.