I spent the last three weeks buried in spreadsheets, on-chain dashboards, and SEC filings that most crypto traders will never open. And honestly? What I found made me question almost everything I thought I knew about where the smart money is actually flowing right now.

What "Analyzing 47 Funds" Actually Looked Like

I didn't just scroll CoinMarketCap and call it research.

I pulled data from RWA.xyz, Dune Analytics, DefiLlama, and Token Terminal. I cross-referenced AUM figures, yield rates, lock-up terms, blockchain deployments, and this is the part nobody does, whether these tokens actually do anything in DeFi beyond sitting in a wallet looking pretty.

I looked at tokenized Treasury products, private credit protocols, commodity-backed tokens, and even the weird corner of tokenized real estate. Forty-seven distinct products. Two all-nighters. One very strong coffee habit. What emerged wasn't a neat story. It was a power shift. And most of it is happening in plain sight while CT argues about whether Saylor selling 32 Bitcoin matters.

The Numbers Don't Lie - Even If Nobody's Reading Them

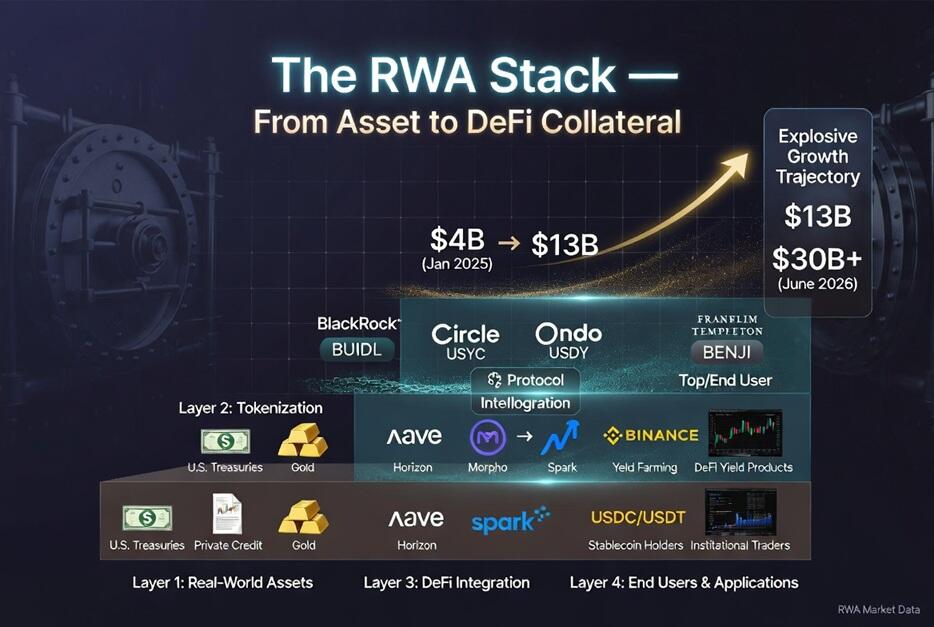

At the start of 2025, tokenized Treasuries were a $4 billion sideshow. By March 2026, that number hit $12.99 billion. That's a 225% explosion in roughly fifteen months. And by May 2026, the broader on-chain RWA market crossed $30 billion, adding over $10 billion in the first five months of the year alone. Let that sink in.

The entire NFT market at its peak was what, $40 billion? Mostly JPEGs and vapor. This is U.S. government debt, private credit, and gold, the most boring, reliable assets on Earth, now living on Ethereum, Solana, XRP Ledger, and a half-dozen other chains. And it's growing faster than DeFi did in 2020.

Why? Because for the first time in crypto history, the product is better than the marketing. Tokenized Treasury funds yield 3.5% to 5% APY while staying liquid enough to collateralize a loan on Aave or back a stablecoin. Your traditional money market fund at Fidelity can't do that. It just sits there, earning the same yield, trapped in a brokerage account like it's 1998.

The Market Is More Crowded Than You Think

When I started this deep dive, I assumed BlackRock BUIDL was the entire game. I was wrong. BUIDL is massive, tracked at $2.17 billion as of late March 2026, and it has grown since. But Circle's USYC actually leads the category at $2.69 billion. Ondo Finance's USDY sits at $1.31 billion. Centrifuge's JTRSY hit $1.12 billion. Franklin Templeton's BENJI is knocking on the door at $990 million. Spiko's EUTBL and WisdomTree's WTGXX are both over $900 million.

That's seven funds over $900 million. Seven. In early 2024, there was basically one.# And the competitive dynamics are brutal. USYC's market share collapsed from 43.8% to as low as 3.5% in mid-2025 before recovering to 20.7%. BUIDL swung from 16.3% to 44.7% and back down to 16.7%. This isn't a gentle monopoly. It's a knife fight between the world's largest asset managers, and the winner gets to define how institutional money moves on-chain for the next decade.

BlackRock knows it. In May 2026, they filed with the SEC for two additional tokenized funds plus onchain shares for an existing $7 billion money-market fund. They aren't experimenting anymore. They're building a product suite.

The Real Story: These Tokens Actually Work Now

Here's where my analysis got genuinely surprising. I expected most of these tokenized treasury funds to be walled gardens, buy, hold, collect yield, redeem. Boring. Useful, but boring.

What I found instead was an integration layer that is quietly rewriting DeFi's risk engine.

In April 2026, BlackRock, Standard Chartered, and OKX announced a joint framework allowing BUIDL to be posted as yield-bearing collateral for institutional trading. That means margin capital that used to sit dead in a prime brokerage account now earns 4.5% while backing a leveraged position. Binance had already started accepting tokenized RWAs like USYC and cUSDO as off-exchange collateral in late 2025. DBS Bank announced plans to let clients use Franklin Templeton's tokenized MMF as loan collateral. And then there's Spark. The Spark Liquidity Layer allocated $1.5 billion to tokenized RWAs, including $800 million specifically in BUIDL, within a $3.5 billion managed portfolio.

This is the part nobody on Crypto Twitter talks about. The tokens aren't just yield products anymore. They're collateral. They're settlement rails. They're the underlying asset class that might eventually back the next generation of stablecoins and lending protocols.

Aave gets it. They launched Horizon, an institutional RWA market targeting $1 billion in deposits in 2026. Morpho Protocol just raised $175 million at a $2 billion valuation in June 2026, during a bear market, no less, specifically to deepen bank and fintech integrations for RWA-backed lending.

If you're wondering where the actual institutional adoption is happening, it's not in memecoins. It's here.

Private Credit: The $2.3 Billion Elephant in the Room

Tokenized Treasuries get the headlines because they're easy to understand. But private credit on-chain is where the yields get interesting.

Total active loans across on-chain private credit protocols hit $2.29 billion by March 2026, up from $400 million at the start of 2025. That's a 477% surge. But here's the wild part: Maple Finance essentially is the market. Their active loan value grew 894% to $2.13 billion, giving them a 93.1% market share. Centrifuge, which once held 20.6%, is now down to 3.3%. Goldfinch fell from 17.6% to 2.5%.

It's a monopoly. And it happened fast.

I dug into why. Maple's borrowers are mostly crypto-native trading firms and market makers, the kind of entities that need liquidity during volatile periods. The other protocols focused on real-world private credit, like tokenized receivables and SME loans, which sounds noble but moves slower and carries more idiosyncratic risk. In a bear market, fast-moving crypto collateral won. Real-world SME lending lost.

That tells you something about where the demand actually is right now. It's not farmers in Kenya needing loans. It's quantitative funds in Singapore needing overnight liquidity.

The Brutal Truth About RWA Tokens

Now for the part that genuinely shocked me.

Despite the sector's explosive growth, RWA project tokens have been absolutely demolished. I checked the price performance of the top seven RWA protocols from January 2025 through March 2026. Six out of seven were down between 44.7% and 98.8%.

Ondo, the leading tokenized asset issuer, crashed 80.6%. Mantra collapsed over 90% even after a rebrand. Centrifuge and Goldfinch got cut in half or worse. The only winner? Maple Finance's SYRUP, which managed a 28.6% gain, and even that came after a 40% drawdown and a wild 300% rally that gave most of it back.

This is the most important disconnect in crypto right now. The sector is maturing. The tokens are dying. The value creation in RWA is accruing to the asset managers, the custodians, and the TradFi institutions, not to the governance tokens of the protocols issuing them. BlackRock doesn't have a token. Circle doesn't have a tradable equity token. The yield goes to the fund holders. The infrastructure fees go to the banks.

If you bought ONDO thinking you were buying "exposure to the RWA megatrend," you got the narrative right and the asset wrong. The megatrend is real. The token was just a proxy that the market stopped caring about.

The Three Funds That Actually Surprised Me

Out of the 47 I analyzed, three stood out for reasons I didn't expect.

WisdomTree's WTGXX posted a 6,762% market cap gain in the tracked period. Not because it was tiny and got lucky, though it did start small, but because it found a regulatory path and distribution channel that others missed. It proved that being boring and compliant is now a competitive advantage in crypto.

Centrifuge's JTRSY grew 2,690% over the same window, despite Centrifuge's native token getting wrecked. This tells me the tokenized Treasury product itself has product-market fit even when the protocol's governance token doesn't. The asset and the equity are decoupling.

Superstate's USTB didn't have the biggest numbers, but it had the cleanest UX and the most transparent reserve reporting I found. In a space where "trust me bro" is still the default disclosure standard, actual transparency is a moat.

What This Means If You're Not a Hedge Fund

Most of us can't buy BUIDL directly. The minimum is typically $5 million, and you need to be a qualified investor. That's fine. The indirect exposure paths are where the real opportunity lives.

Path one: Hold yield-bearing stablecoins or savings products like sDAI, sUSDS, or similar wrappers that pass Treasury yield through to you. These products are increasingly backed by tokenized RWA reserves.

Path two: Pay attention to which DeFi protocols are integrating RWA collateral. When Aave Horizon hits $1 billion in institutional deposits, the protocol's risk engine changes. The composability changes. The yield sources change. Being early to those protocol shifts matters more than picking the right RWA token.

Path three: Watch the regulatory calendar. The EU's MiCA framework, Japan's Progmat platform, and the U.S. GENIUS Act are all moving in 2026. The jurisdictions that clarify custody rights for tokenized securities first will see the capital flows first.

The Chart You Need to See

So Where Is This Actually Going?

JPMorgan, McKinsey, and the World Economic Forum all project $5 to $16 trillion in tokenized assets within a decade. That sounds absurd until you realize the market already went from $5 billion to $30 billion in under two years. The compound math checks out if the regulatory dominoes keep falling.

And they are falling. BlackRock's May 2026 SEC filings weren't a press release. They were a signal to every other asset manager on Earth: the infrastructure is ready, the clients are asking, and the first-mover advantage is closing fast. Fidelity, Vanguard, State Street, they're all watching.

The tokenized Treasury fund is not a crypto product. It's a TradFi product that happens to live on a blockchain. And that's exactly why it will win.

Real talk? I went into this research expecting to find another overhyped narrative with no substance. What I found was the opposite, a sector with so much substance that the hype hasn't even caught up yet. The tokens might be down, but the assets are up, the integrations are live, and the institutions are moving billions while retail panics about Bitcoin ETF outflows.

If you're still measuring crypto's health by what Coinbase lists or what Elon tweets, you're looking at the wrong indicators. The future of on-chain finance is being built in Treasury bills, private credit, and collateral frameworks that most traders will never click on.

But the yields? Those will find you anyway.

Which of these 47 funds would you actually put money into, and which ones do you think are ticking time bombs? Drop your take below. I'd genuinely like to know if I'm wrong about the token disconnect.