Are they really the same? 🤔

There has been a lot of talks recently about MELD being similar to AAVE. And as they do share many similarities, there are some distinct differences between them…

https://youtu.be/e0cd5ET_k0Q?t=724

https://youtu.be/e0cd5ET_k0Q?t=724

Contents

- Core features of AAVE

- Core features of MELD

- Tech & use

- Significance

📊 Core features of AAVE

You can lend and borrow cryptocurrencies! Users can deposit crypto, and earn an interest return per year. After depositing, users also gain the ability to borrow against their position.

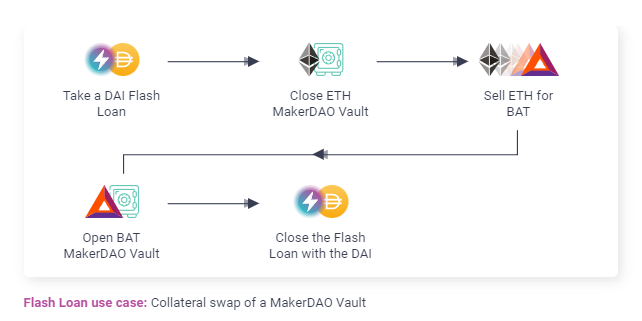

Flash Loans are another unique thing with AAVE. It acts as the first uncollateralized loan option in DeFi! It’s designed for developers to be able to borrow instantly with no collateral… literally mind-blowing stuff you can do with value.

There are many use cases as to why someone would want to do this such as arbitrage across exchanges/liquidity pools, collateral swapping, and even self-liquidations.

Read AAVE docs for more info

📊 Core features of MELD

MELD will act similar to AAVE in many regards. 2 differences to mention with MELD would be their crypto-backed fiat loans and their Genius Loan.

Crypto-backed fiat loan

With MELD, you can fiat currencies from your crypto collateral!

Genius Loan

Ada, Cardano’s native token, has a unique property about it that allows it to still be contributing to the network, earning block rewards (ada %APY), while being able to be used in DeFi and bridging activities.

💻 Tech & use

Are there significant advantages or disadvantages to the blockchain underlying MELD and AAVE?

AAVE is functioning currently, where MELD is set to be operational sometime this year. This is because of the current struggles with the Cardano blockchain itself. not MELD specifically. So in that sense, if we are caring about TVL at the exact moment, then a protocol to build on a blockchain that is able to accept the DeFi requirements at this exact moment would be viewed as an advantage.

But MELD’s main focus here is not to just attract liquidity. They are trying to offer a more efficient user experience, from all angles. Through the UI and ease of use, but even more importantly — through the cost of transactions.

There are some disadvantages currently that exist on the ETH blockchain that limit users from maximizing their fullest potential. And this is due to gas fees. For positions that are bearing a 10% APY, for example, would only seem feasible to those who maybe have over $5000 USD, and are wanting to keep it staked for over a year. As you would likely have to pay $50–$100 in transaction fees alone to enter and exit the position.

As for Cardano, the blockchain MELD is building on, has fees much less than this, opening up attractive value management opportunities to those who don’t have as much capital.

AAVE does exist on Polygon and Avalanche, layer 2 side chains to Ethereum. Users can bridge their assets from the Ethereum blockchain to one of these networks. The benefit of doing this is lower transaction fees.

But how can this actually be beneficial? 👇

Bank transfer to exchange → buy crypto → send to Ethereum wallet (layer 1) → bridge to Polygon or Avalanche (layer 2) → utilize layer 2 DeFi services → bridge out to layer 1 → transfer back to exchange → transfer back to bank.

Who would actually do this?

A lot of people do this… and it only really starts to make sense, under the current conditions, if you have <$5000 USD and want to keep in within the ecosystem for a while.

What has AAVE been used for by individuals and what do we expect to see from MELD?

People use AAVE for a variety of different subjective reasons. A good way to look at and understand AAVE, MELD, and any of these DeFi protocols, is to see them as a tool that can be used. Similar to a hammer and a wrench. They can do things, and the reason why you use them may differ from person to person.

You deposit crypto into a position (smart contract) → you gain the ability to borrow a certain % of your locked collateral. (The exact % different crypto to crypto)

Why do people do this?

- Earn an interest return for lending out your crypto

- Hedge position

- Leverage position (Ex. deposit ETH → borrow USD → buy more ETH)

There are some protocols that will actually perform leveraging for you, and you just choose the % you’d like!

- Exposure to different assets

- It’s relatively cheap (cost to borrow) for the value it offers the user and can be extremely capital efficient

What have you personally used in DeFi lending and what are you looking forward to using in the future?

I dabble here and there, test things out. Mainly out of interest. Reading about something is MUCH different than experiencing it. Especially when value and emotions are involved.

Ethereum-based protocols

Ethereum-based protocols

✨ Significance

What significance do AAVE and MELD bring to their ecosystems more broadly?

AAVE provides decentralized, non-custodial tooling and utility for anyone that wants to use it. MELD will be providing the same + fiat capabilities. On top of this, MELD is creating ADAmatic. Which is a bridge to connect Cardano with Polygon — allowing liquidity to flow between the Cardano, Polygon, and the Ethereum blockchain.

AAVE does also bring further capital efficiency through the introduction of Polygon and Avalanche.

Does that significance reach beyond their own blockchain protocols and ecosystems?

Yes. For Cardano specifically with ADAmatic — opens up an opportunity for DEX liquidity providers to earn trading fees for one of the top 10 currencies, ada. This is tremendous for any DEX that is built on ETH or Polygon. The question then becomes, how much of the $42b dollar market cap of ada will want to go over to ETH?

https://coinmarketcap.com/currencies/cardano/

https://coinmarketcap.com/currencies/cardano/

I would guess an extremely high percentage…

- The ada being bridged will still be earning an interest return through continued delegation to Cardano stake pools → earning block rewards APY.

- There will be opportunities emerging on the ETH blockchain, such as Uniswap V3 Polygon liquidity providing(Uniswap fee article to be written…) where liquidity providers could earn trading fees through users buying and selling the wrapped version of ada.

Bridging Cardano → Polygon VS Bridging Ethereum → Polygon

When you wrap ETH to another blockchain, the ETH gets locked into a smart contract and just sits idle. Whereas on Cardano, the ada that is “locked” on the Cardano blockchain, is still able to be productive, and contribute to the network, thus earning block rewards. (ada rewards distributed to stake pool delegators)

Introducing DeFi to Cardano

This has the potential to, at minimum, introduce another ~$22b USD in stable coins into the ecosystem. This translates into $22b USD worth of potential buying pressure for other assets.

People complain about the government's printing money… I have a perspective that, if they weren’t to do this, they would have no power/control then. Because they are not financial masters, they would eventually lose power over those to those who participate in the production of value through DeFi and more specifically derivatives, and then have no say in any matters.

It’s sad because it really pushes those who are not benefitting directly from — the money that is being printed or those who are not utilizing DeFi tools or derivatives for the production of value — into a deeper hole.

Well, that’s at least how I conceptualize it! Maybe my perspective is wrong. What’s yours?

Thanks for reading :)

- Stu

DeFiKnowledge

Let’s stay connected! 🔗

Twitter | Instagram | Medium | Telegram group chat