Inflation, debt, and geopolitics are converging into a test policymakers may not fully control

The change is subtle, but increasingly visible.

For years, markets operated on a core assumption. The Federal Reserve could guide the economic cycle with a reasonable degree of control. Inflation could be managed. Growth could be supported. Disruptions would be met with credible and effective policy.

That assumption is now under pressure.

Not because policymakers lack intent, but because the system itself has become more constrained. Debt levels are higher, global demand patterns are shifting, and inflation dynamics are being driven as much by geopolitics as by domestic policy.

Inflation Is Already in Motion

The latest pressures are not originating in financial markets. They are coming from the real economy.

Energy prices rose sharply earlier this year amid renewed tension in the Middle East. While prices have moderated, economists note that the effects of such moves tend to filter through slowly. Fuel costs feed into transport, food, and manufacturing over time.

By the time inflation appears in official data, much of the process is already underway.

This creates a policy challenge. Central banks respond to inflation that reflects the past, while markets begin pricing what comes next.

The Limits of High Rates

For much of the past two years, elevated interest rates provided a sense of stability. Cash and short-term government debt offered positive real returns, allowing investors to remain cautious without losing purchasing power.

That balance is becoming less secure.

If inflation begins to move above short-term yields, real returns on cash turn negative. At that point, the incentive structure changes. Investors are pushed toward risk assets or alternative stores of value, not out of optimism, but out of necessity.

Such shifts tend to mark the early stages of broader capital reallocation.

Debt Is the Real Constraint

The more structural issue lies in the scale of U.S. government debt.

Interest payments have become a major component of federal spending. As yields rise, so does the cost of servicing that debt. Each refinancing cycle adds pressure, narrowing the range of viable policy options.

This dynamic is shaping expectations around future Federal Reserve leadership, including figures such as Kevin Warsh. While debate often centers on policy stance, markets increasingly view the constraints as pre-determined.

There are limits to how long rates can remain elevated without creating stress within the system itself.

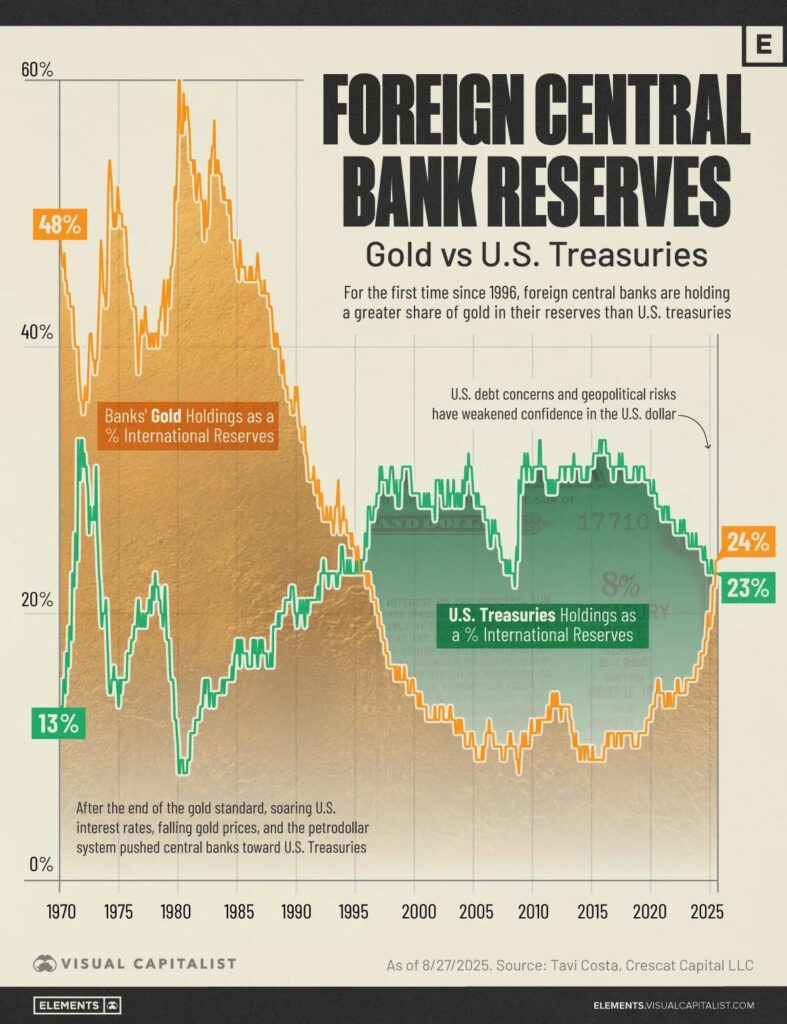

Concerns are also emerging around demand for U.S. Treasuries. Analysts point to reduced foreign participation and a growing reliance on leveraged domestic buyers. Former Treasury Secretary Hank Paulson has warned that disruptions in this market could prove significant.

These are not isolated developments. They point to a shifting foundation.

A Divided Inflation Outlook

At the same time, a new narrative is gaining traction. Advances in artificial intelligence are expected to drive productivity and reduce costs across parts of the economy.

There is evidence to support this, particularly in software and services.

But the impact is uneven. AI does not materially reduce the cost of energy, raw materials, or infrastructure. In some cases, it increases demand for them.

The result is a more complex inflation picture. Disinflation in digital sectors may coexist with persistent cost pressures in the physical economy.

This complicates policy decisions, particularly around the timing and scale of any shift in interest rates.

Markets Are Positioning Ahead

While policymakers continue to assess conditions, markets are beginning to adjust.

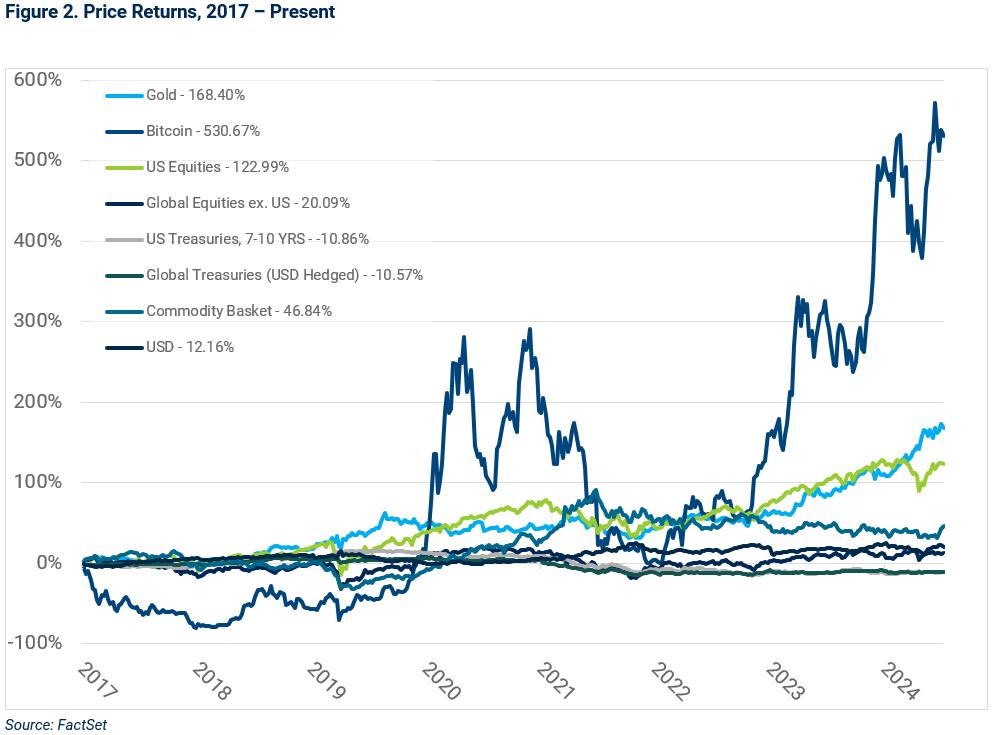

One example is Bitcoin, which has shown resilience despite cautious sentiment. Analysts often interpret such behavior as a response to expectations around liquidity rather than short-term fundamentals.

Bitcoin has historically been sensitive to changes in real interest rates. Periods of declining real yields have often coincided with stronger performance.

More broadly, the behavior of alternative assets suggests that parts of the market are positioning for a shift toward looser financial conditions, even as inflation risks persist.

A System Under Pressure

For households, these dynamics translate into rising costs and greater uncertainty. The balance between saving and investing becomes more complex when real returns are less predictable.

For policymakers, the challenge is equally difficult. Managing inflation, maintaining financial stability, and supporting government financing needs are objectives that increasingly pull in different directions.

The Transition Ahead

The most likely outcome is not a sudden break, but a gradual adjustment.

Central banks are likely to respond as pressures build, potentially easing policy if financial conditions tighten. Governments will continue to rely on debt markets, even as demand evolves.

Markets, however, are unlikely to wait.

As these forces converge, the perception of control may continue to erode, replaced by a more constrained and reactive policy environment.

This is not a collapse. It is a transition.

One where the limits of the current system are becoming clearer, and where both markets and policymakers are adjusting in real time.

Recommended reading:

The Fed’s Crypto Playbook: How Central Bank Actions Create Trading Opportunities

The Emergency Financial Exit Plan: What To Do If Your Country’s System Starts Breaking

How To Stop Being Economically Fragile

The $100 Trillion Wealth Transfer: Why Crypto Is the Only Asset Class Designed for Millennial Inheritance

The Bitcoin Accumulation Playbook: Copying Michael Saylor with $1,000

How To Build a Crypto-Ready Emergency Fund