Vigor protocol is a very advanced DeFi platform but is not that difficult to understand once you get used to it. There are some typical features in common with other lending platforms but also some notable innovations that deserve to be explored and explained.

This article is inspired by the most frequently asked questions in our main chat and will try to clarify to the user the concept of Loans, Bailouts,Lending, Savings, VIG lifeline, Reputation Score, Level of Protection and final reserve. Let’s dig into it.

LOANS

Why would I need a loan?

app.vigor.ai

app.vigor.ai

Taking a loan is not necessarily something you do only when you are about to be rekt, it can also be done as a strategy. Thanks to the advanced characteristics of VIGOR and the free transactions on EOS, you can use loans as a “step” into your earning strategy.

Let’s sum it up with a few examples:

Lever up on EOS: deposit EOS, borrow VIGOR, buy more EOS.

Monetize: deposit EOS, borrow VIGOR, buy a car (you still own your EOS and don’t have to sell them).

Short: deposit VIGOR, borrow EOS, sell short on exchange, wait for market to drop, buy back and repay loan.

Hedge: borrow VIGOR for stability, deposit to savings get rewarded with VIG, and others ways.

Arbitrage: IE on defibox.io buy 1 VIGOR paying 0.88 USDT, on app.vigor.ai deposit 1 VIGOR and borrow 0.94 USDT

None of this can be done on other networks since the fees will eat you alive. Instead, on EOS+VIGOR you can! And you are encouraged to do so!

app.vigor.ai

app.vigor.ai

Note:

To open a loan, a minimum of 100 VIG is mandatory to cover the loan premiums, If you close the loan you will be able to withdraw them. Those VIGs are there to help minimize potential bailouts due to running out of VIG.

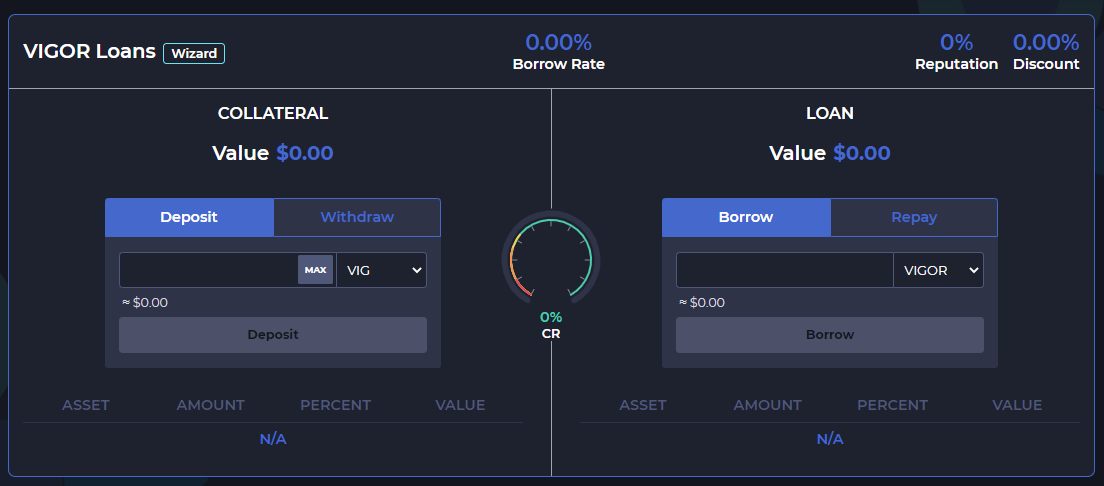

When someone wants to take a loan, let’s say a VIGOR loan, they have to build their collateral basket. Currently you can add VIG, EOS,USDT and IQ to that basket.

For VIGOR vs USDT the minimum collateral Is 106%, all the others are 111%. Liquidation on Vigor happens at 100% and no fees are applied. For comparison Equilibrium liquidates at 130% and MakerDao at 150% CR, their users should not consider less than 175% to start a loan otherwise they risk penalties that can reach 15%.

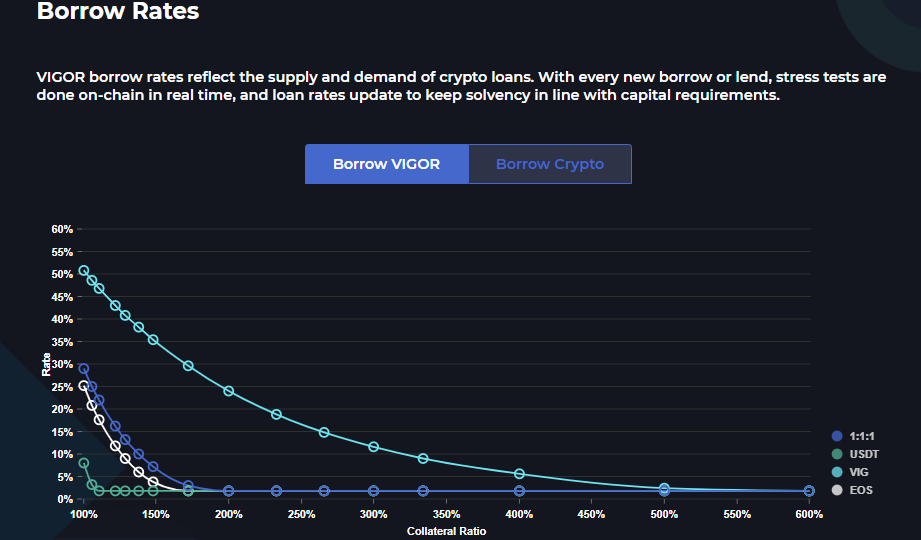

The higher your CR% ( COLLATERAL RATIO ) the better your loan rate, so say you only borrow half your collateral (2:1) your CR% would be 200%. The rate is annualized, variable and depends on your collateral ratio, type of tokens used as collateral, and overall system solvency. In any case, each VIGOR is backed by at least $1 of crypto. And the system treats it as $1.

On VIGOR’s health page there is a graph and a real time calculator as you deposit/withdraw collateral or loan to help you get an idea of your rates and system health.

View the history of your loan rates on stats.vigor.ai

BAILOUTS

What happens if…??

If the prices of all the coins in your collateral basket drop enough that the combined value of your collateral is less than 100% of what you have borrowed. then a bailout occurs.

It’s not specific to any coin, it’s based on the CR% going under 100% of loan value. This happens also if you run out of VIG for premiums, so there’s a mechanism called VIG lifeline that issues VIG as debt to minimize the occurrence of bailouts due to no VIG.

Bailout Guide:

VIGOR Protocol employs some “mitigating tools” to ease the pressure on your loans and four levels of backing for low volatility loans:

Mitigating tools

• On the Vigor platform borrower’s collateral EOS get REX and proxy voter rewards. Those are deposited daily into the same area that you have the EOS.

- Reputation discount: the higher you keep your reputation score in the Protocol the less fees or premiums in VIG are paid to borrow, Reputation takes into account your use of Vigor protocol via: VIG paid (loans) or VIG rewards (Lending and Saving). You are ranked against all other users of the platform on a scale of 0–100%, so your discount scales as well from 0–25% based on that ranking, averaged three months. Example: if your reputation is 60. 0.60 x 25% = 15% discount on whatever base rate you would have based on your CR. Check your Reputation score:

https://stats.vigor.ai/d/mobile/users?orgId=1

Reputation Score Guide:

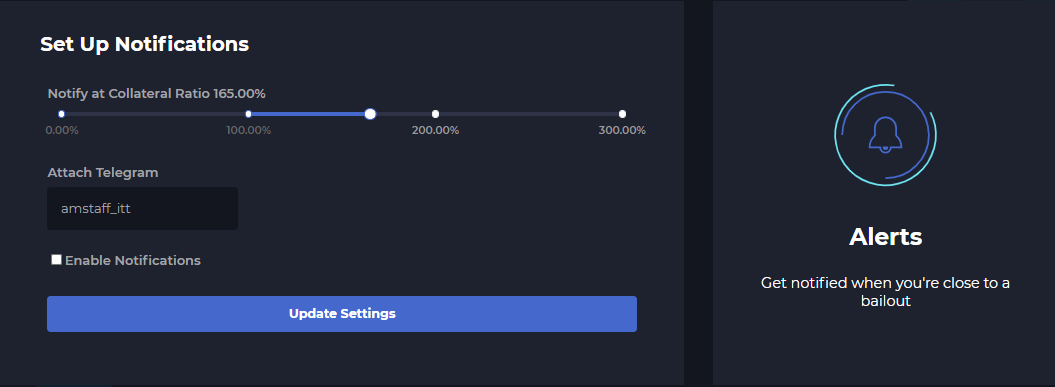

- Make sure to setup a telegram alert and set it up for a CR where you can manage keeping the loan up and avoid bailout.

Four levels of protection

• Borrowers over-collateralize their loans protecting against normal volatility

• Lenders post tokens as insurance assets which provide further backing against price jump risk.

• Final reserve provides a third layer of backing in case the insurance pool depletes.*

• Saving is a collateral to be used after final reserve is depleted

- The system stores a cut of VIG awarded to lenders as final reserves. Check out finalreserve account:

https://stats.vigor.ai/d/mobile/users?orgId=1&var-account=finalreserve&var-totusers=520

VIGOR Loan Protection Levels:

LENDING

Deposit Crypto into a Lending Pool and get Rewards

https://app.vigor.ai/rewards/insure

https://app.vigor.ai/rewards/insure

· Depositing EOS into the lending pool: Rex and Proxy Rewards are deposited daily into the same bucket, VIG Rewards instead will go to a bucket called VIG Fees & Rewards.*

· Depositing USDT into the lending pool: VIG Rewards are going to it’s own bucket called VIG Fees & Rewards.*

· Depositing VIGOR into the lending pool: VIG Rewards are going to it’s own bucket called VIG Fees & Rewards.*

· Depositing IQ ( Everipedia ) into the lending pool: VIG Rewards are going to it’s own bucket called VIG Fees & Rewards.*

* Adding those VIG as collateral or into Lending Pool must be a direct choice by the user.

· Depositing VIG into lending pool: get rewarded in VIGOR, this Rewards are going to Savings pool

· Depositing VIGOR into Savings: get rewarded with VIG Rewards.

Participating in the lending pool you are providing the second layer to back loans. This involves the risk that, if a loan is bailed out, that loan is spread among all lenders proportionately. A lender then is in duty to use its own collateral to pay down that slice of the debt. This is why lenders continuously receive VIG rewards as compensation for the risk.

Some lose some gain

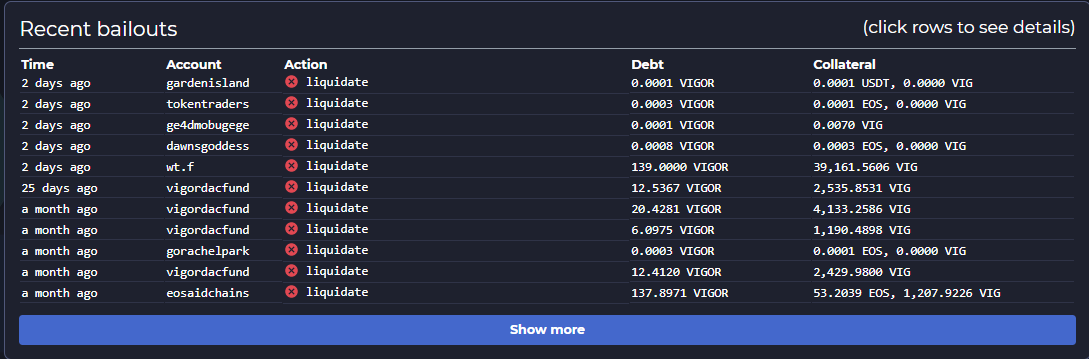

Take a look at the user page “your dashboard” and down at the bottom you can click one of those bailouts to see how every lender received collateral and also a portion of debt https://app.vigor.ai/user

The Debt column is the debt you took over, the Collateral column is the collateral you received from the user who was bailed out.

The lending rate is based on solvency of the system. If the system becomes more risky (due to lower CR rates on loans, or a lack of tokens in the lending pool or even large token price changes in the pool) it will adjust loan rates higher to get users to add collateral or closing some debt. It also raises lending rates to persuade users to add more to the lending pool.

Is it a risk or an opportunity ?

· If the value of the collateral a lender receives continues to drop after he received it, then he has “lost” money (at that time), that’s the risk.

· If the value of the collateral the lender receives goes up after he receives it , then he has gain money ( at that time ) , that’s the opportunity.

If you already have the debt token (VIGOR for example) in lending then it will close the loan right when you receive it and you just keep the collateral. If you don’t have the token in Lending then it will show up as a loan and will move some of your tokens to collateral to keep the loan open until you deposit the VIGOR to close it.

I recommend to users that want to participate in the lending pool to have all the token types in lending. This way the portions of debt you may receive from a bailout is immediately closed and you get the users collateral. Otherwise you carry the debt until you close it out yourself.

Also, if you have only VIG in lending or collateral, adding at least a small amount of EOS,VIGOR,USDT or IQ will improve your rates due to the same diversification benefits.

If shit happens, not everything is lost…

In a worst case scenario, as previously mentioned, if a bailout is triggered because you run out of VIG for premiums, there’s a mechanism called VIG lifeline that issues VIG as debt to minimize the occurrence of bailouts due to no VIG.

VIGOR Lending Pool Guide :

SAVINGS

Lock VIGOR tokens into Savings pool and get rewarded a savings rate on your funds.

https://app.vigor.ai/rewards/savings

https://app.vigor.ai/rewards/savings

The savings rate will float, its value is tied to a percentage of VIG fees total paid in and the total amount of VIGOR in savings, and the savings rate decreases/increases when VIGOR feed price is above/below $1. The savings rate is based off of how many are participating in the savings pool. The system is always assessing risk and adjusting for that risk vice just picking an arbitrary target and hoping for the best. Savings Rewards get rewarded in VIG : VIG Rewards are going to it’s own bucket called VIG Fees & Rewards. It will be a direct action by the user to add VIG as collateral or into Lending Pool .

VIGOR in savings is not legally allowed to be risk free, so savings is positioned in line after the finalreserve to take bailouts, the lowest risk position available on vigorlending. To further keep it legal, with a small tweak, VIG premiums paid to savings go through vigordacfund, and are classified as an expense of the DAC not a profit.

VIGOR Protocol DeFi App Guide:

Vigor DAC and Protocol Links

- Website: https://vigor.ai/

- Vigor Crypto Lending DeFi Application: https://app.vigor.ai

- Vigor DAC: https://dac.vigor.ai

- Telegram: https://t.me/vigorprotocol

- Twitter: https://twitter.com/vigorprotocol

- Medium: https://vigordac.medium.com/

- Vigor DAC YouTube

- Vigor Protocol YouTube

Thank you for your attention to this matter @Zutty , always great to collaborate with you