In today's weekly market updates, we are going to look at what happened in the fixed income, money market, commodities, U.S. equity and crypto markets last week (i.e. the week ending 22 Jul 2022).

The financial market was giving a confused signal last week.

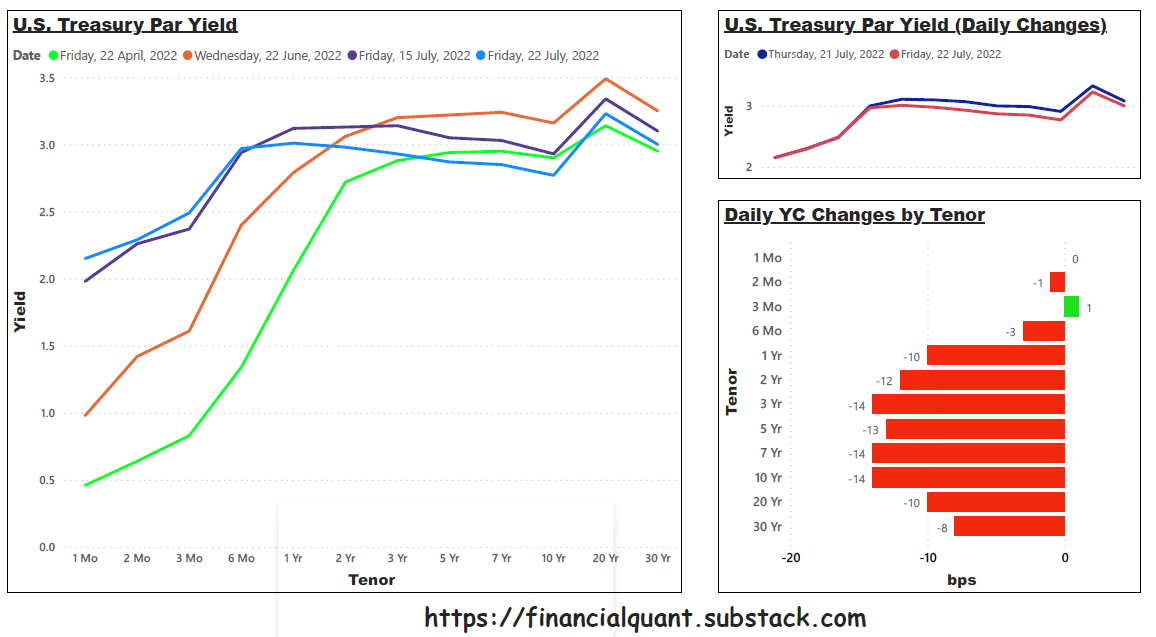

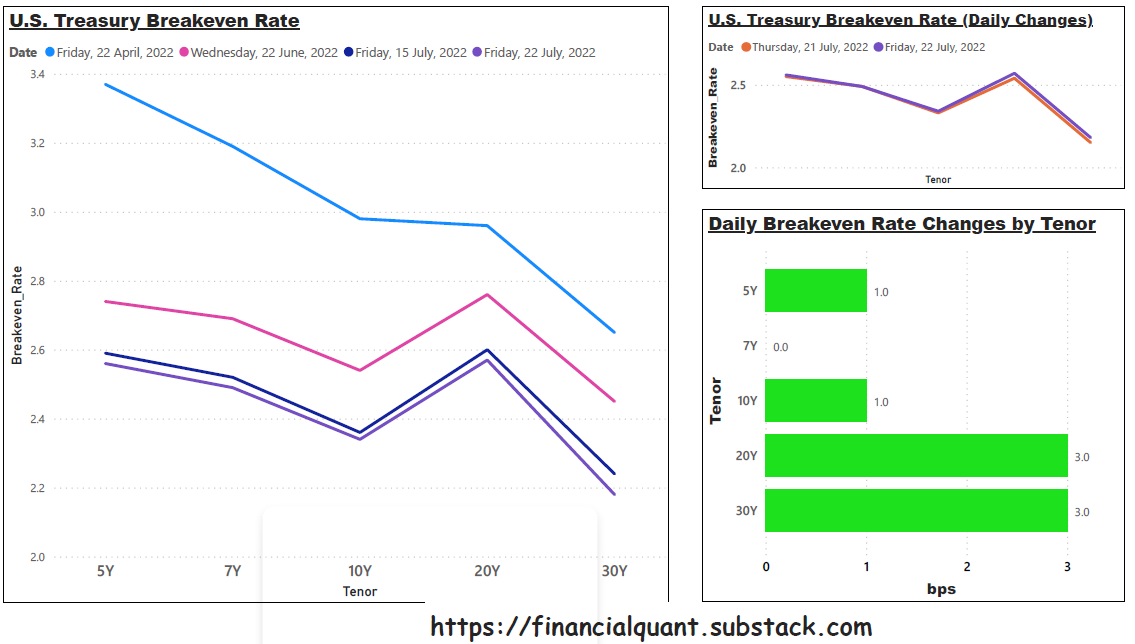

On one hand, the U.S. Treasury yield curve has been flattening and treasury breakeven rates were coming down, a bad sign for the U.S. economy as the whole treasury bond market actions are positioning for an imminent recession.

However, on the other hand, bonds, stocks and cryptos were having a good week with all of them making gains amidst the soaring energy prices.

Investment Disclaimer:

-

I am not a registered investment, legal, or tax adviser or a broker/dealer, and all opinions expressed by me are from my research for educational purposes only.

-

Past performance presented here is not an indicator of future performance.

-

This post expresses my own opinion about the financial market. It is not an offer to buy or sell, or a solicitation of any offer to buy or sell any security mentioned in this post.

Today's market report is available for download at:

Your Daily Market Updates Website

I publish daily and weekly market updates almost daily so that by reading my articles, you would be able to understand the market better and make a data-driven informed decision. If you are interested in my work, feel free to follow me at:

Fixed Income and Money Market

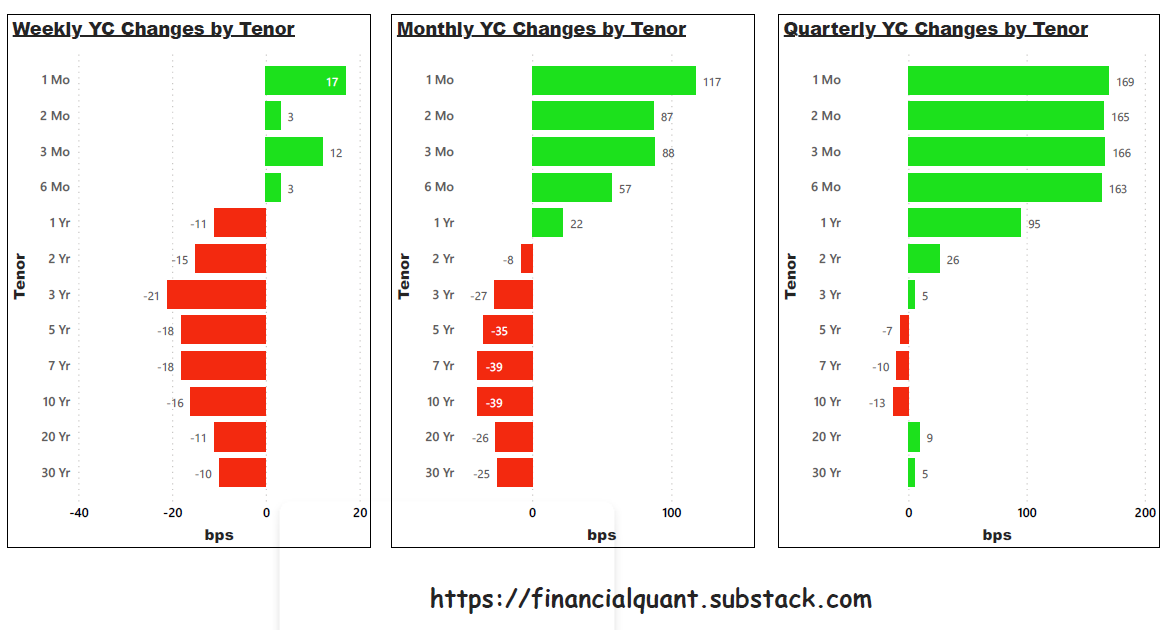

Over the week, near-term U.S. Treasury par yields rose at double-digit basis points while the intermediate to long-term U.S. Treasury par yields dropped sharply with the same magnitude.

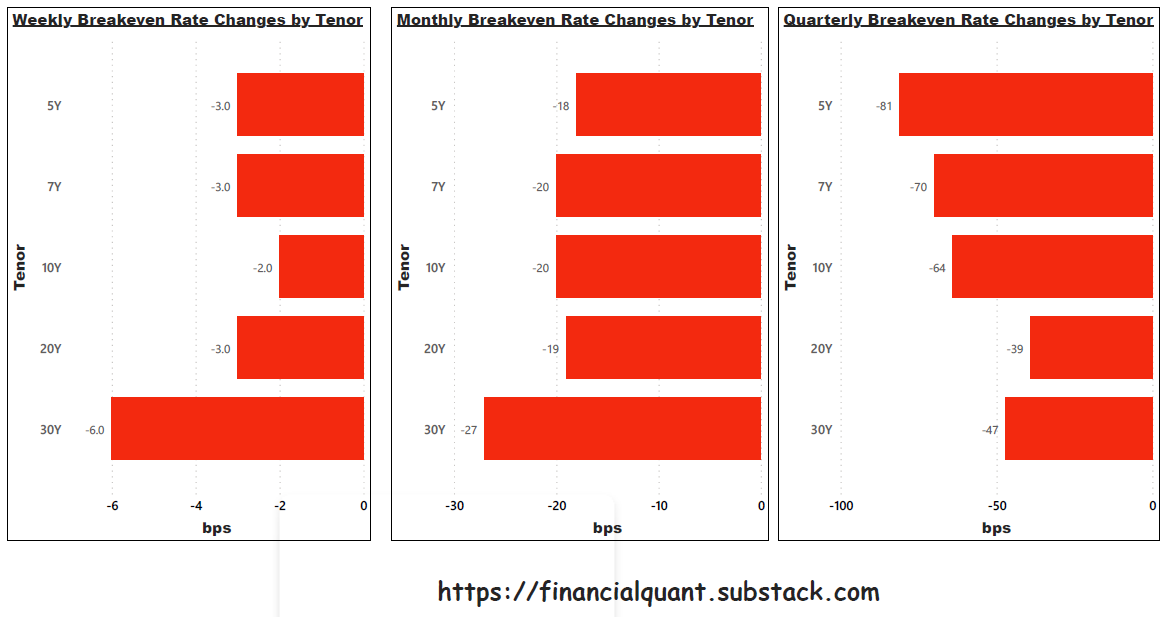

Breakeven rates are calculated as nominal treasury par yield (i.e. the yield of non-inflation protected treasury securities) minus real treasury par yield (i.e. the yield of inflation-protected treasury securities).

Yield is used as a market convention in bond pricing and has an inverse relationship with the bond prices. In another saying, the higher the yield goes, the lower the bond prices are. Because nominal bondholders are taking an inflation risk as compared to inflation-protected bondholders, nominal bonds are always priced cheaper than the inflation-protected bonds, hence, having a higher yield.

While inflation-protected securities would have investors’ principal adjusted higher during an inflationary environment, they would also have their principal adjusted lower in rare circumstances of a deflationary environment. Hence, the nominal yield would only be lower than the real yield in a deflationary environment where one dollar today is worth more than one dollar next month. In this case, investors would prefer to hold normal non-inflation-protected bonds than inflation-protected ones.

A squeeze in the breakeven rate as shown in the diagrams above indicates that the market is pricing in a softer inflation stance due to the economic slowdown.

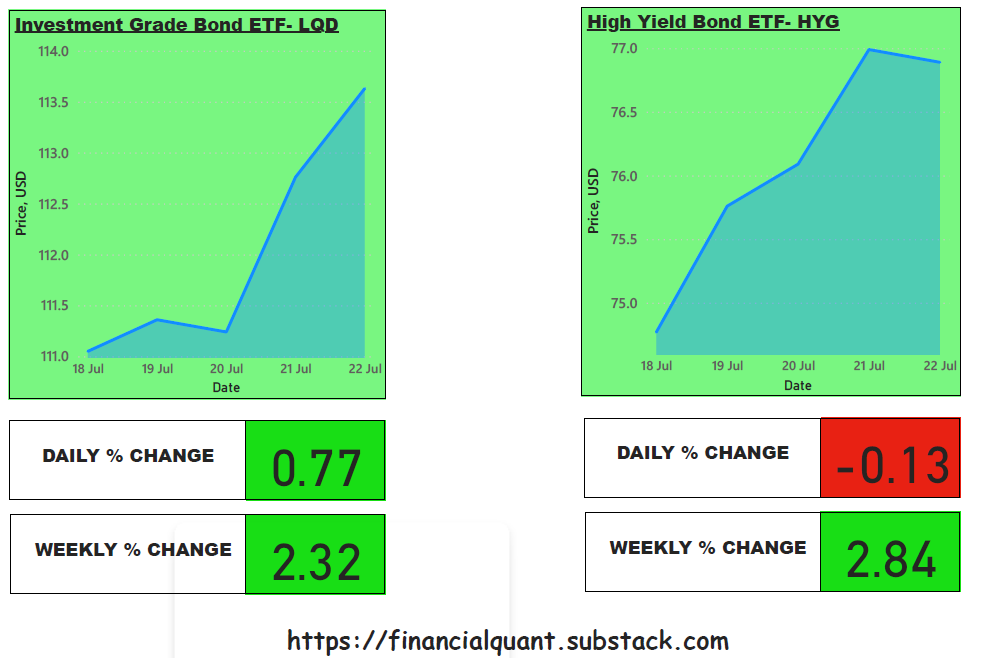

The high-yield bond ETF (NYSEARCA: HYG) is exposed to more cyclical sectors and has more exposure to bonds that are rated BBB and below than the investment-grade bond ETF (NYSEARCA: LQD), therefore, subjected to a higher probability of default and hence more sensitive to the credit cycle. Investment-grade ETF is exposed to more stable sectors and has more exposure to highly rated bonds (rating BBB and above), hence less sensitive to the credit cycle but more sensitive to Fed's rate hike decision. When the economy is booming, high-yield bonds would usually outperform investment-grade bonds and the opposite would happens during a recession.

Last week’s bond market performances, where high-yield bonds outperform investment-grade bonds indicate that the U.S. economy remains strong and investors are pricing in lesser credit spread on the high-yield bonds.

Commodities

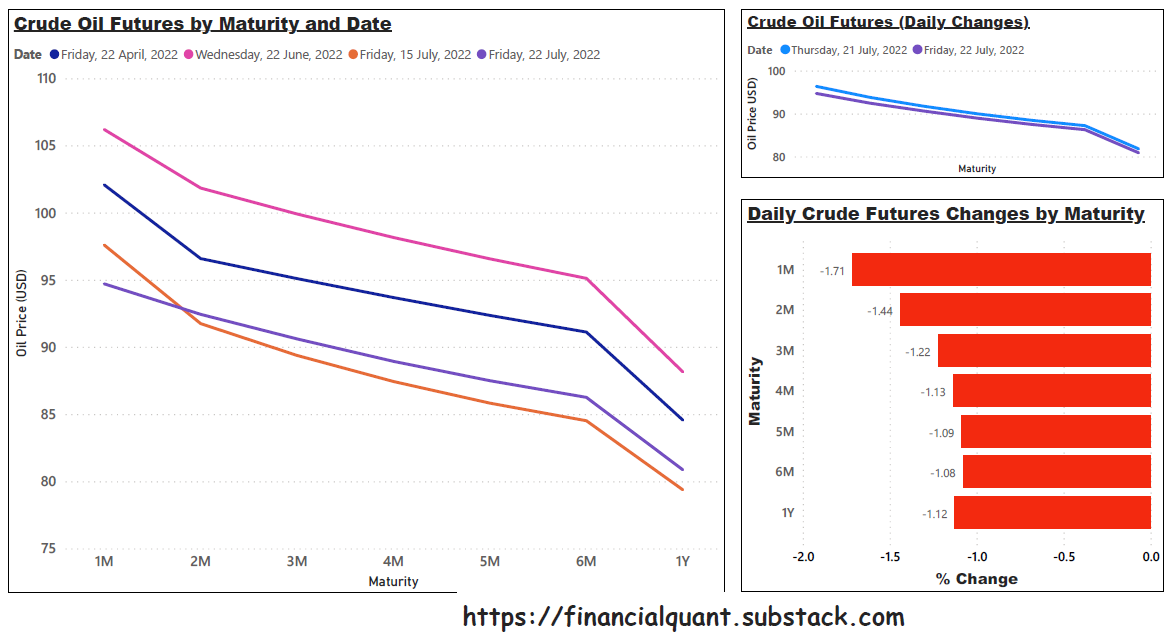

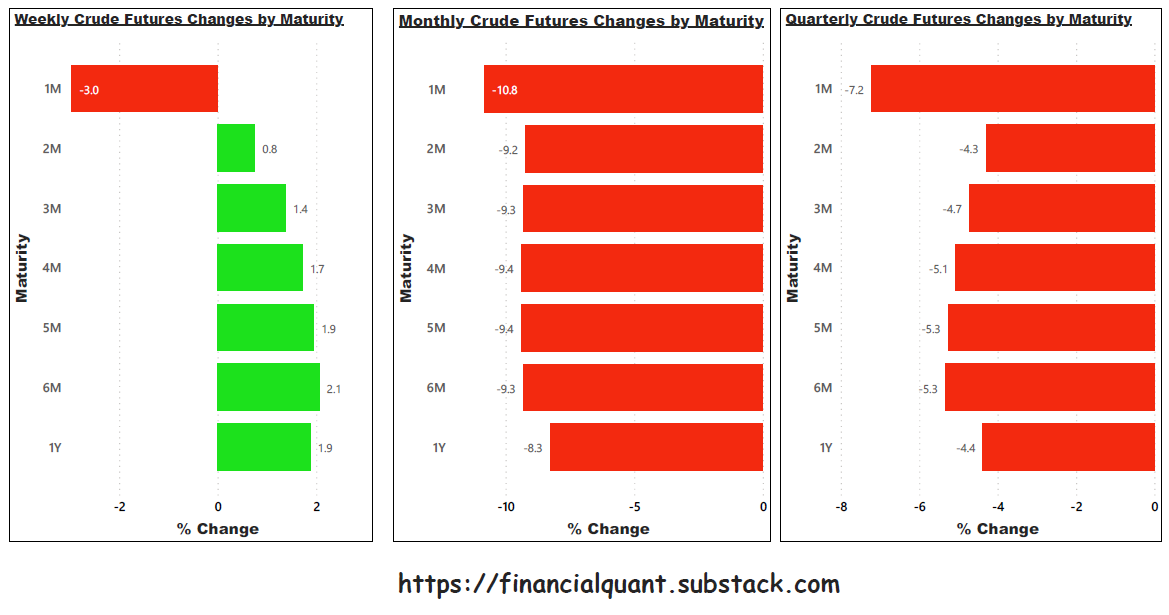

Crude oil futures except the near-term contract ended last week at higher prices as the global economy is opening up after the Covid-19 pandemic while Saudi Arabia revealed that their oil output is near its higher limit.

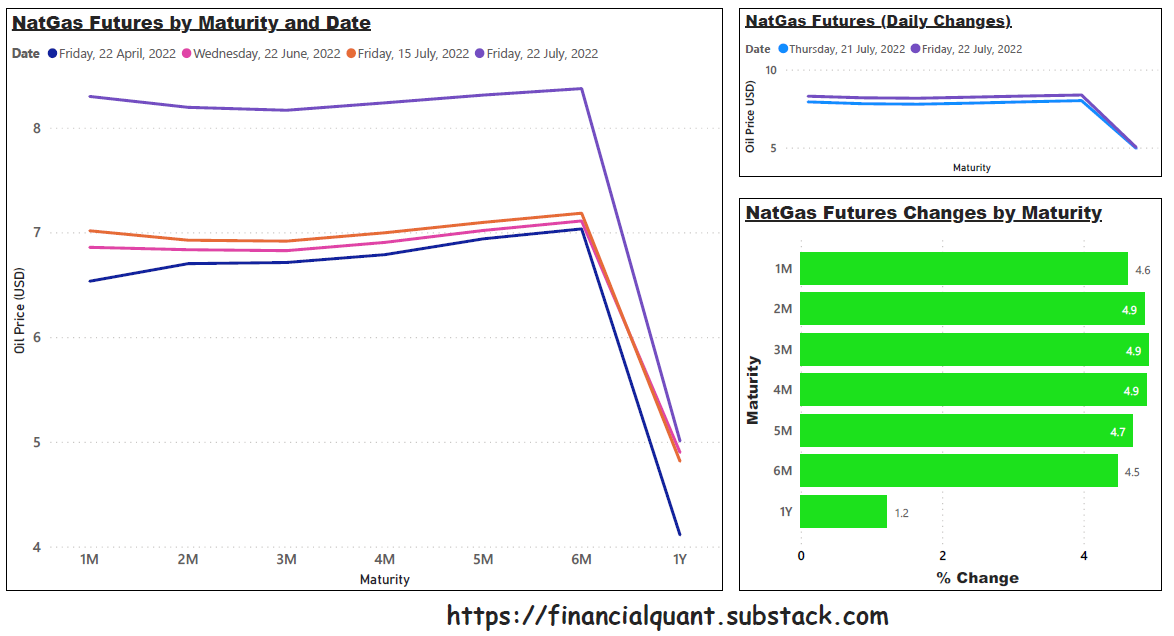

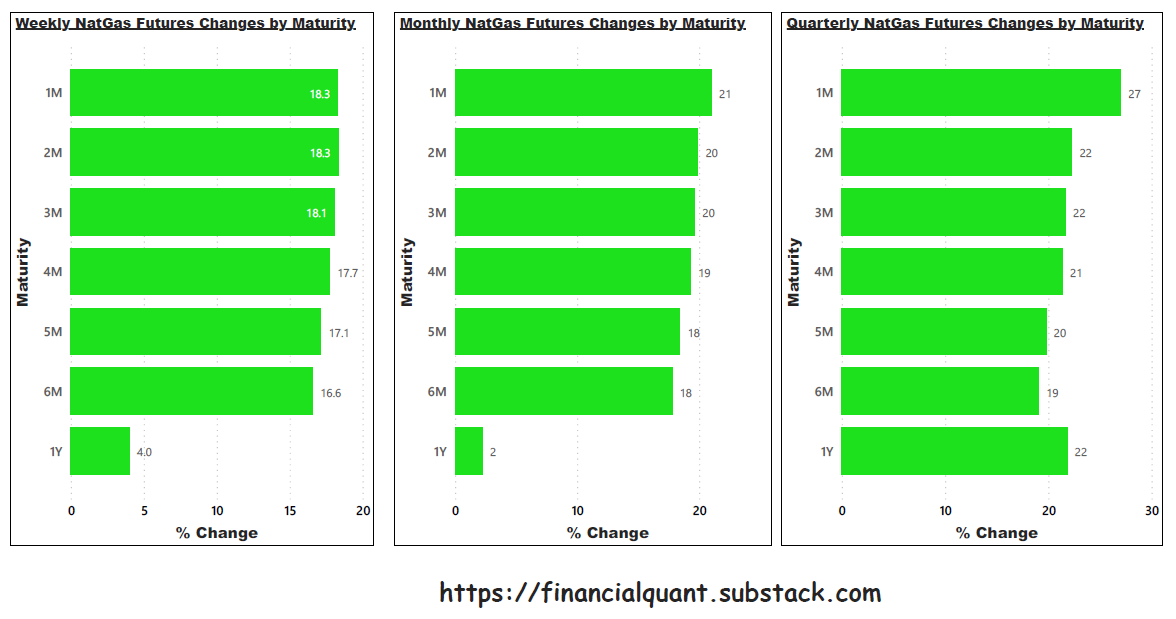

Natural gas futures ended up 16.6% to 18.3% higher last week as the extreme heat wave in the United Kingdom and Europe drove up natural gas demands which are key in all cooling appliances while Russia paused Nord Stream 1, a key gas pipeline between Russia and Europe for maintenance works before resuming it recently.

Equities

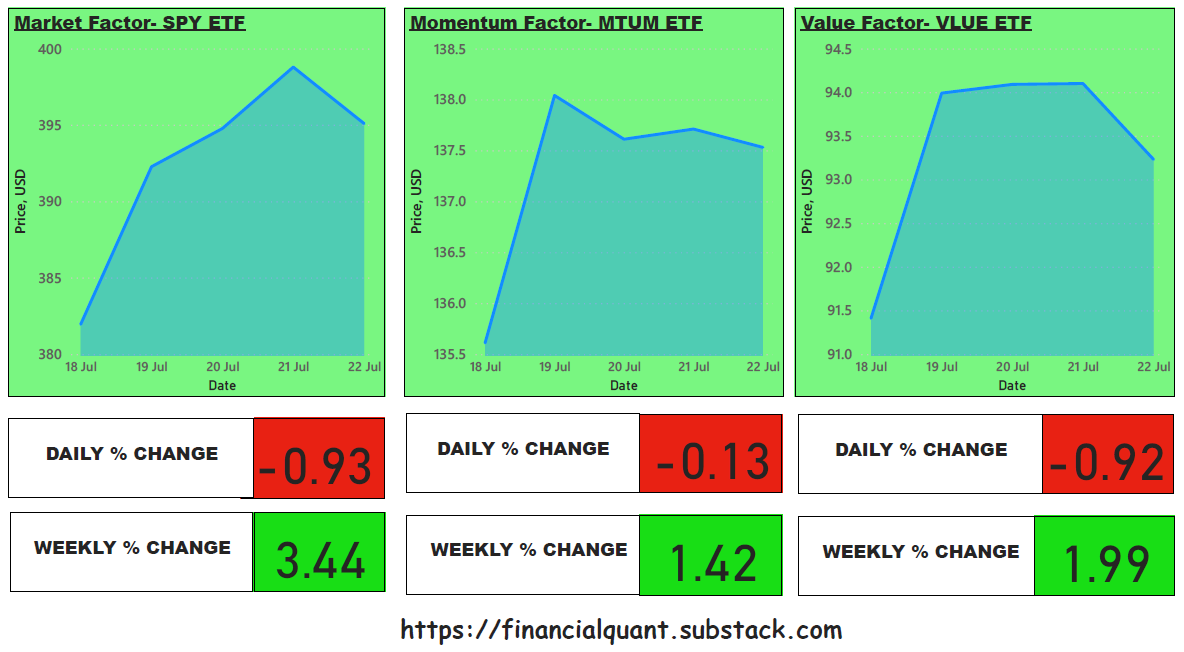

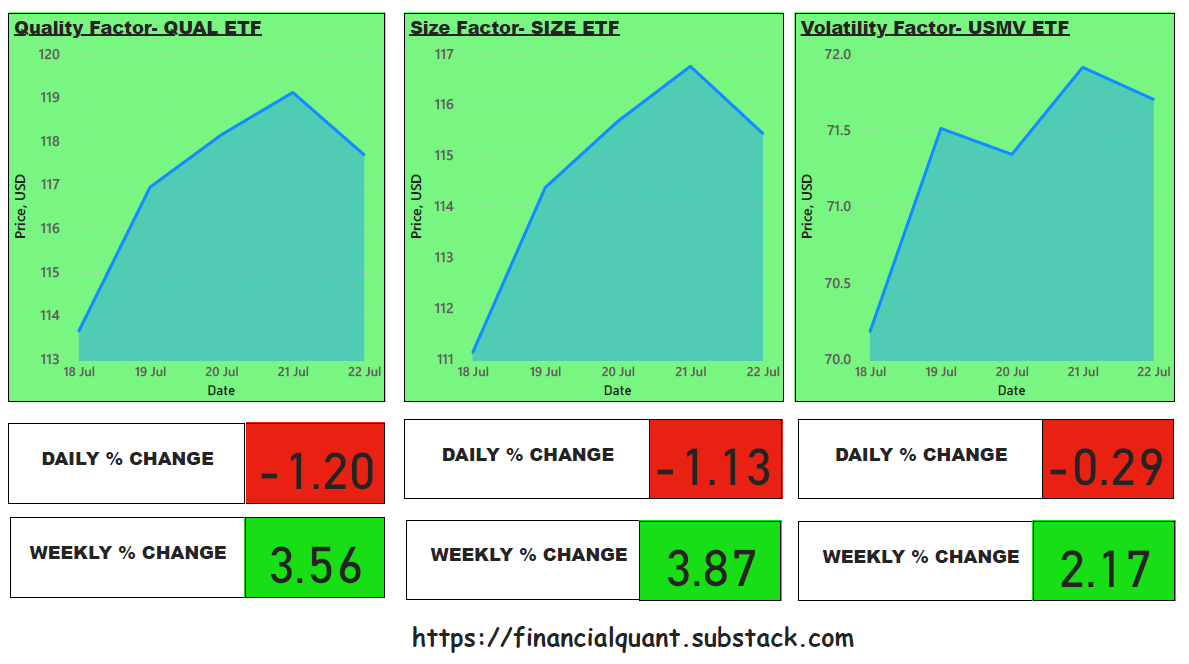

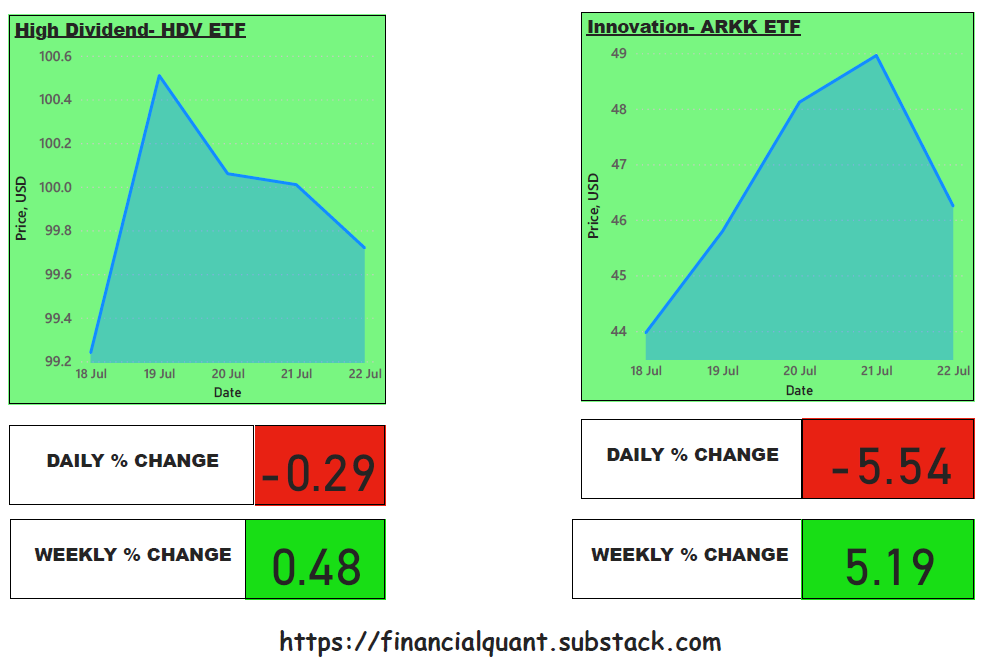

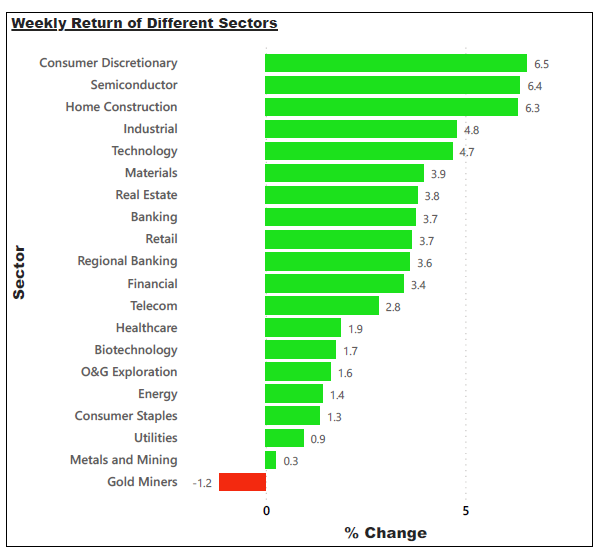

The equity market has had a great week, with S&P 500 market ETF up by 3.56% last week, led by Quality (+3.56%), Size (+3.87%) and Innovation (+5.19%) factors.

All sectors except gold miners were in green last week.

Crypto

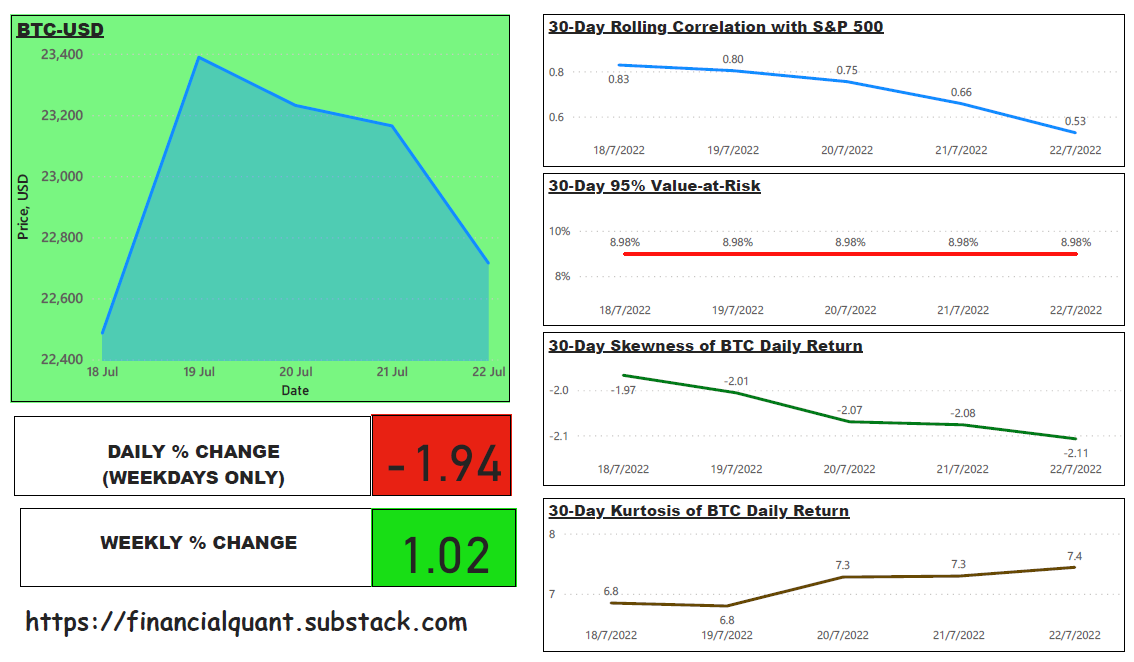

Bitcoin ended the week with a 1.02% gain. The “risk-on” sentiment of Bitcoin has gradually decreased as its 30-day rolling correlation with S&P 500 index fell sharply from a high of 0.88 to now 0.53 over the week.

Despite its gain and a gradual disassociation with S&P 500, Bitcoin’s risk of larger drawdown has however increased based on observed historical data, with an increasing negative skew (i.e. larger probability of making losses than gains) and a higher kurtosis number (i.e. greater risk of large draw-down) as compared to a week ago.

That’s what you need to know for today’s market updates. Please like, share and subscribe if you find this article useful.

Reference:

-

The thumbnail image here was downloaded from Unsplash, where credit is given to Tierra Mallorca, the creator of this photo.