In today's daily market updates, we are going to look at what has happened in the fixed income, money market, commodities and U.S. equity markets yesterday (28 June 2022), and discuss what these would carry for the crypto market.

Fixed Income and Money Market

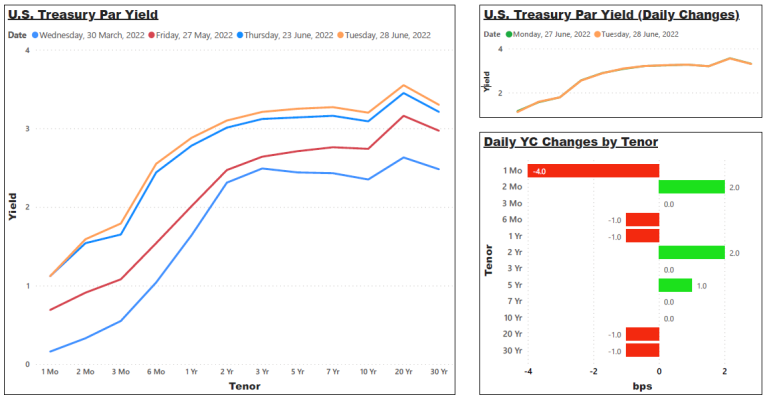

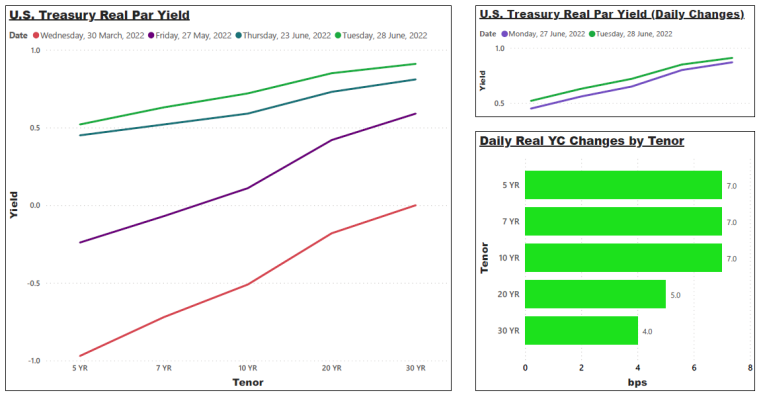

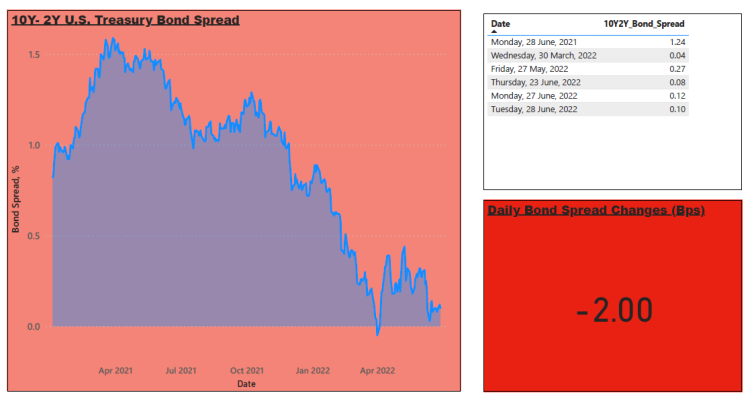

A slight flattening was observed from yesterday's U.S. treasury par yield curve, evident by a 2 bps increase on the 2-month, 2-year and 5-year tenors and a 1 bp drop on the 10-year tenor. As a result, the 10-year - 2-year bond spread has decreased by 2 bps. 5-year, 7-year and 10-year U.S. treasury real par yields were increasing by 7 bps while 7-year and 10-year U.S. treasury nominal par yields were unchanged. As U.S. treasury real par yield was usually priced as treasury par yield minus expected inflation by market convention, a greater increase in U.S. treasury real par yield than its nominal par yield signifies a market expectation of even softer inflation or even a deflation scenario.

(Note: 1 basis point (bp) = 0.01%)

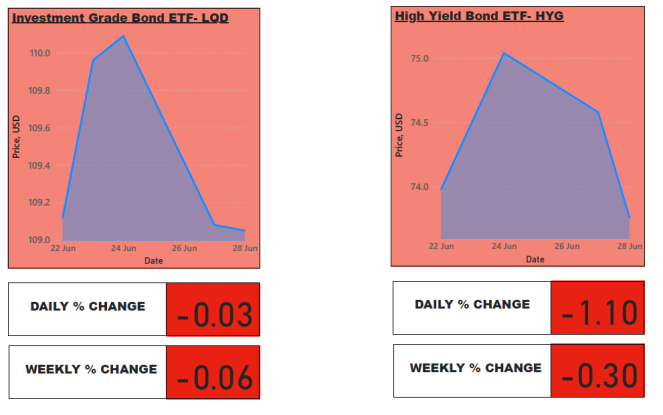

Unlike default-free U.S. treasuries which have government backing, corporate bonds are issued by corporates to finance their day-to-day business operations, hence, subject to the credit risk of missing interest payments or principal default should the credit profile of the bond issuer deteriorates.

2 main components that would impact bond market performances are interest rate decisions by the Federal Reserve (Fed) and the credit profile of the bond issuer.

A hawkish environment (an economic period where there are aggressive rate hikes, e.g. the year 2018) would exert downward pressure on corporate bond prices as borrowing costs are getting more expensive, and investors would prefer to park their money in the safe-haven government securities which now offer a higher yield. On the other hand, if rate hikes are the result of inflationary pressure due to an improving economy, the credit profiles of many bonds issuers are becoming better, hence, this would be positive for the corporate bond prices.

On the other hand, a dovish environment (an economic period where there are aggressive rate cuts, e.g. the year 2020 when there is a Covid-19 outbreak) would exert upward pressure on corporate bond prices as borrowing costs are getting cheaper, and investors would prefer not to park their money in the safe-haven government securities which now offer a very low yield due to rate cuts and would not mind taking some risks on corporate bonds in exchange of higher yield. On the other hand, if rate cuts are the result of an economic recession, the credit profiles of many bond issuers worsen, hence, this would be negative for the corporate bond prices.

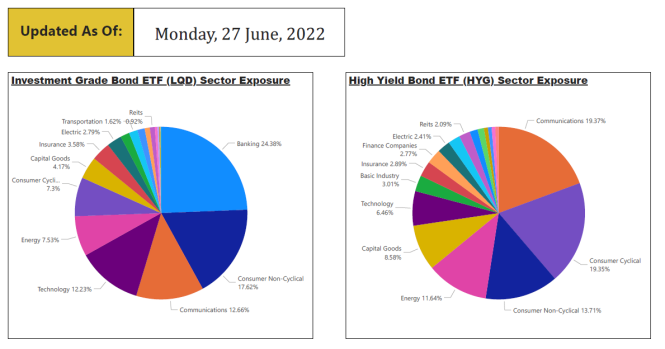

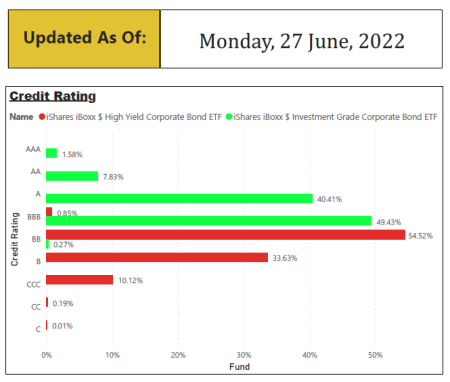

As shown above, the high-yield bond ETF (NYSEARCA: HYG) is exposed to more cyclical sectors and has more exposure to bonds that are rated BBB and below than the investment-grade bond ETF (NYSEARCA: LQD), therefore, subjected to a higher probability of default and hence more sensitive to the credit component. Investment-grade ETF is exposed to more stable sectors and has more exposure to highly rated bonds, hence less sensitive to the credit component but more sensitive to Fed's rate hike decision. When the economy is booming, high-yield bonds would usually outperform investment-grade bonds and the opposite would happen during a recession.

Yesterday's price action (fall in investment-grade bonds, with a greater fall in high-yield bonds) has shown that the bond market is pricing in a scenario where there are aggressive rate hikes amidst an economic recession, as the rate hike decision this time is to combat a supply constraint-induced recession because of sanctions and Russia-Ukraine conflicts which result in a global shortage of energy and food supplies.

Commodities

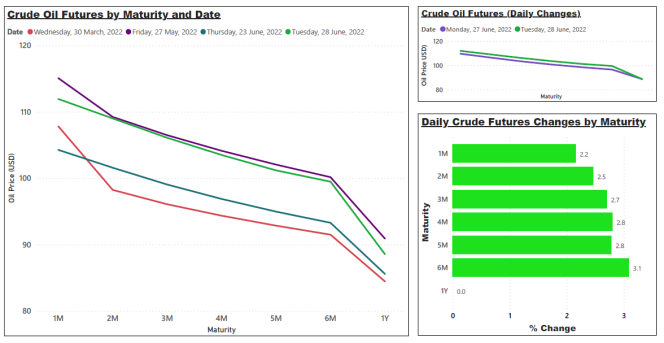

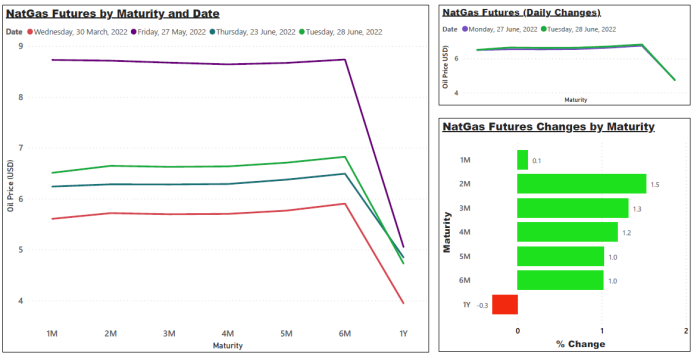

Both crude oil and natural gas futures rebound again for the second day as China cuts quarantine for overseas travelers from 14-21 days to mere 7 days, the very first step taken by China towards its gradual opening. This would undoubtedly increase the possibilities of international travel.

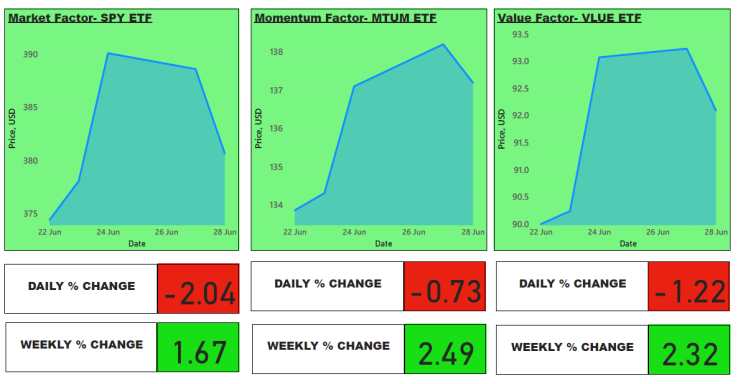

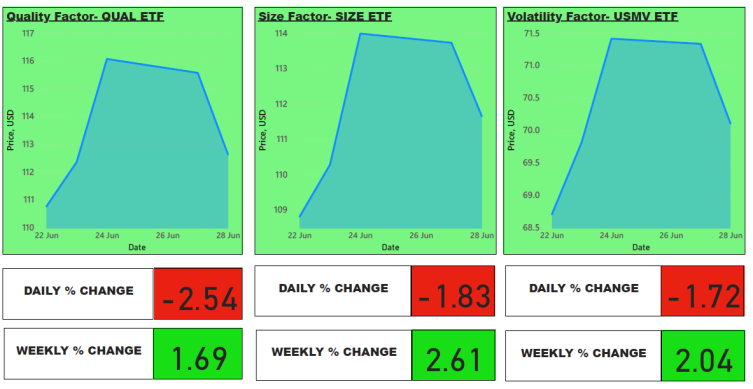

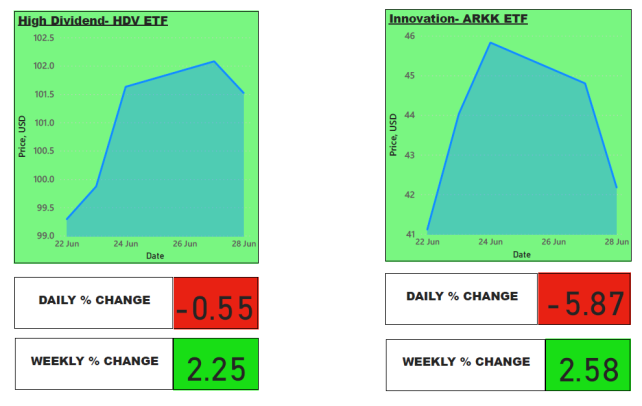

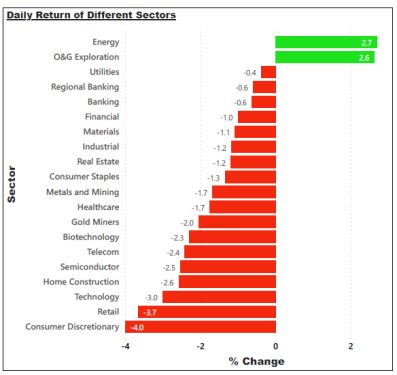

Equities

All factor ETFs and sector ETFs were all down on the release of a disappointing U.S. consumer confidence survey, with

- 29.5% expect business conditions to worsen, up from 26.4%

- 22.0% anticipate fewer jobs, up from 19.5%.

The only exceptions are the energy and oil and gas exploration sectors which benefited from higher energy prices.

Crypto

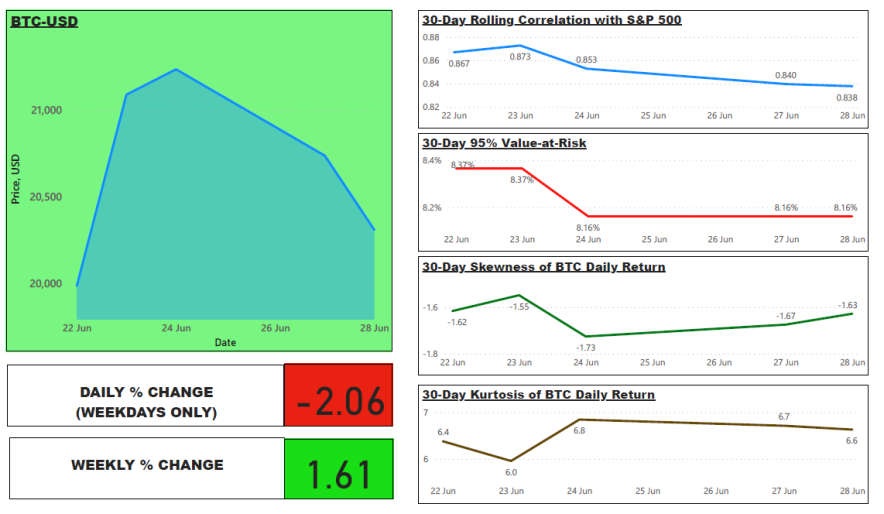

Bitcoin was down 2.06% again yesterday. Although its correlation with S&P 500 index has decreased, it is still not a risk-off asset as its downside risk remains elevated with high values of negative skewness and being fat-tail (indicated by an increased kurtosis value over time).

Voyager Digital (a crypto lender) has just issued a notice of default to Three Arrows Capital, a crypto hedge fund darling last year during the bull run as they have missed the payments on a $670m loan which consists of $350m worth of USDC and 15,250 Bitcoins.

That's it! That's the market updates from me today, happy trading!

Connect with me at:

Reference:

1. Thumbnail image here was downloaded from Unsplash, where credit is given to Mark Basarab, the creator of this photo.

2. https://www.conference-board.org/topics/consumer-confidence

4. https://www.cnbc.com/2022/06/27/three-arrows-capital-crypto-hedge-fund-defaults-on-voyager-loan.html