There are mutterings from some quarters that Bitcoin is a de facto fiat currency. Unfortunate, as most people have very little understanding of what Bitcoin is, many don’t even know what fiat currency is, but to confuse the two deliberately or otherwise is either ignorant or mischievous. Bitcoin may have its faults, but being a fiat currency is not one of them. And to suggest otherwise is suspect.

First, let’s get back to basics. What is money?

A review of monetary principles (by no means the definitive analysis) reminds us that it has always been a system of deferred exchange, whereby suitably practical units, or tokens, are adopted and accepted as intermediary representatives of goods in absentia, to be acquired at a time when necessity dictates. This sensible form of exchange is a socially acceptable method that alleviates the coincidence of wants problem discussed earlier. The tokens require certain properties to be functional (for example they must compensate for the limitations of the goods they are agreed to represent); they must be portable, imperishable, fungible and so on. And it is in this capacity that they are also able to store value. But there is one criterion that they must always be seen to fulfil—they must be seen to reflect in some (possibly arbitrary) way, a measure of effort to acquire, comparable to that which they are traded. It therefore follows that for the practice to work, such a token cannot be passed off with a counterfeit substitute whose acquisition requires far less comparable effort.

Bitcoin: How Can a Virtual Currency Attain Real Market Value?

And now a reminder that fiat currency is legal tender issued by a government, its printed notes having no intrinsic worth other than being counterfeit resistant. Unlike representative money, fiat cannot be redeemed for its equivalent worth in a commodity such as gold or oil, for example, but instead derives value through supply and demand and the stability of the issuing government. Its strength is dependent on the national economy, fiscal policies and government credit; its adoption as a functioning medium of exchange is dependent on the trust in this strength, as a matter of faith.

Fiat is Latin for “let it be done” or “it shall be” or as Captain Picard would say, “Make it so.” It is a decree that its issued denominations in currency is legal tender and must be accepted for the settling of debt, both public and private. And it does enjoy some advantages over representative money in that a certain degree of economic volatility during a crisis can in theory be ‘ironed out’ via various instruments not available to a less flexible representative monetary system such as the gold standard of the 20th century. It has even been suggested that a fiat monetary system if in operation at the time would have mitigated the Great Depression.

The gold standard, whereby the dollar value of gold is fixed and technically redeemable in gold ounces from the vaults of the Federal Reserve, was completely abandoned in 1971 due to the price stability vital to a healthy economy being beholden to the vagaries of supply and the fluctuating price of gold.

Once the dollar no longer represented the gold value that kept it ‘honest’, governments had licence to ‘print money’ via such dubious methods as debt monetisation (issuing and selling government bonds to the central bank) and quantitative easing (buying financial assets on the open market and providing banks with liquidity to stimulate lending and investment). Once the government ditched the gold standard it could really let rip; it could play the marvellous prestidigitator, plucking coins from thin air and tossing them to an eager audience.

What could possibly go wrong?

Emerging around the time of the financial crisis of 2008, and due to the timing, Bitcoin is often misrepresented as a reflexive response to the abuses and mismanagement of fiat currency that contributed directly to the economic meltdown. But it was more likely the completion of an evolving project to address the innate flaws of government printed money happened to coincide with the dramatic economic meltdown. Satoshi Nakamoto, the pseudonymous developer of Bitcoin, put it like this: “The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust.”

Bitcoin was designed to address these limitations and offer a functioning alternative to fiat as a means of storing and exchanging value whilst avoiding the need for trust in a central authority to distribute money and legitimise transactions. However, the magic bullet came at a cost. Specifically, the new consensus mechanism which governs the Bitcoin ledger came at a cost in joules that simply couldn’t be magicked away. Many would say that cost is too high to the environment. And we need to bear that in mind.

Sending and receiving denominations of digital currency peer-to-peer isn’t hypothetically any more costly than sending email. You put some effort into constructing your email and send it off. It isn’t a big deal. Nor is sending off hundreds or thousands of the exact same email. That’s the problem: for a decentralised digital medium of exchange network to work there needs to be a transactional cost involved to deter spam, to deter multiple attempts to send the same counterfeit coin and debase the currency. And that’s where the proof-of-work consensus mechanism peculiar to Bitcoin comes in to play. This is the protocol which every transaction must undergo in order for it to be validated by the network and added to the overall blockchain of transactions that make up the distributed ledger.

What is proof-of-work?

Let’s use an analogy: imagine a Rubik’s Cube competition where each contestant is presented with an identically jumbled cube. When the clock starts they each attempt to solve it systematically without using an algorithmic strategy to cut time—the only advantage being the speed at which each possible combination can be tried—and the winner receives a reward of 50 coins. Now imagine that every time a Bitcoin is sent to a recipient it has to undergo something like this process—actually, a cryptographic hash function commonly referred to as mining—for the transaction to be validated by the network. And that gives you some idea of the computational resources consumed to maintain the Bitcoin network.

Even as far back as 2014, the Bitcoin network consumed as much electricity as the whole of Ireland; by 2019, the Philippines; by 2025 … you get the picture. Satoshi claimed that “if [Bitcoin] did grow to consume significant energy, I think it would still be less wasteful than the labor and resource intensive conventional banking activity it would replace. The cost would be an order of magnitude less than the billions in banking fees that pay for all those brick and mortar buildings, skyscrapers and junk mail credit card offers.”

Depending upon the parameters used to calculate the entire energy consumption of the financial industry (not just the computer servers), a recent statistical model suggests Satoshi is incorrect and that the Bitcoin network is actually more energy intensive relatively speaking, but closing the gap.

So is Bitcoin a fiat currency?

Well, it would have to be a human institution first. No one can simply issue it and pretend it is legal tender; that would require an authority. Bitcoin has no central authority invested with the necessary power to ensure its adoption and it transcends all jurisdictions regardless of their involvement. That's because it is programmed to behave like commodity money and cannot deviate from its intended function. So long as the code holds up, or isn’t radically altered or compromised, or processers take a quantum leap, it cannot do otherwise. And like any commodity, there is demonstrable effort involved in its acquisition (think back to the Rubik’s Cube); there is guaranteed scarcity as Bitcoin circulation is limited to 21 million; and the reward for solving the cryptographic hash function (mining) is reduced by half every four years until there are no more rewards to claim. Also, the difficulty of the hash function is adjusted fortnightly to account for increases and decreases in the collective processing power devoted to mining in order to keep transaction time to approximately 10 minutes, to guarantee a predictable quantity of coins minted, and guard against inflation. Increasing the difficulty of the hash function would be like adding extra squares to each face of a Rubik’s cube, so instead of 3x3 it becomes 4x4 and vice versa.

OK, does Bitcoin have inherent value?

Although people don’t often consider it as such, it can be helpful to understand Bitcoin as the means of converting electricity in terms of joules and watts into a store of value and digital unit of exchange. In other words, Bitcoin converts electricity into the modern digital equivalent of conventional money (the fundamental principles of which have been outlined above). And, importantly, despite what people say, it retains some essence of the use value of electricity in terms of the social utility it now provides as digital currency. So it is misleading to suggest that Bitcoin doesn’t have innate value simply because it isn’t a physical commodity or obviously ‘backed’ by a tangible commodity. No one who follows the Bitcoin market can argue that its price might seem to distort this value, wildly at times, but it still preserves a degree of value from the electricity it converts.

This concept is nothing new, the economist Maynard Keynes mooted the possibility over a century ago around 1913: “Mr H. G. Wells’s view that ‘the problems of economic theory will have undergone an enormous clarification’ if instead of measuring money in fluctuating gold standards, they were measured in units of electrical energy.” (This would be the science-fiction author H. G. Wells who wrote War of the Worlds and other classics of the genre.) What’s more, in 1921 Henry Ford suggested replacing gold with an ‘energy currency’ to stop wars.

It is doubtful that Satoshi had this specifically in mind when coding the protocols in 2008, but that’s kind of what is happening, although assuming its mass adoption will inevitably lead to a reduction in war is probably a stretch. But we do find ourselves in a unique position whereby Bitcoin appears to create arbitrage opportunities. Arbitrage is the process of purchasing an asset (or any product) from one market and selling in to another for a profit made possible by discrepancies of price between the two markets, whether as a result of inefficiencies, information disparities or regulatory differences between the two markets, or any other reason. Speed of execution is important as the window of opportunity slams shut quickly. Theoretically, arbitrage corrects the price disparities between markets so that they eventually converge—the law of one price.

Arbitrage has applications in the local electrical market with the utilisation of battery storage. Companies can buy cheaper electricity off-peak, store it in batteries and sell it back at a higher price during peak demand. Bitcoin arbitrage is also much discussed and the imperative to locate mining operations in areas with low electricity prices such as West Texas or China. But is that arbitrage in the strict sense of the term, and can Bitcoin be utilised as a means of arbitraging the energy market per se?

Can Bitcoin open a trading route between isolated energy markets?

If a natural gas producer in West Texas is trying to sell electricity into their regional pool at the same time that the wind is blowing and the sun is shining across the state, the value for their unit of energy can actually go negative. This means that they would have to pay someone to take their energy. At the very same point in time, someone charging their electric car in California may be paying a peak-demand surcharge for electricity that doubles their cost of energy. The Californian Tesla owner would very much love to have cheaper energy from Texas and the Texas producer would love to charge even a few cents for their power to anyone that would buy it. Unfortunately, these two energy pools operate in isolation. You can’t move a joule of energy from the Texas pool to the California pool without a lot of government paperwork and transportation costs. The arbitrage opportunity can’t be realised.

The Joule Paradox: Energy Sets the Value of Bitcoin and Bitcoin Sets the Value of Energy

Is the Bitcoin network the medium through which the supply and demand differential between two discrete regional energy markets can be satisfied, even to the point of economic equilibrium? Is there an opportunity for the miraculous intervention of Adam Smith’s so-called invisible hand to optimise energy prices across regions in accordance with the law of one price?

For a straightforward arbitrage to work for the above example, a miner would have to mine BTC in West Texas (which is effectively buying cheap electricity and converting/storing it as BTC) and then sell it in California. But BTC can’t be converted to electricity as simply as electricity is converted to Bitcoin. Sure, it can be used to buy electricity in California, but that isn’t exactly fulfilling the fundamentals of arbitrage because a sale needs be executed, surely.

What if the aforementioned BTC was sold exclusively to (or actually mined by) the Pacific Gas & Electric Company (PG&E), for example, and they bought electricity from a different supplier in BTC and sold it on. Perhaps something along those lines would fulfil the criteria of a classic arbitrage trade. Or maybe it is even simpler, if less direct, if we view the operation on a global scale. That is, if we view it as essentially ‘buying’ cheaper electricity from the local market, say from West Texas, and just selling the BTC on the global market, so that the consumer in California has the option to trade their BTC for electricity.

By simply plugging in a mining machine and connecting it to the internet, you can now sell your electricity to an always willing buyer. These two simple pieces of technology allow for energy pools to be linked in a way that hasn’t really existed before.

The Joule Paradox: Energy Sets the Value of Bitcoin and Bitcoin Sets the Value of Energy

But would this ultimately narrow the price margins between regional electricity markets once the operation is sufficiently scaled? Would the law of one price inevitably kick in over time? That remains to be seen, and there is no obvious evidence that this is yet the case.

In thinking about the relationship between bitcoin and energy within this paradox we start to see why the proof-of-work model that Satoshi chose to implement and the system of automated market regulation through the difficulty adjustment is so genius. If either of these features was missing from bitcoin then we would not have the highly valuable asset that we have today. It all comes back to this simple realisation, energy is the fundamental, base commodity upon which everything of value is produced and bitcoin is the most pure embodiment of energy in a monetary form. If we took the energy out of bitcoin then bitcoin would be no better than any other fiat system of money. By acting as the real-time marketplace for internet-enabled energy, the bitcoin network allows us to complete the Joule Paradox: energy sets the value of bitcoin and bitcoin sets the value of energy.

The Joule Paradox: Energy Sets the Value of Bitcoin and Bitcoin Sets the Value of Energy

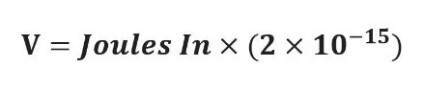

And finally, are there formulae to definitively establish the mathematical relationship between Bitcoin value and joules?

There are various formulae that claim to calculate a ‘fair value’ for Bitcoin. This is one such example:

Bitcoin Energy-Value Equivalence:

A Fair Value for Bitcoin

The hypothesis:

Bitcoin’s fair value is a function of energy input, supply growth rate and a constant representing the fiat dollar value of energy.

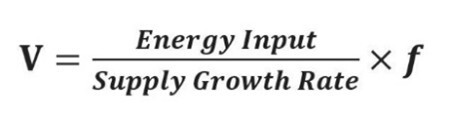

These variables can be combined into the following equation, termed Bitcoin’s Energy Value (V):

The Energy Value Formula

Where:

- Energy Input (unit: Watts) = Hash Rate (GH/s) * Mining Energy Efficiency (J/GH)

- Supply Growth Rate (unit: s-1) = Annual increase in circulating Bitcoins, equivalent to the inverse of Stock-to-Flow. Calculated as the annual rate (unit: year-1) of change in circulating Bitcoins and then converted to seconds

- Fiat Factor ($USD/Joule) = A constant conversion factor to allow for the fiat USD value of energy

As all units of hash rate and supply rate cancel out, this equation suggests that the fair value of Bitcoin (V) can be represented as a function of the Joules of energy spent to produce it:

The Energy Value Formula: Bitcoin’s fair value is a function of Joules

On March 6, 2024 the formula calculated a value of $70,000, and the actual price high for that day was $66,000. We might be cherry-picking here, but that’s close for that given day using the valuing model above. Remember, though, price and value are not the same thing:

Notice that I said value and not price. An old friend of mine used to frequently say that price is what you pay and value is what you get. The same is true here. The value of a bitcoin is based upon the energy inputs and production costs but the market determines the price. Similarly, bitcoin determines what the minimum value for a unit of electricity is but the seller determines whether they will accept that price or sell to someone else for more ... Energy is the true source of value and no other monetary system is built on energy.

The Joule Paradox: Energy Sets the Value of Bitcoin and Bitcoin Sets the Value of Energy

All the other crypto/altcoins with differing consensus mechanisms may appear environmentally friendlier, but without actual proof-of-work aren’t they really, despite their distinctive protocols, just variables measured in Satoshis (denominations of Bitcoin)? Bitcoin undergirds the entire industry such that a departure from the proof-of-work protocol, however tempting, may prove catastrophic to the entire enterprise.

Conclusion

Bitcoin is an energy currency not a fiat currency; it has inherent value, like gold, in so far as it has the capacity to store value and be exchanged through a robust and secure network so long as the infrastructure is sound and society has such a need for an independent system exchanging digital currency.

Some would argue it presents a socially valuable energy arbitrage opportunity.

And some Bitcoin maximalists and disciples of Ford may even argue, along with Henry Ford were he alive, that within its code is the invaluable means to end all war.