You are reading an excerpt from our free but shortened abridged report! While still packed with incredible research and data, for just $20/month you can upgrade to our FULL library of 50+ reports (including this one) and complete industry-leading analysis on the top crypto assets.

Becoming a Premium member means enjoying all the perks of a Basic membership PLUS:

- Full-length CORE Reports: More technical, in-depth research, actionable insights, and potential market alpha for serious crypto users

- Early access to future CORE ratings: Being early is sometimes just as important as being right!

- Premium Member CORE+ Reports: Coverage on the top issues pertaining to crypto users like bridge security, layer two solutions, DeFi plays, and more

- CORE report Audio playback: Don’t want to read? No problem! Listen on the go.

Maker RWAs

At its core, Maker's RWA initiative aims to further diversify the protocol's collateral in order to minimize risk and hedge against DAI's reliance on USDC (USDC makes up more than half of DAI's collateral). Initiative proponents emphasize the significance of RWA in expanding the scope of DAI, enhancing its stability, and increasing its decentralization.

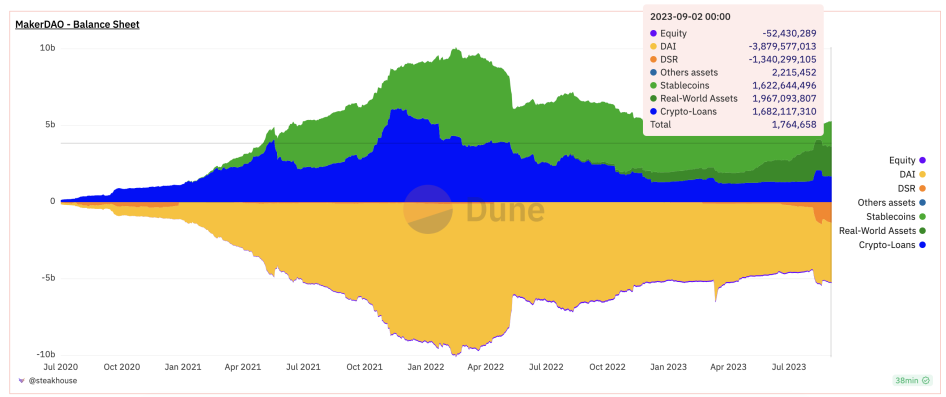

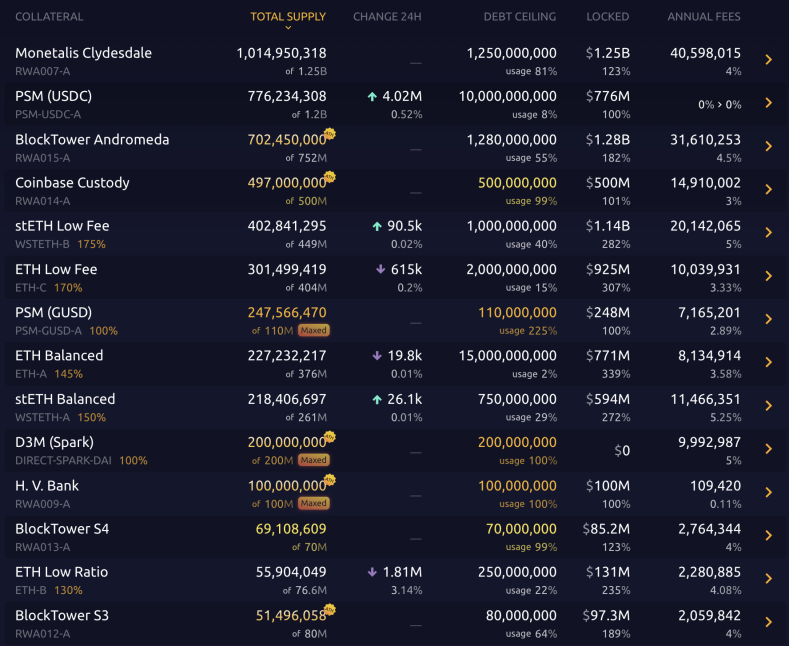

Collateralization using Real World Assets (RWA) within MakerDAO has seen a remarkable uptick. From August 2022 through Q2 2023, DAI backed by RWA within MakerDAO experienced exponential growth. This meteoric rise can be attributed to strategic collaborations with entities such as Monetalis Clydesdale, Huntingdon Valley Bank, and BlockTower. Within the partnership framework of Monetalis Clydesdale, MakerDAO has the opportunity to allocate its dormant PSM USDC towards liquid bonds, thus optimizing the use of idle assets.

MakerDAO, a decentralized finance (DeFi) powerhouse, has been a prominent player in the real-world asset (RWA) arena, with $3.4 billion of its collateral base represented by RWAs, predominantly U.S. treasuries. This move has proven to be lucrative for Maker as RWA-related fees accounted for ~66% of the total fees generated up until July 2023. Despite the growing influence of centralized forces, which has often been a point of contention, the integration of RWAs into Maker’s portfolio has been a valuable addition. While the majority of Maker's exposure is towards assets considered 'risk-free', the platform has also ventured into other asset classes, albeit on a smaller scale, which carry default risks.

Traditional finance addresses defaults through various means, including selling distressed loans at discounted rates, undergoing financial restructuring, or initiating liquidation processes. However, when the recoverable value is negligible or a lender is too junior to receive any recovery versus what is available for distribution, the recovery is usually nil. Additionally, several external factors, such as legal claims, environmental issues, insufficient insurance, or intellectual property disputes, can also affect the token's value.

Challenges Faced by MakerDAO

Recently, MakerDAO encountered a default on one of their RWA loans, a tokenized loan facilitated through Centrifuge in a pool underwritten by ConsolFreight, a trade finance provider. The pool consisted of $2.7 million in loans, with the largest borrower having an outstanding balance of $1.84 million. ConsolFreight was responsible for originating the loans, while Centrifuge Tinlake's infrastructure financed the assets, and MakerDAO, along with other DeFi participants, acted as the lenders. A previous default occurred in April involving a 1.5 million DAI loan under the Harbor Trade pool.

Defaults are not inherently problematic unless they constitute a large portion of a broader portfolio. Effective risk management involves accepting that defaults are inevitable and ensuring that the default risk is acceptable relative to the portfolio and that there is a reasonable estimate of recoveries in the event of a default. However, the crypto space presents additional risk as the legal backing for crypto lenders/investors has not been thoroughly tested. Although the defaulted loans are relatively small compared to Maker's collateral base and do not pose a significant financial risk even if no capital is recovered, the handling of the situation could have long-term implications for managing investments and risks in more impactful scenarios.

Conclusion

The incorporation of RWAs into DeFi protocols like MakerDAO has undeniably been beneficial, as evidenced by the substantial fees generated from RWAs. However, the recent defaults highlight the challenges and uncertainties associated with managing real-world assets in the crypto space. While defaults are a part of any lending operation, the crypto world presents unique challenges related to legal enforcement and the management of investments and risks. As the DeFi space continues to evolve and interact with traditional finance, it is crucial to develop robust strategies and frameworks to address these challenges and minimize their impact on the broader ecosystem.

DAI

From the origination of the Maker project, the first iteration of Dai was known as Single Collateral Dai (SCD) because it had only one asset serving as collateral, Ether. SCD was launched in December 2017 and served as the only widespread stablecoin alternative to the “usual” company-backed stablecoin projects like USDT and USDC. Dai’s decentralized, permissionless features allowed it to become an integral piece of the Decentralized Finance (DeFi) ecosystem, the industry that seeks to build decentralized financial products on top of smart contract-enabled blockchains, eliminating middlemen and rent-seeking entities.

In November 2019, MakerDAO upgraded the protocol to transition from Single Collateral Dai (SCD) to Multi Collateral Dai (MCD) by adding Basic Attention Token (BAT) as additional collateral outside of just Ether. Since then, Maker has added more custodial/less decentralized assets like USDC, WBTC, TUSD, PAX, and USDT.

The collateralization of stablecoin plays a crucial role in securing a significant portion of circulating DAI. A unique innovation in this regard is the Peg Stability Modules (PSM), which are specialized vaults that hold USD stablecoin as collateral. With a 100% collateralization ratio and an interest rate of 0%, assets in these PSM vaults can be exchanged on a 1:1 ratio for DAI.

MakerDAO’s commitment to transparency is evident from the public availability of its DAI collateral list. The organization issues monthly RWA reports, providing detailed commentary for each vault. This level of accessibility allows anyone to dive deep into reports, dashboards, and proposals to verify MakerDAO’s real-world asset exposure, setting a standard that traditional finance could learn from. Although DAI is the largest RWA-backed CDP stablecoin managed by a Decentralized Autonomous Organization (DAO), it is not the only one utilizing RWA collateral. Centralized stablecoins, such as USDC and USDT, also diversify their collateral into various assets. For example, Circle’s reserve fund assets include US Treasury securities and repurchase agreements, while Tether’s reserves contain US Treasury Bills, money market funds, gold, and repurchase agreements.

In summary, the integration of real-world assets as collateral in the crypto landscape, as demonstrated by MakerDAO’s DAI, represents a significant advancement in the world of decentralized finance. The transparency and accessibility of information provided by MakerDAO serve as a benchmark for the industry. Moreover, the diversification of collateral into various assets by centralized stablecoins like USDC and USDT indicates the growing recognition of the importance of real-world assets in the crypto economy.