You are reading an excerpt from our free but shortened abridged report! While still packed with incredible research and data, for just $20/month you can upgrade to our FULL library of 50+ reports (including this one) and complete industry-leading analysis on the top crypto assets.

Becoming a Premium member means enjoying all the perks of a Basic membership PLUS:

- Full-length CORE Reports: More technical, in-depth research, actionable insights, and potential market alpha for serious crypto users

- Early access to future CORE ratings: Being early is sometimes just as important as being right!

- Premium Member CORE+ Reports: Coverage on the top issues pertaining to crypto users like bridge security, layer two solutions, DeFi plays, and more

- CORE report Audio playback: Don’t want to read? No problem! Listen on the go.

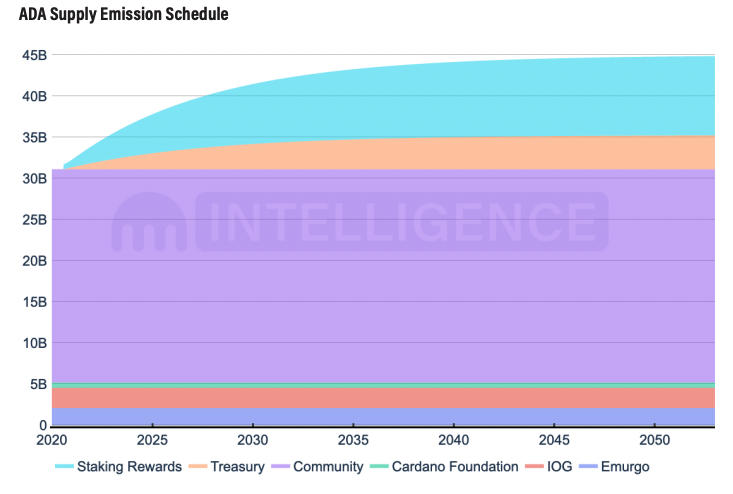

Cardano had an initial supply of 31.1 billion ADA. ADA tokens have a capped supply of 45 billion. The current ADA circulating supply as of Q1 2022 is ~34.6 billion, leaving the remaining 10.5 billion for network incentives.

Staking rewards from the reserve were not available to be issued until after the Shelley hard fork in July 2020. The reserve is depleted at a rate of 0.3% per epoch (every ~five days). This means it will take ~5 years to decrease the reserve supply by 50%.

The split among reserve reward distributions are as follows: the majority (80%) of the rewards are allocated to staking pools and delegators, while the remaining 20% is allocated to the treasury.

Source: Kraken

Source: Kraken

Staking

With the launch of staking in July 2020, there were ~13.8 billion ADA reserved as stake incentives for participants. Every epoch (5 days), the protocol distributes 0.3% of this total reserve pool between all active stakers, which amounts to 41 million ADA. Therefore, rewards are distributed every five days and compounded automatically.

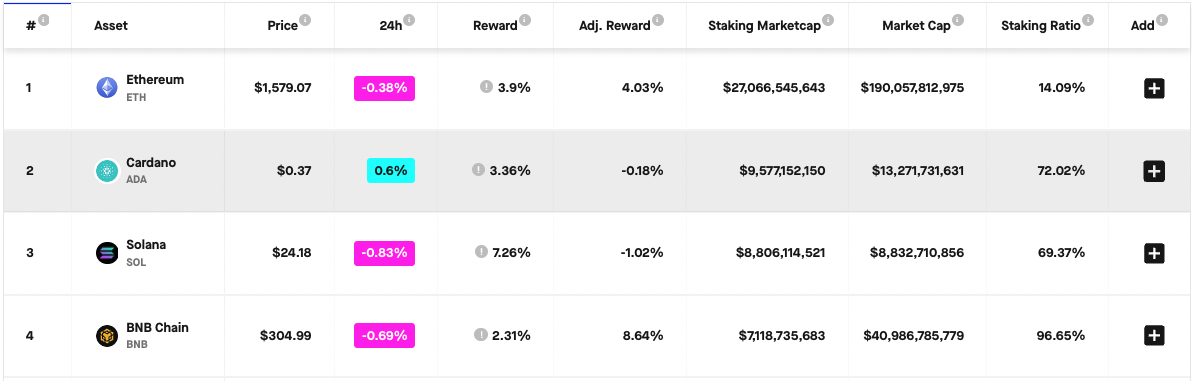

As of Q1 2023, there are currently ~3220 active pools with ~25 billion ADA being staked. This represents ~72% of the circulating supply.ADA fares well in other categories when compared to other staking chains, too (image below). Pool operators set their own fees and profit margins, but on average, the return is ~4% APY.

Users’ earnings are dependent on several network parameters, such as the number of tokens participating in staking and the individual configurations of the staking pool being used. Staking incentives within the Cardano network are designed to prevent the formation of large, concentrated pools. To prevent this, the network sets diminishing rewards once a pool has reached "saturation," i.e., a large size determined by the network.

In most PoS protocols, delegators must lock up their staked funds, making them inaccessible while they are staked. When a delegator wishes to unstake, the funds muster undergo an unbonding period, during which they remain locked and do not accrue rewards. These periods can range from several days to several weeks.

In contrast, Cardano's delegation mechanism is designed to be liquid and flexible, in which funds are never locked and no unbonding period is imposed on delegators. The implementation of unbonding periods in other protocols may be technically justified, but from the perspective of delegators, they are inconvenient and impose an opportunity cost. This can discourage network participants from changing their delegation, which is often done to increase rewards and reduce the risk of stake concentration among a small number of groups or stake pools.

In terms of liquidity, locked funds and unbonding periods can deter participation in staking, as holders often prefer to keep a portion of their funds liquid for trading, decentralized finance (DeFi), and non-fungible token (NFT) transactions. If staked funds are liquid, one would expect participation rates to be higher as seen with Cardano, as well as, the recent rise in liquid staking derivatives (LSDs) on Ethereum and other chains.

ADA fares well in most staking categories when compared to other PoS chains but suffers in adoption metrics like transactions and users. This is illustrative that Cardano, as it exists today, is (essentially) not used for smart contracts, DeFi, or transactions but simply a circular economy of staking until more practical use cases can manifest.

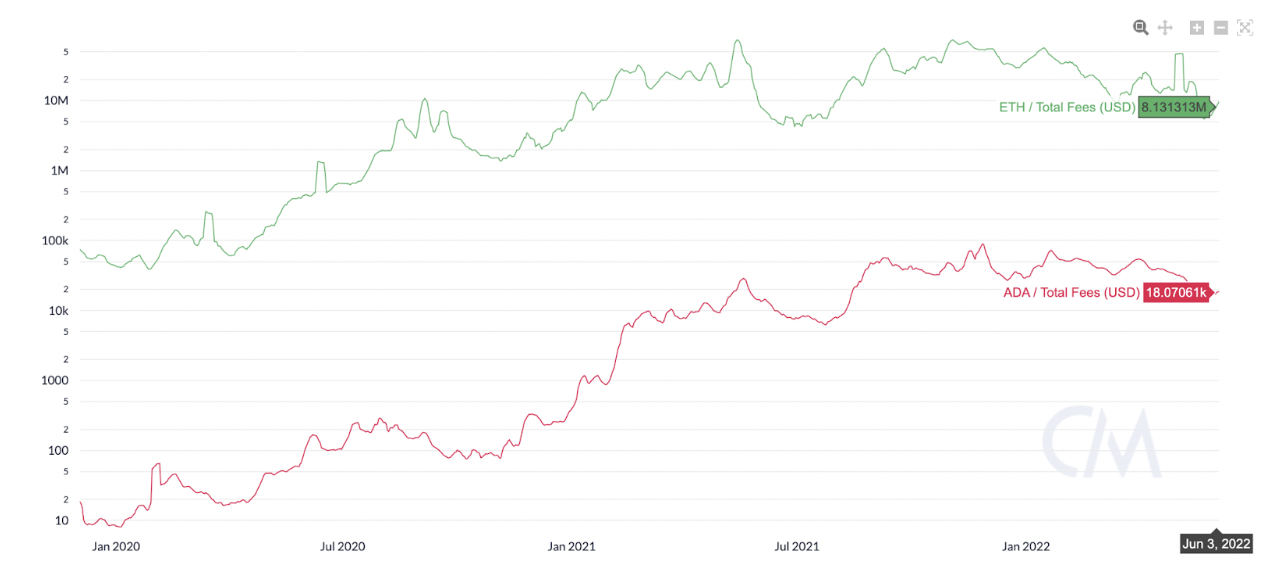

Total Fees Generated on the Cardano Network vs. the Ethereum Network. Source: CoinMetrics

Total Fees Generated on the Cardano Network vs. the Ethereum Network. Source: CoinMetrics

On a positive note, ADA staking is above average when it comes to its peers and the decentralization of its stake. As the image below illustrates, solo stakes are the largest cohort of stakers followed by Binance at ~11%.