If you want more cryptocurrency analysis including full-length research reports, trading signals, and social media sentiment analysis, use the code "Publish0x" when subscribing to CryptoEQ.io to make your first month of CryptoEQ just $10! Or simply click the button above!

UNI Strengths

- One of the top Ethereum dApps by nearly any metric: users, volume, TVL, revenue, etc.

- One of the few truly permissionless, decentralized, and unstoppable protocols with no backdoor vulnerabilities in DeFi

- Impressive team with a stellar record of continually improving the product and shipping new versions (V1 vs V2 vs V3)

- Anyone is able to create a market on Uniswap allowing it to list long tail ERC-20 assets long before centralized exchanges are able

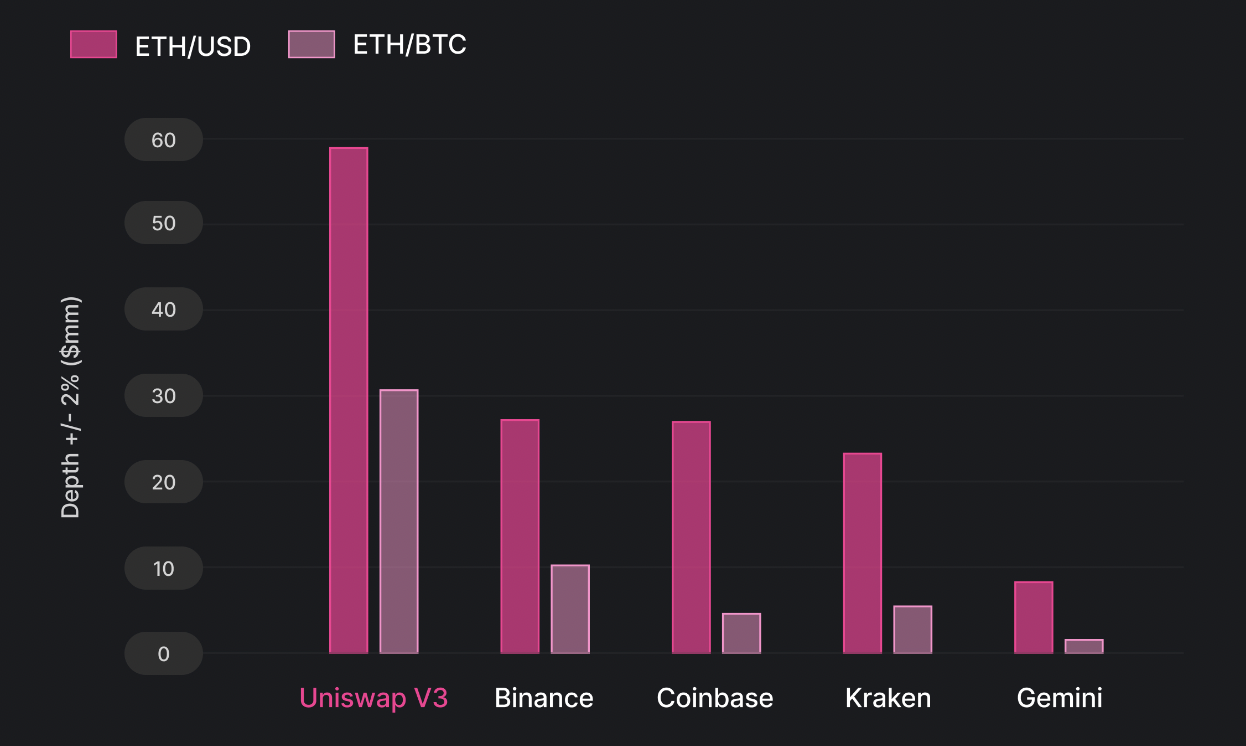

- V3 regularly has more liquidity in ETH/USD, ETH/BTC and other ETH pairs compared to centralized exchanges.

UNI Weaknesses

- UNI token is solely a governance token and does not accrue fees generated by the protocol.

- Uniswap and DEXs, in general, can be copied/knocked off (SushiSwap and PancakeSwap) due to their open-source nature, losing market share.

- Traders may suffer impermanent loss when providing liquidity to Uniswap, deterring a portion of potential users. A report by Topaze Blue and Bancor Protocol found that 49.5% of liquidity providers on Uniswap V3 have incurred losses from impermanent loss.

- Uniswap only trades Ethereum ERC-20 tokens and future cross-chain DEXs like Thorchain and Gravity DEX (Cosmos) may interest more traders looking to trade across blockchains.

Uniswap V3

There are two significant differences that V3 introduces in its design: concentrated liquidity and multiple fee tiers. On Uniswap V2, users provide liquidity evenly along all of its markets’ price curves. This is somewhat inefficient since there does not need to be equal amounts of liquidity for ETH at $1 vs $2500. The concentrated liquidity gives individual liquidity pools control over what price range their funds are allocated to. This allows for individual positions to be fused together into a single pool to make one combined curve for traders to trade against. Liquidity pools can focus capital within a custom price range so pools can provide larger amounts of liquidity at desired prices. This mechanism allows for individualized price curves. In doing so, traders can trade against the combined liquidity pool of all curves with no gas increase per liquidity provider. Trading fees are then collected and dispersed at a given range appropriately.

Multiple fee tiers allow for liquidity pools to be compensated for taking risks. There are three fee tiers per pair: 0.05%, 0.30%, and 1%. These options make sure that liquidity pools are customized to their margins according to certain pair volatility of the tokens. This may lead to some liquidity fragmentation, but the Uniswap team believes that most pairs will calibrate to an appropriate fee tier. Uniswap expects liquidity pools to take more risk on non-correlated pairs like ETH/DAI and to take on less risk in correlated pairs like USDC/DAI. Correlated pairs are expected to sit at around 0.05% fees and .30% fees for pairs like ETH/DAI. 1% swap fees will be more appropriate for riskier pairs. Fees in V3 are more flexible and can be turned on by governance for each pool; these fees can be between 10% and 25% of liquidity pools fees.

In Q3 2021, after months of anticipation, Uniswap launched Optimism, a layer 2 (L2) scaling solution for Ethereum with six assets. Transactions on Optimism are (practically) instant and ~90% cheaper than on the Ethereum mainchain. Since then, V3 is now live on Arbitrum (L2) and Polygon (L1 sidechain) scaling solutions. The Uniswap team expects cross-chain experiences to be a large catalyst for growth and improvement in the user experience. More bridges will be developed and or updated to support bridging governance actions from Ethereum Mainnet.

UNI V3 usage on Ethereum mainnet (left) vs Optimism (right). Source

UNI V3 usage on Ethereum mainnet (left) vs Optimism (right). Source

Liquidity Providers (LPs) will also benefit from the price reduction. The cost associated with withdrawing funds from the pool has gone from $20+ to nearly free on Optimism. This, in turn, opens up the LP market to more retail users and potentially makes it more profitable for even the smallest LPs.

Decentralized exchanges (DEXs), not just Uniswap, have seen enormous growth from 2019 onward. In 2022, they now process 10% of what centralized exchanges (CEXs) process in terms of the number of transactions as opposed to just < 1% two years ago. Uniswap, between v2 and v3, makes up for approximately 50-60% of all trading volume on DEXs.

The V3 upgrade also introduces more characteristics to make Uniswap one of the most flexible and efficient automatic market markers in this space. The liquidity pools can give liquidity with up to 4000x capital efficiency relative to Uniswap V2 so providers can earn higher returns. By concentrating liquidity, users can acquire the same increases as V2 within a certain price range while putting down less principal. V3 also offers a way for low slippage trade execution compared to centralized exchanges and stablecoin AMMs. In order to help protect pool providers, changes were made to increase exposure to preferred assets and to reduce the risk taken. V3 liquidity pools can sell one asset for another by adding liquidity to a price range above or below the market price as needed.

Note: The figure shows the daily average +/- 2% spot market depth in $millions for the sample period from June 2021 to March 2022 for ETH/USD and February 2022 to March 2022 for ETH/BTC. Source

Note: The figure shows the daily average +/- 2% spot market depth in $millions for the sample period from June 2021 to March 2022 for ETH/USD and February 2022 to March 2022 for ETH/BTC. Source

In addition to the greater capital efficiency, v3 also boasts lower fee pairs which bring in users. This can be seen in the USDC/ETH 0.05% pool, which has the highest volume throughout Q3 2022. With the launch of Uniswap on L2s, total fees incurred to trade could even further decrease from 0.05%. As fees decrease, trading volumes on L2s are expected to rise. This is the positive feedback loop Uniswap is looking to ignite: lower trading costs attract more users, increasing LP returns, which drives more liquidity and lower costs.

Another new feature in V3 is that liquidity providers receive non-fungible tokens (NFTs) that represent their Uniswap V3 liquidity positions. In Uniswap V1 and V2, users receive fungible ERC-20 tokens representing their liquidity position in the pool. The reason for issuing NFTs is explained in the V3 mainnet post:

“The pool interface now supports the creation of Uniswap v3 positions with multiple fee tiers and concentrated liquidity ranges. Each position is represented as an NFT and comes with a unique piece of on-chain generative art.”

Uniswap V3 is now the dominant DEX, however, it now also has greater complexity than its predecessors. The downside of increased complexity is that liquidity mining now requires somewhat advanced technical skills. V3 was released a year after V2 and its main goal was on increasing capital efficiency via concentrated liquidity. With the introduction of concentrated liquidity, the liquidity providers can specify a price range for which they would like to provide liquidity and adjust this range based on current market supply and demand. Liquidity providers are compensated with more fee revenue for “actively” managing their positions. This keeps the Uniswap AMM highly capital-efficient but requires active management i.e. constant oversight. Because of this, V3 is seen as a tool for more sophisticated and advanced users. This is also supported by the average transaction size in V3. It is ~30x higher than that in V2!

The high average transaction on V3 can also be attributed to the protocol’s higher market depth across all price levels. This makes it advantageous for users to execute larger trades on Uniswap v3 relative to centralized exchanges because the ultimate price for the transactions is cheaper.