You are reading an excerpt from our free but shortened abridged report! While still packed with incredible research and data, for just $20/month you can upgrade to our FULL library of 50+ reports (including this one) and complete industry-leading analysis on the top crypto assets.

Becoming a Premium member means enjoying all the perks of a Basic membership PLUS:

- Full-length CORE Reports: More technical, in-depth research, actionable insights, and potential market alpha for serious crypto users

- Early access to future CORE ratings: Being early is sometimes just as important as being right!

- Premium Member CORE+ Reports: Coverage on the top issues pertaining to crypto users like bridge security, layer two solutions, DeFi plays, and more

- CORE report Audio playback: Don’t want to read? No problem! Listen on the go.

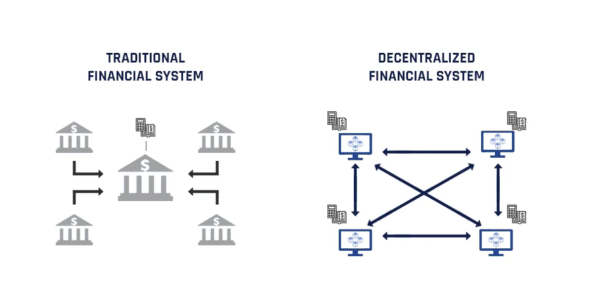

TradFi vs. DeFi

Traditional finance (TradFi) was established based on lending and borrowing practices, forming the backbone of economic growth and financial stability for generations. In recent years, however, significant technological advancements have allowed decentralized finance (DeFi) to rise, emerging as a transformative take on finance through the permissionless and trustless nature of blockchain ledgers.

TradFi revolves around the essential roles of banks and financial institutions as intermediaries. They facilitate the movement of funds and engage in the critical task of assessing borrower's creditworthiness. Market conditions, central bank policies, and macroeconomic factors dynamically influence interest rates in TradFi. They are integral to the symbiotic relationship between lenders seeking returns and borrowers needing capital.

DeFi, led by protocols like Aave, disrupts this traditional model by enabling peer-to-peer or peer-to-protocol transactions through smart contracts. This eliminates the need for traditional intermediaries. Interest rates in DeFi are determined algorithmically based on supply-demand dynamics, utilization ratios, and protocol-specific methodologies. These rates are frequently adjusted to align with current market conditions.

While TradFi and DeFi lending systems have distinct characteristics and benefits, the evolution toward a more inclusive and transparent financial future is evident. DeFi, with its innovative use of blockchain technology and smart contracts, offers a compelling alternative to the traditional financial model, promising to reshape the landscape of global finance.

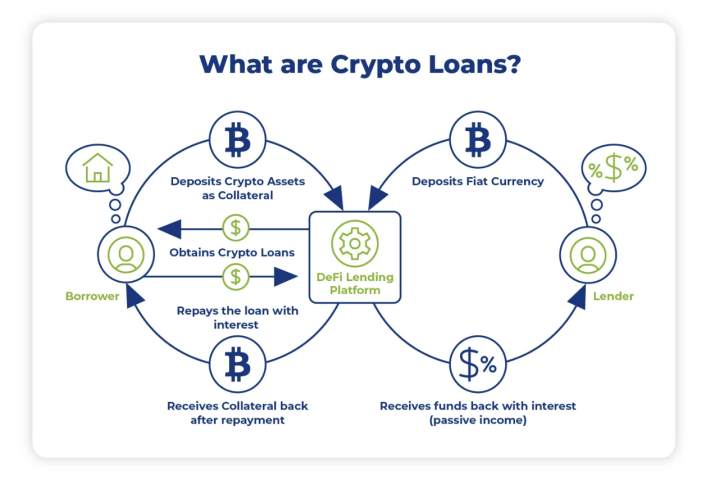

Borrow/Lending Mechanics

Decentralized finance (DeFi) has revolutionized how individuals and entities interact with financial services. At the heart of this transformation are borrowing/lending markets, a fundamental component that diverges significantly from traditional finance (TradFi). Borrow/lend mechanics in DeFi are not only essential for understanding DeFi's operational framework but also exemplify the paradigm shift brought about by blockchain technology in financial interactions.

In DeFi, the borrow/lend system operates peer-to-peer, primarily facilitated by smart contracts on blockchain networks. This decentralized approach eliminates the need for traditional financial intermediaries like banks, making the process more direct, efficient, and accessible.

Transactions in DeFi lending and borrowing are managed and executed by smart contracts. These automated, self-executing contracts with pre-defined rules ensure transparency, security, and trust in the absence of centralized authorities. To promote durability, these smart contracts facilitate financial agreements between two anonymous on-chain parties. A key feature of these DeFi lending agreements, as of 2023, is the requirement for over-collateralization. Borrowers must lock in collateral, typically in the form of cryptocurrencies, that exceeds the value of their loan.

This mechanism mitigates the risk of default, which is particularly pertinent given the absence of traditional credit scoring systems in DeFi. However, there are many valid criticisms that the model is inherently inefficient. For example, say someone would like to borrow $1,000 in a stablecoin like DAI. Depending on the associated collateral requirements, that individual may have to put up $1,500 in value as collateral. During periods of positive, reinforced growth, this method works appropriately as the value of the collateral may rise in value against the loan over time. Unfortunately, during periods of negative growth, the borrower will have to continuously stake more collateral or risk being liquidated.

Interest Rates

Interest rates in DeFi are a critical component of the borrow/lend mechanics, shaping the dynamics of lending protocols and influencing borrower and lender behavior. These rates are more dynamic and market-driven than traditional finance, primarily due to the decentralized nature of the platforms and the underlying blockchain technology. In other words, in DeFi, interest rates are not established by a central authority or bank but are instead determined by supply and demand mechanics within the ecosystem in which individuals are participating.

DeFi platforms typically represent interest rates in an annualized format, either as Annual Percentage Rate (APR) or Annual Percentage Yield (APY). APR represents the simple interest rate over a year, while APY includes the effect of compounding. Many DeFi lending protocols utilize continuous compounding due to the prevalence of zero-duration loans. This method reflects the accruing interest more accurately over time, providing a clearer picture of potential earnings or costs for users. Generally, this approach is necessary as DeFi protocols are constantly in competition with one another to capture on-chain traffic. This can even be extended beyond lend/borrow markets to other DeFi practices like staking.

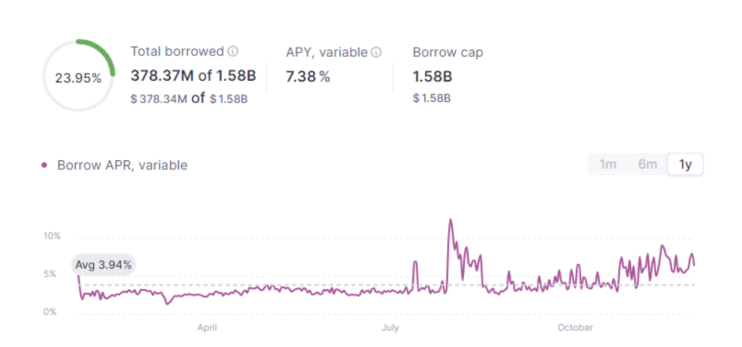

Example of the current borrowing cost of USDC on Aave

Utilization Rates

A common approach in DeFi is utilization-based pricing, where the interest rate is correlated with the utilization ratio of the lending pool. A high utilization rate, indicating strong borrowing demand, increases interest rates. Conversely, lower utilization leads to reduced rates. This model balances the supply and demand within the lending pool efficiently.

When utilization rates are high, it signifies a strong demand for borrowing. This increased demand leads to a rise in both borrowing and supply interest rates. The higher rates perform a dual function:

- Attracting more lenders by offering them higher returns increases the pool's liquidity.

- Moderating borrowing by deterring non-essential or speculative borrowing, ensuring that those take loans with genuine needs.

Over time, this dynamic interaction between demand and supply leads to a market equilibrium, where the availability of assets matches the borrowing needs, maintaining a healthy and stable lending environment. A lower utilization rate suggests excess liquidity in the system, with more assets available than borrowed. In response, the interest rates for both borrowing and lending decrease. The reduction in interest rates encourages more borrowing activities by making it more affordable. Simultaneously, it discourages lenders from adding more assets to the pool as the returns diminish. This natural adjustment process aims to optimize asset utilization, ensuring that assets are not underutilized or idle within the protocol.

While market forces primarily drive interest rates in DeFi, protocol solvency is a critical factor that cannot be overlooked. Solely relying on market dynamics without considering the solvency of the protocol could lead to instability or even insolvency. Therefore, DeFi platforms strive to balance competitive interest rates and the overall financial health of the protocol, ensuring long-term sustainability and trust in the system.