You are reading an excerpt from our free but shortened abridged report! While still packed with incredible research and data, for just $20/month you can upgrade to our FULL library of 50+ reports (including this one) and complete industry-leading analysis on the top crypto assets.

Becoming a Premium member means enjoying all the perks of a Basic membership PLUS:

- Full-length CORE Reports: More technical, in-depth research, actionable insights, and potential market alpha for serious crypto users

- Early access to future CORE ratings: Being early is sometimes just as important as being right!

- Premium Member CORE+ Reports: Coverage on the top issues pertaining to crypto users like bridge security, layer two solutions, DeFi plays, and more

- CORE report Audio playback: Don’t want to read? No problem! Listen on the go.

Aave GHO

In the dynamic world of decentralized finance (DeFi), Aave and MakerDAO are two prominent protocols, each with a unique core product.Aave has established itself as the leading money market in the cryptocurrency space. Its decentralized borrow-lending peer-to-pool model has demonstrated itself to be the most capital-efficient approach for DeFi users to earn interest on their deposits or to obtain immediate access to an asset's liquidity. The Aave platform functions by allowing users to deposit their assets into a lending pool and make them available for others to borrow. In return, borrowers pay back their debts along with interest.

MakerDAO has evolved into a crypto "bank," holding various assets including cryptocurrencies, stablecoins, and real-world assets (RWAs). MakerDAO, also, issues the largest crypto-collateralized stablecoin, DA. Despite their similar Total Value Locked (TVL) metrics and operating costs, these two protocols exhibit significant differences in net revenue.

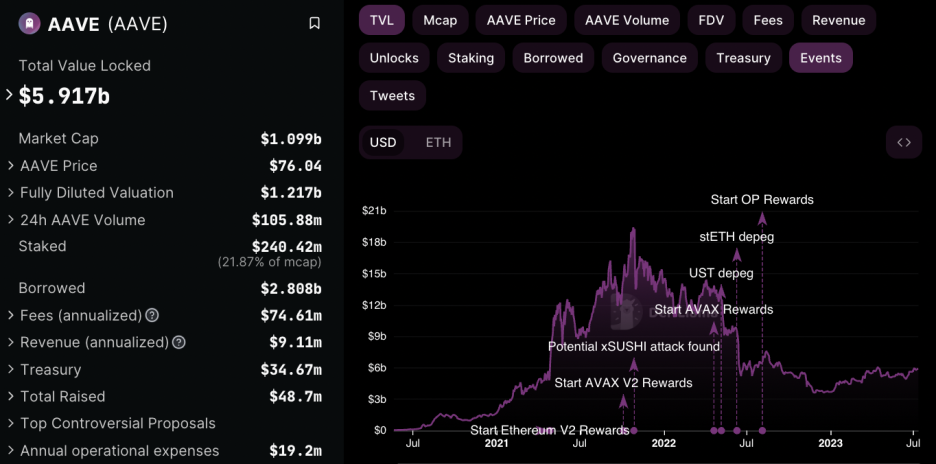

MakerDAO, with a TVL of ~$5.9 billion, generates annual revenues of $110 million against operating costs of $ 27 million. Aave, on the other hand, despite a comparable TVL of $5.9 billion and lower annual fee revenue numbers ($ 75 million/year), reports significantly lower revenue ($9 million). When operating expenses (approximately $19 million) are factored in, Aave's profitability appears elusive.

The divergence in their financial performance can be attributed to their respective business models. MakerDAO, as a stablecoin issuer, creates new money backed by assets, with the same individual providing both the loan request and the collateral assets.

Aave operates through this premise by providing incentives to secure borrow/lending markets and overall protocol liquidity. These incentives include concepts like earned interest where a user deposits crypto in exchange for a pre-determined interest rate. These rates are subject to change depending on the type of cryptoasset being deposited or borrowed as well as the overall utilization rate. When users have deposits on Aave (consisting of at least one deposited asset), users may participate in on-chain swaps between different cryptoassets. Aave currently supports over 25 different cryptoassets, including stablecoins and units of account like DAI, USDC, or USDT for enhanced connectivity and operability.

However, Aave's peer-to-peer lending model requires different customers to supply each side of the market, necessitating a double coincidence of wants for each transaction. This means that Aave depends on both a lender willing to lend USDC and a borrower needing to borrow it for a transaction to occur. Consequently, much of the TVL deposited in Aave remains unused, reflecting a low utilization rate.

In the current phase of the economic cycle (and crypto bear market), where rising interest rates are not conducive to speculative mania, Aave's peer-to-peer lending model faces challenges. In contrast, a stablecoin issuer like MakerDAO can invest its reserves in treasuries and remain solidly profitable.

To address these challenges, Aave has launched a new stablecoin, AAVE GHO. This stablecoin design is similar to MakerDAO's DAI, being a multi-collateral debt position. However, it offers a lower borrowing cost (stability fee) of 1.5%, compared to MakerDAO's 3.5%. Unlike Aave's peer lending system, 100% of this fee goes directly to the Aave treasury.

Aave's new stablecoin, GHO, is underpinned by a meticulously engineered mechanism that balances stability with the dynamic participation of Aave Governance and Facilitators in managing protocol parameters. This design ensures that GHO's value remains aligned with the US Dollar, adjusting programmatically to market forces. Consequently, GHO provides a secure and efficient medium of exchange that benefits all stakeholders.

GHO is designed to be modular, with governance able to delegate the ability to mint GHO to other entities known as facilitators. The first two facilitators are Aave v3 on Ethereum (deposit assets to mint GHO) and a Flashloan facility (mint unbacked GHO provided it is repaid in the same block). In the future, other permissioned facilitators could be added by governance, perhaps to mint GHO backed by Real World Assets. If GHO gains traction and reputable underwriters of RWA debt partner with Aave, this could lead to significant revenue, but it's too early to evaluate this now.

GHO's stabilization mechanism bears resemblance to MakerDAO's DAI stablecoin but with a significant distinction. GHO employs position-based minting, where users deposit collateral on the Aave Protocol and mint GHO against their position. This is a departure from Maker's vault method. Borrowers can mint GHO against their collateral, and when they repay their loan, the GHO protocol burns the GHO tokens, effectively removing the repaid supply from circulation.

The collateral ratio and the fixed interest rate are to be determined by the Aave DAO. This process introduces a new role within the GHO protocol - the Facilitators. Facilitators are the sole entities that can trustlessly mint and burn GHO tokens up to a certain limit, known as a bucket, set by the Aave DAO. Different facilitators will employ different strategies for minting and burning GHO.

One of the first proposed facilitators is the Aave Protocol itself, which will be able to mint a determined amount of GHO to bootstrap its implementation into markets. A key feature of this process is the potential use of portals. Aave's portals allow assets to move across its multichain network, enabling users on Polygon and Avalanche to access tokens native to Ethereum. GHO will inherit this capability, facilitating its trustless distribution across blockchain networks without the complications associated with bridges. This is achieved through message passing on Ethereum.

The revenue model of the GHO token is a central aspect of its design. GHO accrues interest when supplied to a liquidity protocol, with the interest rate determined by Aave governance. Instead of directing the interest paid back on GHO to liquidity providers, Aave proposes that all the revenue generated from GHO be transferred directly to the Aave DAO.

This arrangement grants the Aave DAO full custody over the new revenue, enabling it to fund community projects and initiatives, augment the protocol treasury, and more. This could potentially provide a substantial boost to the Aave DAO's overall revenues, as GHO's utility could extend well beyond the Aave protocol.

In conclusion, Aave's strategic move to launch a stablecoin is a calculated risk, aimed at boosting its profitability and competitiveness in the DeFi space. The success of this initiative will depend on a range of factors, including market dynamics, user adoption, and the effective implementation of incentives. As the DeFi landscape continues to evolve, it will be interesting to observe how Aave's new stablecoin impacts its overall performance and position in the market.