You are reading an excerpt from our free but shortened abridged report! While still packed with incredible research and data, for just $20/month you can upgrade to our FULL library of 50+ reports (including this one) and complete industry-leading analysis on the top crypto assets.

Becoming a Premium member means enjoying all the perks of a Basic membership PLUS:

- Full-length CORE Reports: More technical, in-depth research, actionable insights, and potential market alpha for serious crypto users

- Early access to future CORE ratings: Being early is sometimes just as important as being right!

- Premium Member CORE+ Reports: Coverage on the top issues pertaining to crypto users like bridge security, layer two solutions, DeFi plays, and more

- CORE report Audio playback: Don’t want to read? No problem! Listen on the go.

Aave Transactions, Fees, and Usage

Aave currently generates some of the highest protocol revenue rates for transactions in the crypto economy. But where does the revenue come from? As a quasi-decentralized bank, Aave’s ability to generate revenue and, therefore, value the protocol/token is nearly as straightforward as it gets in the crypto world. Aave’s business model is charging fees for utilizing its platform. These fees are levied on the users when they engage in activities such as borrowing, depositing, liquidating, or utilizing flash loans. The fees collected are split between the Aave DAO and those who offer backing to the protocol's risk management within the Safety Module, through staking of AAVE tokens.

The fee levels for each asset on Aave are determined through governance by the AAVE token holders. The specific fee amount is influenced by various market-related factors, such as the supply, market capitalization, market depth, and others, for each individual asset. This implies that each asset on Aave is assigned a fee level based on the perceived risk perception within the community.

At a high level, Aave is able to charge fees/pat interest due to traders in the market taking positions (long and short) and/or using leverage. The activity in lending markets is largely driven by the occurrence of long and short positions. During a bear market, individuals initiate short positions, utilizing stablecoins as collateral which leads to an increase in stablecoin supply and a subsequent reduction in stablecoin true returns. This results in the borrowing of cryptocurrency, followed by its sale, leading to a rise in the cryptocurrency's true returns.

In a bull market, participants enter into long positions, utilizing their cryptocurrency as collateral which leads to a decrease in cryptocurrency true returns. They then borrow stablecoins to purchase more cryptocurrency from the market, leading to an increase in stablecoin true returns, and subsequently deposit the acquired cryptocurrency as additional collateral, further decreasing cryptocurrency true returns.

The determination of various parameters for the Aave protocol requires a delicate balance between the Aave core contributors and AAVE holders. The fees need to be set at a level that provides adequate revenue for the protocol, offsets the risks it assumes, and incentivizes usage of the platform.

Revenue generation is a crucial aspect of Aave's operations, as it enables the platform to continue its development. Despite being a decentralized entity, Aave still has to compensate its contributors and developers. The revenue is also critical in incentivizing staking within the Safety Module, as it is used to reward the AAVE holders who backstop the protocol's risk. Without a significant revenue stream, there would be limited motivation for AAVE holders to perform the crucial function of backstopping the protocol's risk, and this would result in a reduction in expenses for staking and development.

Throughout 2022, Aave's revenue dropped due to interest rates, more attractive return opportunities in TradFi, and users leaving crypto during the 2022 bear market. Below is the amount of money Aave earns after paying out bettors from the Safety Module. These are the funds controlled by AAVE holders. The revenue generated by the protocol from January to November 2022 is ~$22 million. This puts Aave on track to achieve its projected annual income of $23M. Given that Aave is a protocol with about $6.4 billion in TVL and a market cap of $1 billion, $23 million per year does not appear to be particularly lucrative. However, Aave draws deposits through a low net-interest margin, which means that Aave takes less money off the top for profits than typical banks. As a result, Aave's profitability may always be relatively subdued.

Fee generation has been modest at best for most crypto protocols compared to Ethereum’s $32 million every week. The next-closest smart contract platform is Avalanche at $1.8 million. Notably, Aave has connectivity to both Ethereum (being an ERC-20 token) and Avalanche, giving Aave access to two of the largest fee-generating smart contract platforms in the world. This has undoubtedly assisted Aave’s growth since 2020.

Maker

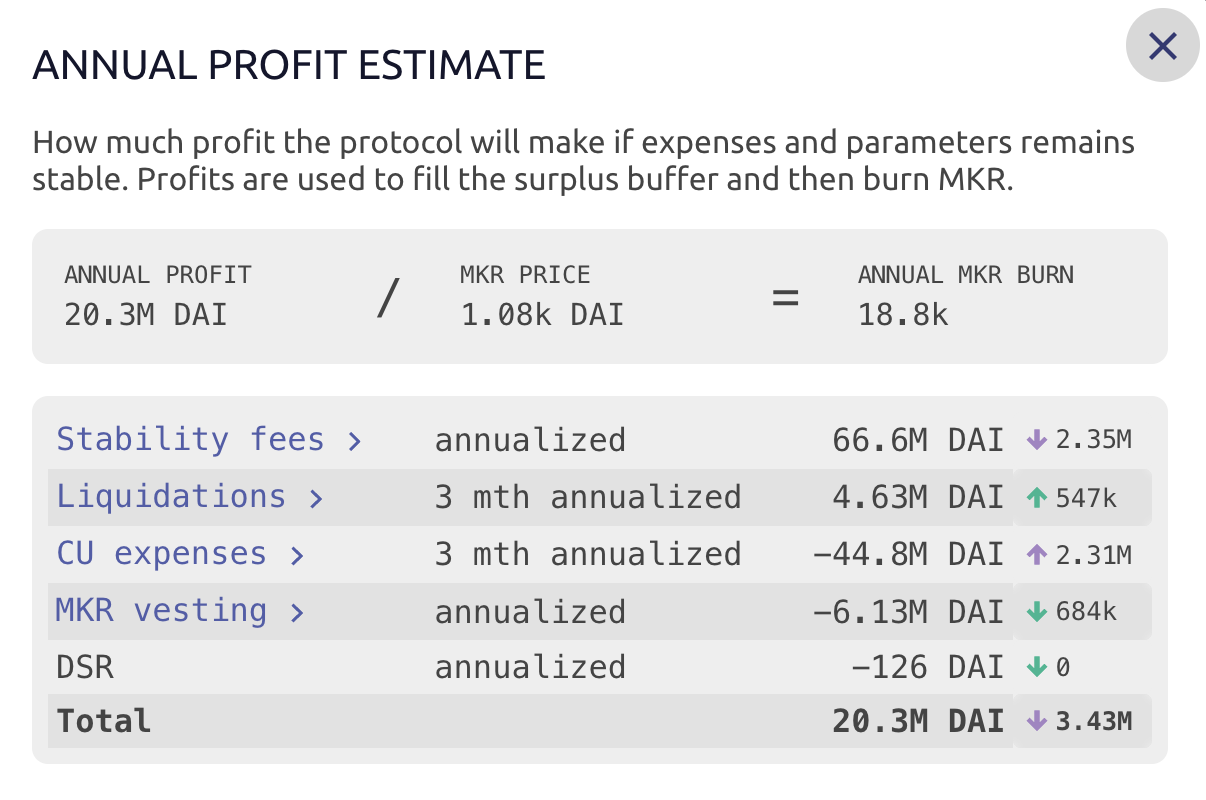

Value accrues back to MKR through buybacks from revenues, liquidations, and excess reserve assets. The Maker surplus is the amount of money in excess if every debt was instantly repaid. The surplus increases with time as fees on debt accrue and when liquidations net a profit for the system. The system aims to keep a buffer of 250M, and when the surplus surpasses this buffer the exceeding amount is used to buy back and burn MKR. Whenever the DAO has expenses, these are paid by pulling DAI from the surplus.

MKR revenues. Source

MKR revenues. Source

Real World Assets (RWA)

In April 2021, MKR governance voted and passed an executive order that allows real estate assets as collateral in the form of an ERC-20 token. Two separate interest-bearing tokens will be created, DROP and TIN, as non-fungible tokens (NFTs) tied to individual deposits from New Silver, the real estate partner in this initiative. Adding real-world assets has always been on the roadmap for Maker, and the new addition significantly increases the number of loans that can be produced as such a large market of collateral is now available.

In 2022, MakerDAO voted to launch a new $30M collateral vault consisting of €40M in OFH bonds issued by Societe Generale (SocGen), one of the largest French banks. The AAA-rated bonds were issued on Ethereum for the first time in 2020 and are backed by French mortgages. SocGen's subsidiary SG-Forge is responsible for pledging the OFH bonds to Maker, creating the DAI, and lending it to SocGen, who will convert it to USD. Maker has recruited the Paris-based financial services firm DIIS Group to represent Maker in the real world and enforce the loan terms on Maker's behalf.

The loan will have a stability charge, or interest rate, of 0.5%, and it may be liquidated if the collateral ratio falls below 115%. A daily valuation will be performed by an independent collateral agent to ensure that the market value of the OFH bonds exceeds the liquidation ratio. If the value falls below the collateral ratio, the agent will alert Maker governance, who can then trigger the liquidation using an RWA-specific liquidation oracle contract.

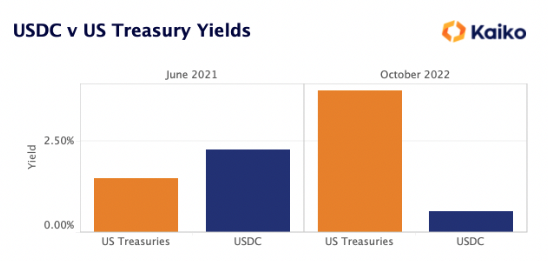

The addition of $630M worth of real-world assets indicates a 15-fold increase in Maker's exposure to RWA. However, RWA still constitutes less than 10 percent of total outstanding DAI, though. At its core, Maker's RWA initiative aims to further diversify the protocol's collateral in order to minimize risk and hedge against DAI's reliance on USDC (USDC makes up more than half of DAI's collateral). Initiative proponents emphasize the significance of RWA in expanding the scope of DAI, enhancing its stability, and increasing its decentralization.

Additionally, in Q4 2022, MakerDAO voted to invest $500 million into U.S. Treasuries and corporate bonds. The vote was passed with the hopes that USTs can earn greater yield than other collateral backing DAI. The majority of DAI's $9 billion collateral pool is made up of USDC, which currently earns a very low yield as DeFi yields have contracted during the bear marker of 2022. MakerDAO will allocate 80% of the $500 million to USTs, with 10-year treasury yields rising to nearly 2.5% in just over a year to 3.9%.

Source: Kaiko

Source: Kaiko

Fees, Protocol Revenue, and Value Capture

All accrued fees on MakerDAO are paid in MKR. The protocol purchases MKR off the secondary market and burns it, ensuring proper alignment incentive between MKR token holders. The burning of MKR reduces its supply in circulation through its intentional destruction. It is an effective method for increasing and stabilizing the price of MKR with the increased value given to the holder resembling that of a dividend.

A comparison of DeFi "blue chips" and their market cap to revenue ratio. MKR remains comparable to peers in this regard with SNX being the outlier. Image credit: TheBlock

A comparison of DeFi "blue chips" and their market cap to revenue ratio. MKR remains comparable to peers in this regard with SNX being the outlier. Image credit: TheBlock

A significant milestone for MKR holders, Maker finally began raising interest rates away from zero in Q3 2020, translating to significant returns for MKR holders. Annualized earnings to MKR holders topped $27 million and in 2021 saw even more dramatic growth with projected annual returns of ~$200 million if all parameters remained steady throughout the remainder of the year

MakerDAO earnings. Source: Messari

MakerDAO earnings. Source: Messari

However, despite the market downturn in 2022 slowing Maker's profitability somewhat, it still remains at the top when comparing the amount of revenue generated vs. the amount of tokens issued for incentives.

Source: TokenTerminal

Source: TokenTerminal