If the crypto world were judged by one of the most common metrics used in the stock market — namely, the ability to generate revenue for networks — the rankings would look very different from the usual market capitalization charts.

That’s because the “fee rankings” — the commissions collected by networks — tell us at least two things: first, which sectors are actually generating volumes in the crypto space; and second, which networks are most successfully hosting these sectors.

The Fee Rankings: A Few Surprises for the Newcomers

On one side, we have the narratives; on the other, the numbers — and numbers appeal to everyone because they tell many stories, often depending on who’s telling them. Here, we aim to provide some clarity, presenting in a neutral way the data reported by the chains and their… commissions.

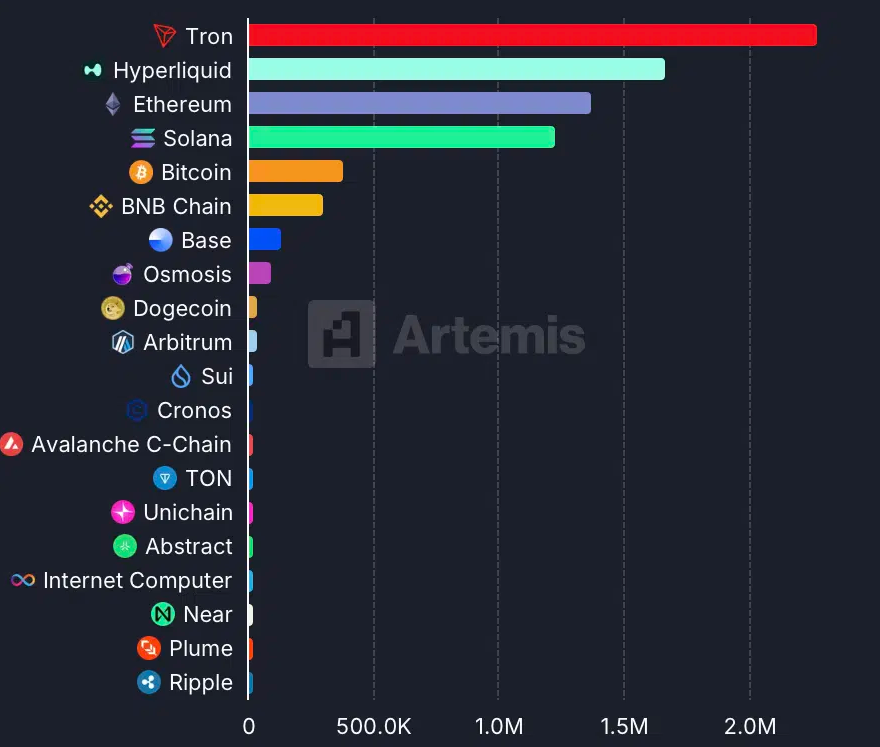

The chart speaks for itself: while it reflects the past 24 hours, it also captures the broader trend of recent times, during which transaction volumes on the most established chains have been relatively muted.

Tron is the standout — though perhaps only to those who don’t closely follow developments in the crypto world. It collects a significant amount of fees, primarily linked, as we’ll see, to the stablecoin sector. In fact, it’s Tether’s USD that drives the bulk of activity on this chain.

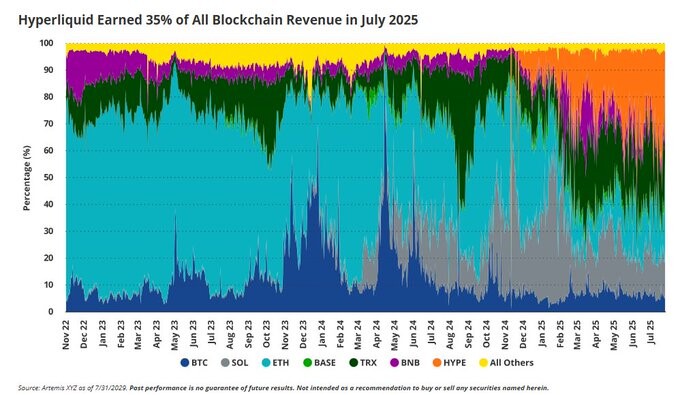

A relative surprise comes in second place: Hyperliquid, which Alessandro Adami recently covered in a special feature. The decentralized derivatives (and spot) exchange is experiencing a golden moment, accounting for roughly 35% of all fees collected, as also noted by Matthew Sigel of VanEck in a recent post on X.

In third place is Ethereum, which, along with other high-profile chains, is currently experiencing a period of relative stagnation in fee generation — a consequence of transaction volumes that resemble bear market conditions.

Fourth place goes to Solana, which continues to prove itself as the only network capable of challenging the top tier of the crypto sector, at least in terms of relevance and usage. It would now be unfair to still call it a “surprise.” The crypto market has taken shape, and Solana is unquestionably a solid player in this space.

Bitcoin, to the surprise of many readers, comes in only fifth. This is yet another indication that, in recent days, weeks, and months, the trend has been driven primarily by ETFs and traditional finance. For many, this signals the “death” of Bitcoin — not as an investment asset, but as a free monetary system. Whether this trend holds or is reversed will be left to history to decide.

Stablecoins and Open Trading

Dominating the sector and driving fee generation — which ultimately represents network revenue and one of the most telling metrics for assessing the health of the crypto ecosystem — are two key segments.

The first is stablecoins, with Tether USDT and USDC standing out as two of the most successful protocols ever created, grown, and developed in the blockchain space.

The second is (relatively) decentralized derivatives trading. Hyperliquid is currently enjoying a period of strong momentum, reflected in the fees it collects, and it could well establish itself as one of the most profitable niches going forward.

For now, other sectors remain far behind — a clear sign that the strongest current use cases for blockchain and crypto lie in investment and payments.