With the end of the September interest rate hike and the terminal interest rate trend brought by the dot-matrix, risk market sentiment continued to be positive. With the closing of US stocks in the early morning hours, the BTC and ETH, driven by the Nasdaq, almost returned to the price before the interest rate hike. They did not fall below the low point of yesterday's interest rate hike. So, while a terminal rate of 4.4% (4.5%) is enough to make 2022 desperate, there is no silver lining. Let us now set the timetable for rolling back the challenges and opportunities that may be encountered, so that we can make the appropriate moves. First, it is well known that what Powell said in his speech, the bitmap does not necessarily represent the final program, but it does not necessarily represent the Fed's forward thinking. After all, for the current Fed, fighting inflation is now its top priority, and raising interest rates and shrinking tables are all weapons in its arsenal. Fed members who are studying rate hikes every day must know better than us what the implications are, and the bitmap reflects the revolt of these FOMC members over inflation that they are likely to be unable to contain by conventional means. As the saying goes, a pain is better than a pain. A rapid and short-term end to inflation is the Fed's top priority. Therefore, we can also learn from the consensus within the Federal Reserve that the October CPI is likely to continue the trend of September, that is, the CPI may indeed fall year-on-year, but the magnitude of the drop will not be large, and even the signs of a rebound cannot be ruled out. And core CPI is likely to continue rising. There is no meeting in October, so the number of jobless claims in the first three weeks of September and October is less important. After all, at yesterday's Fed meeting, tolerance for unemployment was raised. Therefore, the first key point was the announcement on September 27 of the housing price trend in July. Although this data is less delayed than the current CPI, it can still not be judged that the September CPI data provides a reference. Especially from the housing price trend shown in the chart, starting from March, housing prices started to fall, and June housing prices even showed a larger drop. Because housing prices and rents are highly correlated, and the housing index comprising them accounts for the largest share of the CPI and the core CPI, the CPI's movements are largely determined, if anything, by the behavior of housing. Also released at the same time is the trend of housing prices in the big city of S&P/CS20 in July, and the sales situation of new homes in August, all these data are very helpful in predicting the September CPI. In particular, there is still a long way to go from house prices to rents. Adding to the headache for rents, the trend in August has pushed rents above all-time highs since 1990, which means high inflation. So the September 27 figure may not change the market much, but it will be a good warning time for investors considering buying at a low or selling risky assets.

The next data should be about two EIA crude inventories, but because of the mid-term elections, Biden has taken oil from the bottom to force oil prices back down to around 80 dollars, so this data is not very meaningful. At this point, the oil price is down by nearly seven dollars compared to the same period last month, and if the oil price continues to fall, the drop in oil price may be even larger. Previously calculated, for every ten dollars drop in oil price, the CPI could drop by 0.4%. Then there is the core PCE number to be released on September 30. Also because there is no October meeting, the core PCE number is not likely to be very volatile, but it is very indicative of the direction of the core PCE number for October and the CPI number for September, especially since the Fed has publicly said that it will pay more attention to the core PCE number than to the CPI number. With the unemployment rate poised to rise, the Fed's hold on unemployment is set to remain below 4% in 2022, so the September unemployment rate, to be released on October 7, and the non-farm data for September, set a ceiling for the Fed's rate hike on November 3. That is, the lower the unemployment rate and the stronger the non-farm data are, the more likely the Fed will choose to raise interest rates by 75 basis points in November, with CPI equivalent. So if unemployment falls and non-farm data strengthens, that would be my first assumption of a stake, even if it had little impact on risk market movements at the time. And if the unemployment rate rises to 4%, which is unlikely, then this will be my first time since then, regardless of the non-farm data, to make the lowest possible bet that unemployment will probably push the Fed to the wall. Then there is the release of the PPI data on October 12, this data can be used as the lead CPI data, if the PPI data has a larger decline, it will help manufacturers to sell and service the corresponding CPI weakened, and even as a standard for judging the price of food and new cars, and food is second only to housing in the CPI the largest proportion. The result of this data will be the second to determine my share of construction. The next day, October 13, was the most important release of CPI for September. Through unemployment, non-farm and PPI data have basically decided the first time to build stocks, and CPI data decide whether to build stocks according to this share. The first is the year-on-year CPI (annualized CPI), and the second is the month-on-month CPI (monthly CPI). These two figures are the main considerations for construction. If the annualized rate falls below 7.5% and falls short of expectations, the monthly rate goes negative, and the core CPI is falling, I will position according to market share. This is a bet that the Fed would be willing to sell favoritism to Democrats in a positive CPI data, favoring a 50-basis-point increase in November and a 4.25% terminal rate at the end of the year, implying a 125-basis-point reduction in aggregate interest rates to 100 basis points in November and December. And if the last two of these three are agreed, but CPI is not lower than 7.5% per year, but lower than expected, my position-building program may be discounted, choosing a smaller share of positions or abandoning the plan, depending on how much the core CPI falls. For this is likely to divide the Fed, and while a 50 basis point increase in November is still possible, a change in the terminal rate is unlikely to materialize. Then there's the October NAHB index for the U.S. real estate market, which will be released Oct. 18, and the August FHFA monthly and August S&P/CS20 annualized home price indices for major cities, which will be released Oct. 25. These are the same as July's data, but they are not directly attributable to building positions, and yet the change in home prices, the bulk of the CPI, is still the expectation of the second building share. Measure the October CPI data released in November. The next big numbers to focus on will be the jobless claims figure in the early part of the week, the last before the November rate rise, and GDP, released on Oct. 27. Because the GDP figure is so much less important than it was when the Q2 Fed was still talking tough, having known that the economy was bound to shrink and the Fed would rather keep joblessness and recession in place than fight inflation. In particular, if the reading continues to decline it will not necessarily dent the Fed's resolve to raise interest rates by 75 basis points in November, but it will be a fly in the ointment for Democrats heading into the midterm elections. Three consecutive quarters of negative data represent almost no prospect of positive GDP growth in 2022. And if the month-on-month increase is good, if the month-on-month decline, the impact is likely to cause a decline in risk markets. The next day's core PCE data will be the last share adjustment before the second position is built, then the 2 a.m. interest rate hike on November 3 and the end-of-year terminal interest rate announcement are also the main considerations for determining whether to build positions for the second time. This time, it will be simpler. If the interest rate hike is greater than or equal to 75 and the terminal interest rate is less than or equal to 4.5%, then a few positions will be built, betting on the last big interest rate hike in 2022. In December, the interest rate hike will be up to 50 at most, and then the slowdown will be started. A small position would also be built if the increase was 50 basis points or more and the terminal rate was 4.25% or less. betting on a reduction in terminal rates is good for markets and good for the mid-term elections. Of course, I'm not convinced that a rate hike below 50 and a terminal rate of 4% will occur, and if they do occur, just take sides, because this represents the Fed and the Democrats on the same side, and Powell's willingness to raise rates at any cost is bullshit. So far before and after the November 3 interest rate hike, all the points and key points I personally think have been announced, and the reason to follow this time line to build positions is that if there is no new epic interest or short of the BTC and ETH in these 40 days, then the overall trend will inevitably follow the Nasdaq, which must depend on the changes of various macro-emotions, which is the main reason why I consider this kind of construction scheme. The other is that during this period, there is a short-term strategy that is completely independent of macro sentiment and almost independent of CPI. That is, the third-quarter earnings season for Nasdaq-leading stocks, especially tech stocks, are highly correlated with BTC and ETH. So you can make a short-term buying (long) or selling (short) strategy before earnings season is announced. That's not a detailed strategy, so let's discuss it alone.

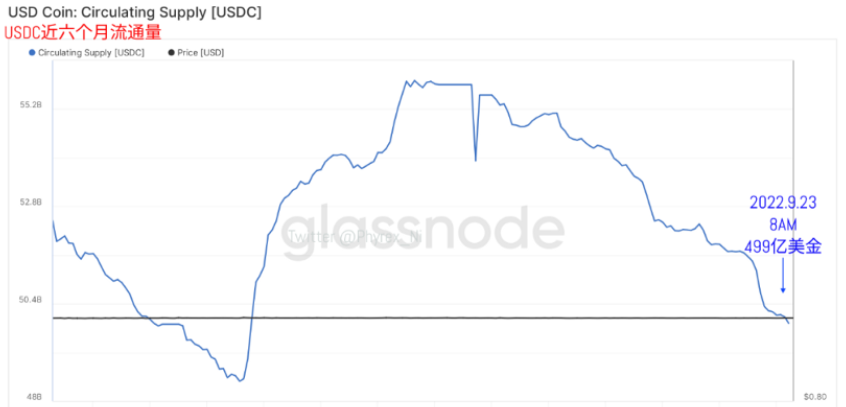

For currency market data, the most important is still the situation of funds, especially the entry of external funds and the reduction of funds in the market. Statistically, after the macro-sentiment shift that followed the rate hike, while USDT showed signs of renewed growth, this was offset by USDC's market capitalization falling below $50 billion, and BUSD's horizontal movement showed signs of continued weakness in the major stablecoins, with continued loss of money.

In terms of stock on the stock exchanges, although BTC prices were relatively firm during the key period of interest rate increase, the stock levels were rising continuously, which indicated that the BTC's buying sentiment was low, or the selling pressure was excessive to prepare for departure. And while the ETH lost a lot of value and the exchange rate would fall below 0.07, the stock of the exchange did lose a lot of weight, which could help a little in the future.

Finally, as the volatility of Nasdaq futures after the closing of US stocks can be seen, Nasdaq futures actually appeared a new low after interest rate increase, but it is not known whether the reason for the over-fall BTC and ETH both appeared to follow the rise but not follow the fall, so there is still caution. On the emotional side, BTC has turned away from being bearish and has a bullish trend. Although ETH is still more bearish, it is not very bearish